You might also like

- Financial Accounting and Reporting Study Guide NotesFrom EverandFinancial Accounting and Reporting Study Guide NotesRating: 1 out of 5 stars1/5 (1)

- Accounting Basics for Non-AccountantsDocument129 pagesAccounting Basics for Non-Accountantsdesikan_r100% (7)

- AS-3 Cash Flow StatementDocument26 pagesAS-3 Cash Flow StatementJonathan BarretoNo ratings yet

- Finance Primer - 2016Document26 pagesFinance Primer - 2016Gurram Sarath KumarNo ratings yet

- FADM Cheat SheetDocument2 pagesFADM Cheat Sheetvarun022084No ratings yet

- Cash Flow Statements (FRS 1) : A2 Level Accounting - Resources, Past Papers, Notes, Exercises & QuizesDocument6 pagesCash Flow Statements (FRS 1) : A2 Level Accounting - Resources, Past Papers, Notes, Exercises & QuizesCross MatricNo ratings yet

- Apuntes AccountingDocument35 pagesApuntes AccountingPatricia Barquin DelgadoNo ratings yet

- PFS StudyDocument19 pagesPFS Studyigorwalczak321No ratings yet

- Cash Flow StatementDocument11 pagesCash Flow StatementKrishna MohanNo ratings yet

- Notes CanniiDocument53 pagesNotes Canniicaro.colcerasaNo ratings yet

- Accounting Acc106Document23 pagesAccounting Acc106zary100% (3)

- Dpa1013 Note Chapter 3Document28 pagesDpa1013 Note Chapter 3Mohd Noor HamamNo ratings yet

- Introduction and Double EntryDocument36 pagesIntroduction and Double EntryInsyirah Nur ZakariaNo ratings yet

- Types of FI AccountsDocument12 pagesTypes of FI Accountsragz22No ratings yet

- CFA Level 1Document90 pagesCFA Level 1imran0104100% (2)

- Statement of Cash FlowsDocument36 pagesStatement of Cash FlowsLoida Yare Laurito100% (1)

- Chapter 1 - Introduction To Accounting: Concepts and PrinciplesDocument25 pagesChapter 1 - Introduction To Accounting: Concepts and Principlesd_hambrettNo ratings yet

- Accounting Cheat SheetsDocument4 pagesAccounting Cheat SheetsGreg BealNo ratings yet

- The Accounting CycleDocument78 pagesThe Accounting CycleNajib Ali MurtadloNo ratings yet

- CFA Level 1 (Book-B)Document170 pagesCFA Level 1 (Book-B)butabutt100% (1)

- Chap 013Document16 pagesChap 013Jessica GonzalezNo ratings yet

- FCFChap002 - Financial StatementsDocument23 pagesFCFChap002 - Financial StatementsSozia TanNo ratings yet

- Review sessionDocument25 pagesReview sessionK60 Bùi Phương AnhNo ratings yet

- Revision Notes Accounting ADocument5 pagesRevision Notes Accounting AAndrewNo ratings yet

- Review of Chapter 8/9Document36 pagesReview of Chapter 8/9BookAddict721100% (1)

- A Lecture6 9 29 22Document46 pagesA Lecture6 9 29 22Kawaii SevennNo ratings yet

- Basic AccountingDocument25 pagesBasic AccountingGaurav AgarwalNo ratings yet

- Acb3 01Document41 pagesAcb3 01lidetu100% (3)

- Ifsa Chapter2Document31 pagesIfsa Chapter2bingoNo ratings yet

- Cash Flow StatementDocument38 pagesCash Flow StatementSatyajit Ghosh100% (2)

- Administer Subsidiary Accounts and Ledgers GuideDocument42 pagesAdminister Subsidiary Accounts and Ledgers Guidegizachew alekaNo ratings yet

- MBA 560 Accounting Managerial NotesDocument18 pagesMBA 560 Accounting Managerial NotesDesi MarianNo ratings yet

