You might also like

- The Bankers Code Book PDFDocument202 pagesThe Bankers Code Book PDFOrdu Henry Onyebuchukwu100% (3)

- V35 C11 539leavDocument11 pagesV35 C11 539leavd1234d100% (1)

- Gs Lodging Industry Primer 2012Document103 pagesGs Lodging Industry Primer 2012crticoticoNo ratings yet

- Resume Book: Columbia Healthcare and Pharmaceutical Management ProgramDocument44 pagesResume Book: Columbia Healthcare and Pharmaceutical Management ProgramJohn Mathias100% (2)

- Phuket CaseDocument4 pagesPhuket Casejperez1980100% (1)

- Bonds and Their Valuation: Key Features of Bonds Bond Valuation Measuring YieldDocument34 pagesBonds and Their Valuation: Key Features of Bonds Bond Valuation Measuring YieldSyed Farzan AzharNo ratings yet

- SAPM Quiz 3Document137 pagesSAPM Quiz 3Netflix FlixNo ratings yet

- Bond ValuationDocument49 pagesBond ValuationMuhammad Saleh AliNo ratings yet

- 5 - Bond and Stock Valuation (Compatibility Mode)Document58 pages5 - Bond and Stock Valuation (Compatibility Mode)Ái Mỹ DuyênNo ratings yet

- EFM - MSESPM - Lec 4 - Bond & Share Valuation - 2019-20Document46 pagesEFM - MSESPM - Lec 4 - Bond & Share Valuation - 2019-20RabinNo ratings yet

- CH 4Document23 pagesCH 4Gizaw BelayNo ratings yet

- Bond AnalysisDocument45 pagesBond AnalysisAbhishekNo ratings yet

- Bond Mathematics ExplainedDocument35 pagesBond Mathematics Explainedrohan.explorerNo ratings yet

- Bonds, Stock and Their Valuation: Presented By: Irwan Rizki Basir Neela Osman YuningsihDocument68 pagesBonds, Stock and Their Valuation: Presented By: Irwan Rizki Basir Neela Osman YuningsihnensirsNo ratings yet

- Bonds and Their Valuation: Key Features of Bonds Bond Valuation Measuring Yield Assessing RiskDocument31 pagesBonds and Their Valuation: Key Features of Bonds Bond Valuation Measuring Yield Assessing Riskmkmu9No ratings yet

- Bonds and Their Valuation: Key Features of Bonds Bond Valuation Measuring Yield Assessing RiskDocument30 pagesBonds and Their Valuation: Key Features of Bonds Bond Valuation Measuring Yield Assessing Riskomar hashmiNo ratings yet

- Bonds, Bond Valuation, Interest Rates - Session 7 - 8Document19 pagesBonds, Bond Valuation, Interest Rates - Session 7 - 8anon_974035635No ratings yet

- FIS Assignment 1 Bitan SahaDocument6 pagesFIS Assignment 1 Bitan SahaBitan SahaNo ratings yet

- Investment Analysis & Portfolio Management: Bond Valuation: That Holding Period IsDocument5 pagesInvestment Analysis & Portfolio Management: Bond Valuation: That Holding Period IsNitesh KirarNo ratings yet

- Bonds and Their ValuationDocument36 pagesBonds and Their ValuationRubab BabarNo ratings yet

- Chapter 7 Interest Rates and Bond ValuationDocument18 pagesChapter 7 Interest Rates and Bond ValuationMai AnhNo ratings yet

- BFC5935 - Tutorial 7 SolutionsDocument4 pagesBFC5935 - Tutorial 7 SolutionsXue XuNo ratings yet

- FINA2004 Unit 7Document14 pagesFINA2004 Unit 7Taedia HibbertNo ratings yet

- Stocks and Bonds ValuationDocument82 pagesStocks and Bonds ValuationRonald MendozaNo ratings yet

- Chap010 StuDocument24 pagesChap010 StuBingbong Magluyan MonfielNo ratings yet

- Key Features of Bonds Bond Valuation Measuring Yield Assessing RiskDocument28 pagesKey Features of Bonds Bond Valuation Measuring Yield Assessing RiskShuja GhayasNo ratings yet

- Valuation of SecuritiesDocument53 pagesValuation of SecuritiesGaurav AgarwalNo ratings yet

- Sujoy Kumar Dhar Faculty Member IBS Business School, KolkataDocument17 pagesSujoy Kumar Dhar Faculty Member IBS Business School, KolkataAyesha KhanNo ratings yet

