You might also like

- Accounting and Finance-Based Measures of RiskDocument18 pagesAccounting and Finance-Based Measures of RiskshldhyNo ratings yet

- Mid MonthDocument4 pagesMid Monthcipollini50% (2)

- ASEAN Corporate Governance Scorecard Country Reports and Assessments 2019From EverandASEAN Corporate Governance Scorecard Country Reports and Assessments 2019No ratings yet

- Chapter 6 - Using Discounted Cash Flow Analysis To Make Investment DecisionsDocument14 pagesChapter 6 - Using Discounted Cash Flow Analysis To Make Investment DecisionsSheena Rhei Del RosarioNo ratings yet

- Fair Value Accounting: ©2018 John Wiley & Sons Australia LTDDocument42 pagesFair Value Accounting: ©2018 John Wiley & Sons Australia LTDSonia Dora DemoliaNo ratings yet

- A Contingency Framework For The Design of Accounting Information SystemDocument15 pagesA Contingency Framework For The Design of Accounting Information SystemAdeel RanaNo ratings yet

- Critical Financial Review: Understanding Corporate Financial InformationFrom EverandCritical Financial Review: Understanding Corporate Financial InformationNo ratings yet

- Muslim Entrepreneurship & Global Business Opportunities - MILE 2020Document3 pagesMuslim Entrepreneurship & Global Business Opportunities - MILE 2020Rizki Raja100% (1)

- A Study On Quality of Earnings in Petrochemical IndustryDocument9 pagesA Study On Quality of Earnings in Petrochemical IndustrySudheer KumarNo ratings yet

- Case 4Document11 pagesCase 4sulthanhakimNo ratings yet

- Mergers and Acquisitions DivestituresDocument42 pagesMergers and Acquisitions DivestituresEmie Rio Titular100% (1)

- Lecture 2 - Answer Part 2Document6 pagesLecture 2 - Answer Part 2Thắng ThôngNo ratings yet

- Accounting Chapt 15Document71 pagesAccounting Chapt 15karen_park1No ratings yet

- Accounting Information System - Chapter 2Document88 pagesAccounting Information System - Chapter 2Melisa May Ocampo AmpiloquioNo ratings yet

- What Is The Difference Between Book Value and Market ValueDocument12 pagesWhat Is The Difference Between Book Value and Market ValueAinie Intwines100% (1)

- Audit Committee Quality of EarningsDocument3 pagesAudit Committee Quality of EarningsJilesh PabariNo ratings yet

- Chap009 131230191204 Phpapp01Document41 pagesChap009 131230191204 Phpapp01AndrianMelmamBesyNo ratings yet

- Comprehensive Case Applying Financial Statement AnalysisDocument4 pagesComprehensive Case Applying Financial Statement AnalysisFerial FerniawanNo ratings yet

- Off Balance Sheet Transactions For Islamic BanksDocument25 pagesOff Balance Sheet Transactions For Islamic BanksSyed MohiuddinNo ratings yet

- Investment Banking Valuation - Equity Value - and Enterprise ValueDocument18 pagesInvestment Banking Valuation - Equity Value - and Enterprise ValuejyguygNo ratings yet

- Empirical Studies in FinanceDocument8 pagesEmpirical Studies in FinanceAhmedMalikNo ratings yet

- Comprehensive Case-Campbell SoupDocument9 pagesComprehensive Case-Campbell SoupIlham Muhammad AkbarNo ratings yet

- IAS 18 - Revenue PDFDocument12 pagesIAS 18 - Revenue PDFJanelle SentinaNo ratings yet

- Chap 012Document29 pagesChap 012azmiikptNo ratings yet

- Trade Off Between Relevance and ReliabilityDocument1 pageTrade Off Between Relevance and ReliabilitylciimNo ratings yet

- Charles P. Jones and Gerald R. Jensen, Investments: Analysis and Management, 13 Edition, John Wiley & SonsDocument17 pagesCharles P. Jones and Gerald R. Jensen, Investments: Analysis and Management, 13 Edition, John Wiley & SonsFebri MonikaNo ratings yet

- Free Cash Flow Valuation: Wacc FCFF VDocument6 pagesFree Cash Flow Valuation: Wacc FCFF VRam IyerNo ratings yet

- Chapter OneDocument18 pagesChapter OneBelsti AsresNo ratings yet

- 6.4-Case Study APA Paper 15-2 and 16-1 - Document For Financial Accounting TheoryDocument11 pages6.4-Case Study APA Paper 15-2 and 16-1 - Document For Financial Accounting TheorySMWNo ratings yet