- Double-Entry Book-Keeping Slides For Handout - Session 4Document10 pagesDouble-Entry Book-Keeping Slides For Handout - Session 4Dilfaraz KalawatNo ratings yet

- Learning Guide: LevelDocument39 pagesLearning Guide: LevelAgat100% (1)

- Financial Statement AnalysisDocument63 pagesFinancial Statement AnalysisHarsh DalmiaNo ratings yet

- Paradise Valley College Financial Training GuideDocument34 pagesParadise Valley College Financial Training GuideGuddataa Dheekkamaa100% (6)

- Session 2 Review of AccountingDocument39 pagesSession 2 Review of AccountingMargaretta LiangNo ratings yet

- Chap2+3 1Document36 pagesChap2+3 1Tarif IslamNo ratings yet

- Debit and CreditDocument32 pagesDebit and CreditBasma ShaalanNo ratings yet

- Advanced General Ledger-Reporting and Using Optional ChartfieldsDocument18 pagesAdvanced General Ledger-Reporting and Using Optional Chartfieldsje-ann montejoNo ratings yet

- Fundamentals of Accounting Chapters 3-4Document16 pagesFundamentals of Accounting Chapters 3-4Renshey Cordova MacasNo ratings yet

- Business Analysis and Valuation - Measuring Cash FlowsDocument35 pagesBusiness Analysis and Valuation - Measuring Cash FlowscapassoaNo ratings yet

- Unit I - Accounting EquationDocument6 pagesUnit I - Accounting EquationAnime LoverNo ratings yet

- Lecture4 Economy EnglishDocument14 pagesLecture4 Economy Englishali5halilNo ratings yet

- CH 2 Accounting TransactionsDocument52 pagesCH 2 Accounting TransactionsGizachew100% (1)

- Purpose of Financial StatementDocument22 pagesPurpose of Financial StatementMonkey2111No ratings yet

- Trial Balance To Profit & Loss A/c and Balance Sheet For Corporate & Non-Corporate EntitiesDocument24 pagesTrial Balance To Profit & Loss A/c and Balance Sheet For Corporate & Non-Corporate EntitiesChintan PatelNo ratings yet

- Week 2Document9 pagesWeek 2Angelina ThomasNo ratings yet

- HGFDDocument6 pagesHGFDHasanAbdullahNo ratings yet

- AcctngDocument7 pagesAcctngKazumi ShioriNo ratings yet

- Introduction To Financial Accounting: Key Terms and Concepts To KnowDocument16 pagesIntroduction To Financial Accounting: Key Terms and Concepts To KnowAmit SharmaNo ratings yet

- Financial Accounting BasicsDocument24 pagesFinancial Accounting BasicsMonirHRNo ratings yet

- Note 2Document7 pagesNote 2faizoolNo ratings yet

- Basic Elements of AccountingDocument19 pagesBasic Elements of AccountingMonique DanielleNo ratings yet

- Acctg CycleDocument10 pagesAcctg CycleBenjamin dela Cruz Cailao IIINo ratings yet

- Tle ReviewerDocument8 pagesTle ReviewerQuella Zairah ReyesNo ratings yet

- Acct1501 Notes: 1. Introduction To Financial AccountingDocument11 pagesAcct1501 Notes: 1. Introduction To Financial AccountingLena ZhengNo ratings yet

- Week 4 - ACCY111 NotesDocument10 pagesWeek 4 - ACCY111 NotesDarcieNo ratings yet

- VALUCON - SCF & ManAccDocument21 pagesVALUCON - SCF & ManAccDanna VargasNo ratings yet

- Curs 5 AuditDocument18 pagesCurs 5 AuditcociorvanmiriamNo ratings yet

- Ex Portfolio StructureDocument11 pagesEx Portfolio StructurecociorvanmiriamNo ratings yet

- Portfolio Management Tips from SimonaDocument14 pagesPortfolio Management Tips from SimonacociorvanmiriamNo ratings yet

