You might also like

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Vodafone Payment ReceiptDocument1 pageVodafone Payment ReceiptRahul ManwatkarNo ratings yet

- Your Dojo Invoice: 06 Mar To 05 Apr 2023 (31 Days)Document3 pagesYour Dojo Invoice: 06 Mar To 05 Apr 2023 (31 Days)Helen KingNo ratings yet

- Brandon ClayshootDocument1 pageBrandon ClayshootbgctampaNo ratings yet

- WWW - Bankofindia.co - in UserFiles File DebitCumATMCardApplicationDocument1 pageWWW - Bankofindia.co - in UserFiles File DebitCumATMCardApplicationSiddharth ShanbhogueNo ratings yet

- Monthly StatementDocument2 pagesMonthly StatementYuniioor UrbaezNo ratings yet

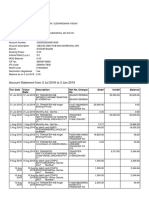

- Tanggal Uraian Transaksi Nominal Transaksi SaldoDocument4 pagesTanggal Uraian Transaksi Nominal Transaksi SaldoKBLH gamingNo ratings yet

- 1.04.21 - 31.03.22 CanaraDocument14 pages1.04.21 - 31.03.22 CanaraMADHUBALA SAHAYNo ratings yet

- Credit Card Details VCCGenerator OrgDocument4 pagesCredit Card Details VCCGenerator Orga.dockery01010167% (3)

- Application Form For DBP Prepaid CardDocument1 pageApplication Form For DBP Prepaid CardNOr JOe Sanidad50% (2)

- TRUWORTHSDocument1 pageTRUWORTHSridbastraNo ratings yet

- New VBM Acq Merchant 62714 v5Document3 pagesNew VBM Acq Merchant 62714 v5Yan Naing SoeNo ratings yet

- Sample Medical BillDocument1 pageSample Medical Billmiranda criggerNo ratings yet

- Bunna International Bank S.C Debit Card Personalization RequestDocument16 pagesBunna International Bank S.C Debit Card Personalization RequestSolomon TekalignNo ratings yet

- Gringa SsssDocument44 pagesGringa Ssssefrain ramos50% (2)

- Statement of Account: 70 JALAN AU 4/1 Taman Sri Keramat Tengah 54200 Ampang, WP Kuala LumpurDocument9 pagesStatement of Account: 70 JALAN AU 4/1 Taman Sri Keramat Tengah 54200 Ampang, WP Kuala LumpurLYE ManagementNo ratings yet

- Client Number: BSB Number: Orange Everyday Number: Statement Number: Statement FromDocument23 pagesClient Number: BSB Number: Orange Everyday Number: Statement Number: Statement FromJoseph JaeKwon KimNo ratings yet

- Regristration Form Regristration Form: No.002 - No.002Document1 pageRegristration Form Regristration Form: No.002 - No.002flailaNo ratings yet

- Society Attitude Towards Debit and Credit CardsDocument76 pagesSociety Attitude Towards Debit and Credit Cardskaran chaware100% (1)

- BCA ECR Documentation Fase IIIDocument70 pagesBCA ECR Documentation Fase IIIliko anas setyawatiNo ratings yet

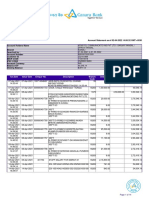

- Account Statement From 3 Jul 2018 To 3 Jan 2019: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument8 pagesAccount Statement From 3 Jul 2018 To 3 Jan 2019: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceGopagani DharshanNo ratings yet

- Receipts GasDocument21 pagesReceipts Gasbijan8261No ratings yet

- Account Name Account Number Transaction Date Year Transaction AmountDocument6 pagesAccount Name Account Number Transaction Date Year Transaction AmountSahara ReportersNo ratings yet

- ATM Card InfoDocument3 pagesATM Card Infojack meoffNo ratings yet

- Transaction StatementDocument10 pagesTransaction Statementsukeshsree sree33% (3)

- DNC-05 Clara Patricia (Kel 12)Document24 pagesDNC-05 Clara Patricia (Kel 12)clara_patricia_2No ratings yet

- Customer Name Card Account No MR Gundekari Vamshi Krishna 4375 XXXX XXXX 9005Document7 pagesCustomer Name Card Account No MR Gundekari Vamshi Krishna 4375 XXXX XXXX 9005vmshiNo ratings yet

- Ej S1DPRIR006 20230829Document373 pagesEj S1DPRIR006 20230829mhdluth5No ratings yet

- Statement of Account: Transaction Date Description Debit Credit Available BalanceDocument3 pagesStatement of Account: Transaction Date Description Debit Credit Available BalanceRashid ShahNo ratings yet

- Cashier Audit 09-AugDocument3 pagesCashier Audit 09-AugRoberto LamasNo ratings yet

- July MIS 2018Document154 pagesJuly MIS 2018Saurav sharmaNo ratings yet