- CH 03 Financial Statements ExercisesDocument39 pagesCH 03 Financial Statements ExercisesJocelyneKarolinaArriagaRangel100% (1)

- International Bond MarketDocument16 pagesInternational Bond MarketashishNo ratings yet

- Simon Chap. 5Document33 pagesSimon Chap. 5harum77No ratings yet

- Lakeside Jawaban CaseDocument40 pagesLakeside Jawaban CaseDhenayu Tresnadya HendrikNo ratings yet

- 02 Oct 2013 Fact SheetDocument1 page02 Oct 2013 Fact SheetfaisaladeemNo ratings yet

- Manajemen Keuangan - Merger and Acquisition PDFDocument36 pagesManajemen Keuangan - Merger and Acquisition PDFvrieskaNo ratings yet

- Case SPMDocument4 pagesCase SPMainiNo ratings yet

- Auditing - Hook Chapter 9 SolutionsDocument12 pagesAuditing - Hook Chapter 9 SolutionsZenni T XinNo ratings yet

- East Coast Yachts Goes InternationalDocument1 pageEast Coast Yachts Goes InternationalAries MayaNo ratings yet

- Kelompok 5 Soal TerjemahanDocument1 pageKelompok 5 Soal TerjemahanElgaNurhikmahNo ratings yet

- Tutorial A40 Kis Aktuaria/Materi TGL 15 A40Document40 pagesTutorial A40 Kis Aktuaria/Materi TGL 15 A40nirmalazintaNo ratings yet

- Eva & MvaDocument5 pagesEva & MvaVineet ChouhanNo ratings yet

- Case 15-5 Xerox Corporation RecommendationsDocument6 pagesCase 15-5 Xerox Corporation RecommendationsgabrielyangNo ratings yet

- PCL TVDocument4 pagesPCL TVEm MonteNo ratings yet

- Mac Session 15Document12 pagesMac Session 15Dhairya GuptaNo ratings yet

- Statement of Comprehensive Income (Income Statement)Document29 pagesStatement of Comprehensive Income (Income Statement)Alphan SofyanNo ratings yet

- Investment Analysis - Chapter 7Document36 pagesInvestment Analysis - Chapter 7Linh MaiNo ratings yet

- AIS Group 8 Report Chapter 17 Hand-OutDocument8 pagesAIS Group 8 Report Chapter 17 Hand-OutPoy GuintoNo ratings yet

- Bsz263432882inh PDFDocument4 pagesBsz263432882inh PDFMarsiniNo ratings yet

- Chapter 2 - Understanding StrategiesDocument31 pagesChapter 2 - Understanding StrategiesSarah Laras WitaNo ratings yet

- FSA 8e Ch04 SMDocument63 pagesFSA 8e Ch04 SMmonhelNo ratings yet

- Summary A Survey of Corporate Governance by Shleifer VishnyDocument61 pagesSummary A Survey of Corporate Governance by Shleifer VishnyAlayou Tefera100% (1)

- Managing MA RiskDocument14 pagesManaging MA RiskBartosz SobotaNo ratings yet

- Chapter 7 Analisis Laporan Keuangan SubramanyamDocument59 pagesChapter 7 Analisis Laporan Keuangan SubramanyamIbnu Wibowo100% (1)

- Ch17 Bond Yields and Prices Ch18 Bonds - Analysis and StrategyDocument47 pagesCh17 Bond Yields and Prices Ch18 Bonds - Analysis and StrategyCikini MentengNo ratings yet

- Analisis Kebangkrutan (Financial Distress) - JurnalDocument2 pagesAnalisis Kebangkrutan (Financial Distress) - JurnalAnnisa Dhia46No ratings yet

- CAMELS and PEARLS Applied To Financial Management of Commercial Bank in VietnamDocument44 pagesCAMELS and PEARLS Applied To Financial Management of Commercial Bank in VietnamDan LinhNo ratings yet

- SFM Chapter 7Document43 pagesSFM Chapter 7WilsonNo ratings yet

- The Product Portfolio PDFDocument5 pagesThe Product Portfolio PDFRami El TakiNo ratings yet

- M1 Foundation in Financial Planning and Tax Planning Syllabus FinalDocument10 pagesM1 Foundation in Financial Planning and Tax Planning Syllabus FinalCalvin YeohNo ratings yet