- Czech RepublicDocument7 pagesCzech RepubliccociorvanmiriamNo ratings yet

- Semivariance MacrosDocument1 pageSemivariance MacroscociorvanmiriamNo ratings yet

- Curs 7 AuditDocument35 pagesCurs 7 AuditcociorvanmiriamNo ratings yet

- Planning, Understanding Risks and Materiality in Audit ProcessDocument33 pagesPlanning, Understanding Risks and Materiality in Audit ProcesscociorvanmiriamNo ratings yet

- ReportDocument314 pagesReportOnel FlorianNo ratings yet

- Curs 6 AuditDocument23 pagesCurs 6 Auditcociorvanmiriam100% (1)

- 2013-2014 Worldwide Personal Tax GuideDocument1,399 pages2013-2014 Worldwide Personal Tax GuideTony GallacherNo ratings yet

- Audit Curs 1Document42 pagesAudit Curs 1cociorvanmiriam100% (1)

- Audit Curs 3Document50 pagesAudit Curs 3cociorvanmiriamNo ratings yet

- Audit Curs 2Document31 pagesAudit Curs 2cociorvanmiriamNo ratings yet

- Audit Curs 1Document42 pagesAudit Curs 1cociorvanmiriam100% (1)

- Italy Vs Uk Tax ComplianceDocument7 pagesItaly Vs Uk Tax CompliancecociorvanmiriamNo ratings yet

- A Good Practice Guide To Co-Operation Between External and Internal AuditorsDocument47 pagesA Good Practice Guide To Co-Operation Between External and Internal AuditorscociorvanmiriamNo ratings yet

- LinksDocument1 pageLinkscociorvanmiriamNo ratings yet

- Banking System of EnglandDocument11 pagesBanking System of EnglandcociorvanmiriamNo ratings yet

- Romanian Malpractice CaseDocument2 pagesRomanian Malpractice CasecociorvanmiriamNo ratings yet

- Principles of Credit Risk ManagementDocument2 pagesPrinciples of Credit Risk ManagementcociorvanmiriamNo ratings yet

- Teme Lucrari de Licenta in Lb. Engleza 2014-2015Document2 pagesTeme Lucrari de Licenta in Lb. Engleza 2014-2015cociorvanmiriamNo ratings yet

- US GAAP Vs IFRSDocument52 pagesUS GAAP Vs IFRSSumair ShahidNo ratings yet

- Avon and OriflameDocument17 pagesAvon and OriflamecociorvanmiriamNo ratings yet

- Recipe Book and Autobiography by Colonel Harland SandersDocument184 pagesRecipe Book and Autobiography by Colonel Harland SandersAdam Buchnowski100% (3)

- Romanian Banking SystemDocument11 pagesRomanian Banking SystemcociorvanmiriamNo ratings yet

- Tehnici Curs 4 Intubatia OrotrahealaDocument5 pagesTehnici Curs 4 Intubatia OrotrahealacociorvanmiriamNo ratings yet

- Financial AccountingDocument20 pagesFinancial AccountingcociorvanmiriamNo ratings yet

- Statistics 1st YearDocument6 pagesStatistics 1st YearcociorvanmiriamNo ratings yet

- Inventories AccountingDocument15 pagesInventories AccountingcociorvanmiriamNo ratings yet

- Cash Book Practice QuesDocument3 pagesCash Book Practice Quesnehal dagarNo ratings yet

- Chapter 4 - : E-Commerce and Supply Chain ManagementDocument31 pagesChapter 4 - : E-Commerce and Supply Chain Managementkl25No ratings yet

- Consolidated Intercompany TransactionsDocument73 pagesConsolidated Intercompany TransactionsFatima AL-Sayed100% (1)

- Analisis Kinerja Rumah Sakit Berdasarkan Balanced Scorecard Di Rumah Sakit Umum Daerah Arifin Achmad Provinsi RiauDocument8 pagesAnalisis Kinerja Rumah Sakit Berdasarkan Balanced Scorecard Di Rumah Sakit Umum Daerah Arifin Achmad Provinsi RiauRizalNo ratings yet