- Week 3 Valuation of Bonds and Bills: DFN 2013-Financial ManagementDocument34 pagesWeek 3 Valuation of Bonds and Bills: DFN 2013-Financial Managementkavi priyaNo ratings yet

- FBI Chapter - 6 Part 2Document9 pagesFBI Chapter - 6 Part 2Golam RamijNo ratings yet

- Revision MidtermDocument12 pagesRevision MidtermKim NgânNo ratings yet

- Bonds and Their Valuation: Key Features of Bonds Bond Valuation Measuring Yield Assessing RiskDocument30 pagesBonds and Their Valuation: Key Features of Bonds Bond Valuation Measuring Yield Assessing RiskMohamed HosnyNo ratings yet

- Fixed Income Securities GuideDocument8 pagesFixed Income Securities GuideOumer ShaffiNo ratings yet

- FM CH - IvDocument55 pagesFM CH - IvGizaw BelayNo ratings yet

- CHAPTER 7 Bonds and Their ValuationDocument43 pagesCHAPTER 7 Bonds and Their ValuationAhsan100% (2)

- Valuation of BondsDocument27 pagesValuation of BondsAbhinav Rajverma100% (1)

- Bond Issue by "Nabard"Document12 pagesBond Issue by "Nabard"Ravi SinghNo ratings yet

- Presentation 5 - Valuation of Bonds and Shares (Final)Document21 pagesPresentation 5 - Valuation of Bonds and Shares (Final)sanjuladasanNo ratings yet

- DM Theory Part 2Document40 pagesDM Theory Part 2Atharva GoreNo ratings yet

- Week 5 SlidesDocument37 pagesWeek 5 SlidesKarthik RamanathanNo ratings yet

- Bond ValuationDocument51 pagesBond ValuationRudy Putro100% (1)

- 1453975109ch 4 Bond ValuationDocument50 pages1453975109ch 4 Bond ValuationAshutoshNo ratings yet

- Commerce 308: Introduction To Finance: Bond Valuation & Interest RatesDocument47 pagesCommerce 308: Introduction To Finance: Bond Valuation & Interest RatesPamela Santos100% (1)

- Topic2 BondDocument37 pagesTopic2 Bond1033996544No ratings yet

- What Are Bonds?Document21 pagesWhat Are Bonds?ashish20gupta86No ratings yet

- 6-ch 18Document38 pages6-ch 18herueuxNo ratings yet

- Bonds and Their Valuation: Key Features of Bonds Bond Valuation Measuring Yield Assessing RiskDocument40 pagesBonds and Their Valuation: Key Features of Bonds Bond Valuation Measuring Yield Assessing RiskMSA-ACCA100% (2)

- Corporate Finance: Dr. A. DemaskeyDocument21 pagesCorporate Finance: Dr. A. DemaskeyrachealllNo ratings yet

- Lecture 7 BH CH 7 Bond and ValuationDocument41 pagesLecture 7 BH CH 7 Bond and ValuationAydin GaniyevNo ratings yet

- RepoDocument132 pagesRepoJiashen Charles GouNo ratings yet

- How To Value Bonds and Stocks: Corporate FinanceDocument40 pagesHow To Value Bonds and Stocks: Corporate FinanceNguyễn Thùy LinhNo ratings yet

- Bond Valuation and Yield CalculationsDocument27 pagesBond Valuation and Yield CalculationsOmar SerhalNo ratings yet

- Bond Valuation & Risk ChapterDocument23 pagesBond Valuation & Risk ChapterSheevun Di GulimanNo ratings yet

- Introduction to Fixed Income SecuritiesDocument44 pagesIntroduction to Fixed Income SecuritiesShahruzzaman AkashNo ratings yet

- Document Name Bond Math Version Number V1 Approved by Marisha Purohit Approval Date 03/05/2020 Creator Audience Students/Faculty/ManagementDocument20 pagesDocument Name Bond Math Version Number V1 Approved by Marisha Purohit Approval Date 03/05/2020 Creator Audience Students/Faculty/ManagementRavindra A. KamathNo ratings yet

- Bond Valuation and Yield CalculationsDocument26 pagesBond Valuation and Yield Calculationslibison1No ratings yet

- Bond Yields DurationDocument18 pagesBond Yields DurationKaranbir Singh RandhawaNo ratings yet

- Booth Cleary 2nd Edition Chapter 6 - Bond Valuation and Interest RatesDocument93 pagesBooth Cleary 2nd Edition Chapter 6 - Bond Valuation and Interest RatesQurat.ul.ain MumtazNo ratings yet

- Introduction To BondsDocument5 pagesIntroduction To BondsHuu Duy100% (1)