- The Basics of Capital Budgeting: MINI CASE SolutionDocument18 pagesThe Basics of Capital Budgeting: MINI CASE SolutionVinod MathewsNo ratings yet

- BHARATH SfinalDocument66 pagesBHARATH Sfinalaurorashiva1No ratings yet

- Contoh AnalisisDocument17 pagesContoh AnalisisNurnazihaNo ratings yet

- CH 2 SSQ Bak - Answers OnlyDocument8 pagesCH 2 SSQ Bak - Answers OnlypkehmerNo ratings yet

- Mini Case - Chapter 10Document6 pagesMini Case - Chapter 10mfitani75% (4)

- IRR, ERR and Payback - pptx-1470084967Document41 pagesIRR, ERR and Payback - pptx-1470084967Alexie GonzalesNo ratings yet

- Class Cases CH 13: Capital Budgeting Decisions: Year Investment Cash Inflow Unrecovered InvestmentDocument7 pagesClass Cases CH 13: Capital Budgeting Decisions: Year Investment Cash Inflow Unrecovered InvestmentDinatul FadhilaNo ratings yet

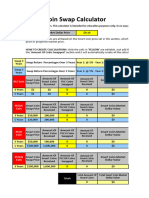

- Smart Coin Swap CalculatorDocument4 pagesSmart Coin Swap CalculatornktradzNo ratings yet

- Capital Investment Factors7to16Document15 pagesCapital Investment Factors7to16Spencer Tañada100% (1)

- AAII-My Investment Letter Words of Advice For My GrandchildrenDocument5 pagesAAII-My Investment Letter Words of Advice For My Grandchildrenbhaskar.jain20021814No ratings yet

- Jay Abraham - 9 Profit DriversDocument17 pagesJay Abraham - 9 Profit Driversmarketing_curator100% (5)

- Benefits of International Portfolio DiversificationDocument9 pagesBenefits of International Portfolio DiversificationflichuchaNo ratings yet

- Chapter 4 AnswersDocument9 pagesChapter 4 AnswersCDT MIKI EMERALD CUEVANo ratings yet

- Benchmarking BenchmarkDocument205 pagesBenchmarking Benchmarkharun hakshiNo ratings yet

- LP Formulation ProblemsDocument6 pagesLP Formulation Problemsmeetmak50% (2)

- CAT Investment AnalyisDocument12 pagesCAT Investment Analyisbrianmc1No ratings yet

- Final TheoTrade Summer SchoolDocument24 pagesFinal TheoTrade Summer Schoolliang yuanNo ratings yet

- Ratio Analysis of Beximco Pharmaceuticals LimitedDocument12 pagesRatio Analysis of Beximco Pharmaceuticals Limitedapi-3707335100% (4)

- Midterm NotesDocument32 pagesMidterm NotesGabriel Garza100% (2)

- FINANCE MANAGEMENT FIN420 CHP 2Document12 pagesFINANCE MANAGEMENT FIN420 CHP 2Yanty IbrahimNo ratings yet

- Company Analysis of Blue StarDocument42 pagesCompany Analysis of Blue Stardevika_namajiNo ratings yet

- FINS1613 File 02 - Bonds + Equities Additional Practice QuestionsDocument7 pagesFINS1613 File 02 - Bonds + Equities Additional Practice Questionsisy campbellNo ratings yet

- Notes On PrivatisationDocument64 pagesNotes On PrivatisationSwathi ShekarNo ratings yet

- Fama FrenchDocument47 pagesFama FrenchHamid UllahNo ratings yet

- T02 - Capital BudgetingDocument107 pagesT02 - Capital BudgetingSuehNo ratings yet

- 14239Document89 pages14239maxeytm_839061685No ratings yet

- Week 2-6 CFM SolutionsDocument32 pagesWeek 2-6 CFM SolutionsRalph MarquetaNo ratings yet

- Creative Abstract Watercolor: The beginner's guide to expressive and imaginative paintingFrom EverandCreative Abstract Watercolor: The beginner's guide to expressive and imaginative paintingRating: 3 out of 5 stars3/5 (1)

- The Lost Art of Handwriting: Rediscover the Beauty and Power of PenmanshipFrom EverandThe Lost Art of Handwriting: Rediscover the Beauty and Power of PenmanshipRating: 4.5 out of 5 stars4.5/5 (14)

