You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- RamayanaDocument22 pagesRamayanaManisha PrajapatiNo ratings yet

- Ipo Summit at LahoreDocument25 pagesIpo Summit at LahoreManisha PrajapatiNo ratings yet

- BeezedDocument27 pagesBeezedManisha PrajapatiNo ratings yet

- Proforma For Students ListsDocument1 pageProforma For Students ListsManisha PrajapatiNo ratings yet

- Comparative Ratio Analysis of Britannia and CadburyDocument21 pagesComparative Ratio Analysis of Britannia and CadburyPriyank Galaw57% (7)

- Daily TaskDocument1 pageDaily TaskManisha PrajapatiNo ratings yet

- The Indian Cosmetics Industry Has Seen Strong Growth Over The Past FewDocument3 pagesThe Indian Cosmetics Industry Has Seen Strong Growth Over The Past FewManisha PrajapatiNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- CreditReport Piramal - Mahendra Jain - 2023 - 05 - 12 - 11 - 43 - 04.pdf 12-May-2023 PDFDocument7 pagesCreditReport Piramal - Mahendra Jain - 2023 - 05 - 12 - 11 - 43 - 04.pdf 12-May-2023 PDFGamer SinghNo ratings yet

- Groups in TallyDocument3 pagesGroups in TallyenimaneNo ratings yet

- FS PT BPS Fy2020Document5 pagesFS PT BPS Fy2020A Jonathan100% (1)

- Tennessee-Atlantic Paper Company capital investment analysisDocument3 pagesTennessee-Atlantic Paper Company capital investment analysisYasir AamirNo ratings yet

- Accounting Assignment 1Document2 pagesAccounting Assignment 1Hamna FarooqNo ratings yet

- Mock Prelim - Intermediate AcctDocument9 pagesMock Prelim - Intermediate AcctNikki LabialNo ratings yet

- ABMF 3174 AssignmentDocument39 pagesABMF 3174 AssignmentRayNo ratings yet

- On January 1 Pulse Recording Studio Prs Had The FollowingDocument1 pageOn January 1 Pulse Recording Studio Prs Had The FollowingLet's Talk With HassanNo ratings yet

- LIM TONG LIM Vs Phil Fishing GearDocument3 pagesLIM TONG LIM Vs Phil Fishing GearRhea Mae A. SibalaNo ratings yet

- Cash Flow Part 2 To 7 Term 2 Sunil PandaDocument35 pagesCash Flow Part 2 To 7 Term 2 Sunil PandaAnupama SinghNo ratings yet

- Bank’s Logo Loan ApplicationDocument4 pagesBank’s Logo Loan ApplicationMonika ShuklaNo ratings yet

- Welcome: Selestian AugustinoDocument24 pagesWelcome: Selestian AugustinoDane Chybo TzNo ratings yet

- CHAPTER 8 - Audit of Liabilities: Problem 1Document27 pagesCHAPTER 8 - Audit of Liabilities: Problem 1Mikaela Gale CatabayNo ratings yet

- AUDC To AH - 6.28.23Document11 pagesAUDC To AH - 6.28.23Sean KeenanNo ratings yet

- BOOKING FORM - Gulmohar Residency 18 07 - 19Document2 pagesBOOKING FORM - Gulmohar Residency 18 07 - 19Venkat DhruvaNo ratings yet

- Grade 7 Ems Marking Guideline 2023Document6 pagesGrade 7 Ems Marking Guideline 2023Mavis100% (1)

- FAR - Level 1 TestDocument3 pagesFAR - Level 1 TestRay Joseph LealNo ratings yet

- Excel 19Document6 pagesExcel 19debojyotiNo ratings yet

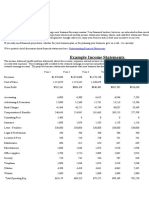

- Example Income Statements: Business Plan Financial ProjectionsDocument3 pagesExample Income Statements: Business Plan Financial ProjectionsSUMANTO SHARANNo ratings yet

- Leases - Brief ExercisesDocument5 pagesLeases - Brief ExercisesPeachyNo ratings yet

- Intermediate Acctng. AR Online ResorcesDocument14 pagesIntermediate Acctng. AR Online ResorcesDos BuenosNo ratings yet

- Promise To Pay and Order To PayDocument2 pagesPromise To Pay and Order To PayShazna SendicoNo ratings yet

- Journal Ledger Trial BalanceDocument8 pagesJournal Ledger Trial BalancejessNo ratings yet

- Payment Instruments ExplainedDocument40 pagesPayment Instruments ExplainedThanh HuyenNo ratings yet

- Engineering Economics: ENGG 404Document7 pagesEngineering Economics: ENGG 404Angel SakuraNo ratings yet

- Simple Interest and Discount Mathematics of InvestmentDocument13 pagesSimple Interest and Discount Mathematics of InvestmentMary Maevelyn MaglahusNo ratings yet

- FAC1503 Lecture 1Document14 pagesFAC1503 Lecture 1Beverly JohnNo ratings yet

- Oblicon ReviewerDocument3 pagesOblicon ReviewerJulia JumagdaoNo ratings yet

- Slides 07Document44 pagesSlides 07Vinay Gowda D MNo ratings yet

- Tutorial 2: Exercise 12.2 Calculation of Current TaxDocument13 pagesTutorial 2: Exercise 12.2 Calculation of Current TaxKim FloresNo ratings yet