- Bsa Midterm Exam - TaxDocument12 pagesBsa Midterm Exam - TaxHazel Grace PaguiaNo ratings yet

- Chapter 15 Multiple Choice Questions and ProblemsDocument14 pagesChapter 15 Multiple Choice Questions and Problemsmarycayton83% (6)

- Contoh LEMBAR KERJADocument57 pagesContoh LEMBAR KERJAKurikulum SMKN5PAlembangNo ratings yet

- BITS PILANI Operation Management SyllabusDocument12 pagesBITS PILANI Operation Management Syllabussap6370No ratings yet

- Test 3 ReviewDocument3 pagesTest 3 ReviewOmarSalehNo ratings yet

- 34318586Document8 pages34318586Gopesh ObalappaNo ratings yet

- Afar.3401 PartnershipDocument8 pagesAfar.3401 PartnershipEverly Mae ElondoNo ratings yet

- Acquisition and Payment CycleDocument19 pagesAcquisition and Payment CycleE-kel Anico Jaurigue67% (3)

- Https WWW - Cimb.bizchannel - Com.my Corp Front Transactioninquiry - Do Action DoPrintDocument1 pageHttps WWW - Cimb.bizchannel - Com.my Corp Front Transactioninquiry - Do Action DoPrintSyed HanafieNo ratings yet

- ISCEA Flyer 2023 - (NEW)Document17 pagesISCEA Flyer 2023 - (NEW)arubinaldoNo ratings yet

- Edgar Detoya Tax Consultant (Acca101)Document56 pagesEdgar Detoya Tax Consultant (Acca101)Hannah Pearl Flores VillarNo ratings yet

- 4PL Supply Chain Transformation SolutionsDocument2 pages4PL Supply Chain Transformation SolutionsGourav HegdeNo ratings yet

- Introduction For Scs Supplier Collaboration SystemDocument16 pagesIntroduction For Scs Supplier Collaboration SystemAwojobi Alexander Habeeb OloladeNo ratings yet

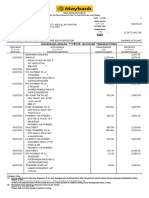

- Malayan Banking Berhad Savings Account StatementDocument16 pagesMalayan Banking Berhad Savings Account StatementhydaNo ratings yet

- Supply Chain Practice and Information SharingDocument18 pagesSupply Chain Practice and Information SharingUmang SoniNo ratings yet

- Built-Up Rates 2Document2 pagesBuilt-Up Rates 2Julian KitingNo ratings yet

- Bengkalis MuriaDocument10 pagesBengkalis Muriareza hariansyahNo ratings yet

- Business StrategiesDocument24 pagesBusiness StrategiesJohn Patrick Lazaro AndresNo ratings yet

- Basic Accounting Midterm ExamDocument11 pagesBasic Accounting Midterm ExamC J A SNo ratings yet

- Accounting Cycle Self Test QuestionsDocument6 pagesAccounting Cycle Self Test QuestionsFahad MushtaqNo ratings yet

- Abueg Clarence Angela R. Bsa1cDocument8 pagesAbueg Clarence Angela R. Bsa1cAnonnNo ratings yet

- R13.17D Financial OTBI Index ColumnsDocument224 pagesR13.17D Financial OTBI Index ColumnsNabeel RashidNo ratings yet

- Rekening Koran Permata IDRDocument2 pagesRekening Koran Permata IDRericksanjaya80% (5)

- Ch01 Managerial AccountingDocument7 pagesCh01 Managerial AccountingIrdo KwanNo ratings yet

- Basic Accounting Final ExamDocument7 pagesBasic Accounting Final ExamCharmae Agan Caroro75% (4)

- Chawla Parties Upto 14 Jan-19Document104 pagesChawla Parties Upto 14 Jan-19mudassar nazarNo ratings yet