- Drawing and Sketching Portraits: How to Draw Realistic Faces for BeginnersFrom EverandDrawing and Sketching Portraits: How to Draw Realistic Faces for BeginnersRating: 5 out of 5 stars5/5 (5)

- Beginner's Guide To Procreate: Characters: How to create characters on an iPad ®From EverandBeginner's Guide To Procreate: Characters: How to create characters on an iPad ®3dtotal PublishingRating: 4 out of 5 stars4/5 (1)

- Art Models Sam074: Figure Drawing Pose ReferenceFrom EverandArt Models Sam074: Figure Drawing Pose ReferenceRating: 4 out of 5 stars4/5 (1)

- Drawing: Flowers: Learn to Draw Step-by-StepFrom EverandDrawing: Flowers: Learn to Draw Step-by-StepRating: 5 out of 5 stars5/5 (2)

- Swatch This, 3000+ Color Palettes for Success: Perfect for Artists, Designers, MakersFrom EverandSwatch This, 3000+ Color Palettes for Success: Perfect for Artists, Designers, MakersRating: 3.5 out of 5 stars3.5/5 (3)

- Fundamentals of Character Design: How to Create Engaging Characters for Illustration, Animation & Visual DevelopmentFrom EverandFundamentals of Character Design: How to Create Engaging Characters for Illustration, Animation & Visual Development3dtotal PublishingRating: 5 out of 5 stars5/5 (2)

- Art Models Jesse222: Figure Drawing Pose ReferenceFrom EverandArt Models Jesse222: Figure Drawing Pose ReferenceRating: 3.5 out of 5 stars3.5/5 (3)

- Designa: Technical Secrets of the Traditional Visual ArtsFrom EverandDesigna: Technical Secrets of the Traditional Visual ArtsRating: 5 out of 5 stars5/5 (1)

- The Kew Gardens Botanical Artist: Learn to Draw and Paint Flowers in the Style of Pierre-Joseph RedoutéFrom EverandThe Kew Gardens Botanical Artist: Learn to Draw and Paint Flowers in the Style of Pierre-Joseph RedoutéNo ratings yet

- Art Models SarahAnn031: Figure Drawing Pose ReferenceFrom EverandArt Models SarahAnn031: Figure Drawing Pose ReferenceRating: 3 out of 5 stars3/5 (4)

- Ernst Haeckel's Art Forms in Nature: A Visual Masterpiece of the Natural WorldFrom EverandErnst Haeckel's Art Forms in Nature: A Visual Masterpiece of the Natural WorldNo ratings yet

- One Zentangle a Day: A 6-Week Course in Creative Drawing for Relaxation, Inspiration, and FunFrom EverandOne Zentangle a Day: A 6-Week Course in Creative Drawing for Relaxation, Inspiration, and FunRating: 4 out of 5 stars4/5 (25)

- Watercolor For The Soul: Simple painting projects for beginners, to calm, soothe and inspireFrom EverandWatercolor For The Soul: Simple painting projects for beginners, to calm, soothe and inspireRating: 5 out of 5 stars5/5 (6)

- Art Models AnaIv309: Figure Drawing Pose ReferenceFrom EverandArt Models AnaIv309: Figure Drawing Pose ReferenceRating: 3 out of 5 stars3/5 (2)

- Art Models KatarinaK034: Figure Drawing Pose ReferenceFrom EverandArt Models KatarinaK034: Figure Drawing Pose ReferenceRating: 3.5 out of 5 stars3.5/5 (3)

- Zentangle® Sourcebook: The ultimate resource for mindful drawingFrom EverandZentangle® Sourcebook: The ultimate resource for mindful drawingRating: 5 out of 5 stars5/5 (1)

- Just Draw Botanicals: Beautiful Botanical Art, Contemporary Artists, Modern MaterialsFrom EverandJust Draw Botanicals: Beautiful Botanical Art, Contemporary Artists, Modern MaterialsRating: 3.5 out of 5 stars3.5/5 (3)

- An Introduction to Hand Lettering with Decorative ElementsFrom EverandAn Introduction to Hand Lettering with Decorative ElementsRating: 4.5 out of 5 stars4.5/5 (7)

- Art Models Jenni001: Figure Drawing Pose ReferenceFrom EverandArt Models Jenni001: Figure Drawing Pose ReferenceRating: 5 out of 5 stars5/5 (1)

- Art Models Adrina032: Figure Drawing Pose ReferenceFrom EverandArt Models Adrina032: Figure Drawing Pose ReferenceRating: 5 out of 5 stars5/5 (2)