- Chapter 4 Cont..Document30 pagesChapter 4 Cont..Lan Nhi NguyenNo ratings yet

- Lecture 4 Macro Analysis Bond MarketsDocument43 pagesLecture 4 Macro Analysis Bond MarketsOnyee FongNo ratings yet

- Fixed Income Securities: A Beginner's Guide to Understand, Invest and Evaluate Fixed Income Securities: Investment series, #2From EverandFixed Income Securities: A Beginner's Guide to Understand, Invest and Evaluate Fixed Income Securities: Investment series, #2No ratings yet

- P 20 BV Marathon Notes Divya AgarwalDocument36 pagesP 20 BV Marathon Notes Divya AgarwalrayNo ratings yet

- Momentum PicksDocument27 pagesMomentum Picksashokdb2kNo ratings yet

- Rochefort & Associés - General Overview - March 2021 - AcropolisDocument10 pagesRochefort & Associés - General Overview - March 2021 - AcropolisHangyu LvNo ratings yet

- Elliott Wave CalculatorDocument11 pagesElliott Wave CalculatorthairckshanNo ratings yet

- 14.1 Equity Versus Debt Financing: Capital Structure in A Perfect MarketDocument5 pages14.1 Equity Versus Debt Financing: Capital Structure in A Perfect MarketAlexandre LNo ratings yet

- Port Folio Number 2007 MASDocument8 pagesPort Folio Number 2007 MASSasa LuNo ratings yet

- WEF Alternative Investments 2020 FutureDocument59 pagesWEF Alternative Investments 2020 FutureOwenNo ratings yet

- Regulations On Fdi, Adr, GDR, Idr, Fii &ecbDocument59 pagesRegulations On Fdi, Adr, GDR, Idr, Fii &ecbAvinash SinghNo ratings yet

- Cash Management and Working Capital ProblemsDocument2 pagesCash Management and Working Capital ProblemsRachel RiveraNo ratings yet

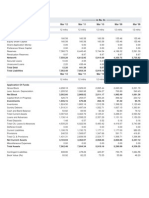

- Balance Sheet and P&L of CiplaDocument2 pagesBalance Sheet and P&L of CiplaPratik AhluwaliaNo ratings yet

- An Analysis of Demat Account and Online TradingDocument90 pagesAn Analysis of Demat Account and Online TradingNITIKESH GORIWALENo ratings yet

- Fullpaper Icopss2017 PDFDocument1,095 pagesFullpaper Icopss2017 PDFNurul AidaNo ratings yet

- Chapter 9: FOREX MARKET Key PointsDocument6 pagesChapter 9: FOREX MARKET Key PointsDanica AbelardoNo ratings yet

- Profitplan Year0Document3 pagesProfitplan Year0Kurth ReyesNo ratings yet

- 2014-16 Beer Store Strategic PlanDocument23 pages2014-16 Beer Store Strategic PlanannachlebowskaNo ratings yet

- Kekra-01 220119Document8 pagesKekra-01 220119rastamanrmNo ratings yet

- Introduction to Currency Trading: The Ultimate Beginner's GuideDocument25 pagesIntroduction to Currency Trading: The Ultimate Beginner's Guidearunchary007No ratings yet

- SIMPLE INTEREST COMPLETE CHAPTERDocument81 pagesSIMPLE INTEREST COMPLETE CHAPTERarobindatictNo ratings yet

- Direct Lenders First Real Test: Deloitte Alternative Lender Deal Tracker Spring 2020Document56 pagesDirect Lenders First Real Test: Deloitte Alternative Lender Deal Tracker Spring 2020fjdglf klfdNo ratings yet

- Full Download Strategic Marketing 10th Edition Cravens Test BankDocument35 pagesFull Download Strategic Marketing 10th Edition Cravens Test Banklevidelpnrr100% (34)

- Maruti Suzuki India 030522 KRDocument6 pagesMaruti Suzuki India 030522 KRVala UttamNo ratings yet

- International Arbitrage and Interest Rate Parity Chapter 7 Flashcards - QuizletDocument11 pagesInternational Arbitrage and Interest Rate Parity Chapter 7 Flashcards - QuizletDa Dark PrinceNo ratings yet

- Introduction To Point & Figure and Candle Charting MamualDocument22 pagesIntroduction To Point & Figure and Candle Charting Mamualesthermays50% (4)

- Chapter 38 - Teacher's ManualDocument27 pagesChapter 38 - Teacher's ManualHohoho67% (6)

- Trustline Summer Training Report PresentationDocument27 pagesTrustline Summer Training Report Presentationatul kumar100% (1)