You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5783)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (72)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Statement of Account for M/S STEEL HYPERMART INDIA PVT LTDDocument44 pagesStatement of Account for M/S STEEL HYPERMART INDIA PVT LTDSURANA1973No ratings yet

- In Gold We Trust 2015Document140 pagesIn Gold We Trust 2015Gold Silver Worlds100% (1)

- Usage Patterns of Credit Card Holders in AhmedabadDocument141 pagesUsage Patterns of Credit Card Holders in AhmedabadAshraj_16No ratings yet

- Icici ChallanDocument1 pageIcici ChallanKimet Chhendipada AngulNo ratings yet

- Bankers As Buyers 2023-1Document66 pagesBankers As Buyers 2023-1devi_mamoniNo ratings yet

- Branch Banking IBP Stage 1 PDFDocument216 pagesBranch Banking IBP Stage 1 PDFSarim Shahid67% (3)

- PNB V CA GR No.107508Document2 pagesPNB V CA GR No.107508mayaNo ratings yet

- Sales and Trading or Relationship Manager or Fixed Income SalesDocument2 pagesSales and Trading or Relationship Manager or Fixed Income Salesapi-121440494No ratings yet

- Credit Creation Theory (: Kalecki and Schumpeter)Document14 pagesCredit Creation Theory (: Kalecki and Schumpeter)Anamik vermaNo ratings yet

- AKPF Fast Facts PDFDocument2 pagesAKPF Fast Facts PDFBernard Vincent Guitan MineroNo ratings yet

- Financial Analysis of Public and PrivateDocument31 pagesFinancial Analysis of Public and Privaten.beauty brightNo ratings yet

- TDS Return LegalraastaDocument10 pagesTDS Return LegalraastaLegalRaastaNo ratings yet

- Experience The Difference: Annual Report & Accounts 2003Document41 pagesExperience The Difference: Annual Report & Accounts 2003thestorydotieNo ratings yet

- Articles of Indian Constitution in Telugu LanguageDocument2 pagesArticles of Indian Constitution in Telugu LanguageVali BayikatiNo ratings yet

- BLM-1603 Law on Pledge and MortgageDocument20 pagesBLM-1603 Law on Pledge and MortgageMyka C. DecanoNo ratings yet

- Recalled Questions - Promotion Test For Scale II To IIIDocument8 pagesRecalled Questions - Promotion Test For Scale II To IIIcandeva2007No ratings yet

- The Great Indian Bank RobberyDocument10 pagesThe Great Indian Bank RobberyJustin HallNo ratings yet

- Teena FDHGDocument2 pagesTeena FDHGTeena VarmaNo ratings yet

- BSP PresentationDocument27 pagesBSP PresentationMika AlimurongNo ratings yet

- One Private Investment Application Form (SCMF)Document1 pageOne Private Investment Application Form (SCMF)ksskarthi50% (2)

- History of World Bank and its influence on ASEANDocument1 pageHistory of World Bank and its influence on ASEANFatimah Rahima JingonaNo ratings yet

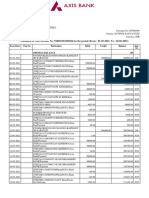

- Account STMTDocument3 pagesAccount STMTDhanush KumarNo ratings yet

- Towards Future of SME Lending in JapanDocument14 pagesTowards Future of SME Lending in JapanADBI Events100% (1)

- Know Your Customer Quick Reference GuideDocument2 pagesKnow Your Customer Quick Reference GuideChiranjib ParialNo ratings yet

- Maritime Short Courses Enquiry Email ResponseDocument11 pagesMaritime Short Courses Enquiry Email ResponseChandanKumarNo ratings yet

- EMI Calculator BreakdownDocument12 pagesEMI Calculator BreakdownHemant Singh TanwarNo ratings yet

- AC 506 Midterm ExamDocument10 pagesAC 506 Midterm ExamJaniña NatividadNo ratings yet

- Gold's Losing Luster Reveals The Cracks in Sri Lanka's Pawning SegmentDocument7 pagesGold's Losing Luster Reveals The Cracks in Sri Lanka's Pawning SegmentRandora LkNo ratings yet

- Draft Format of Board ResolutionDocument2 pagesDraft Format of Board ResolutionzamasuaepNo ratings yet

- ATM ComplaintDocument6 pagesATM ComplaintKUTV2NewsNo ratings yet