You might also like

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Sample Questions Level IDocument31 pagesSample Questions Level IWong Yun Feng Marco100% (1)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- These Notes Are A Synthesis of Ideas Presented in The Following BooksDocument35 pagesThese Notes Are A Synthesis of Ideas Presented in The Following BooksANo ratings yet

- Chapter 8Document19 pagesChapter 8Benny Khor100% (2)

- 16 x11 FinMan DDocument8 pages16 x11 FinMan DErwin Cajucom50% (2)

- Case Submission - Stone Container Corporation (A) ' Group VIIIDocument5 pagesCase Submission - Stone Container Corporation (A) ' Group VIIIGURNEET KAURNo ratings yet

- Internal CommunicationDocument11 pagesInternal Communicationanks0909No ratings yet

- LeveragesDocument51 pagesLeveragesmaitrisharma131295100% (1)

- Fincorp managers' focus on long-term valueDocument56 pagesFincorp managers' focus on long-term valueJuanaArbuluMuñozNo ratings yet

- Calculating Financial Ratios and FiguresDocument27 pagesCalculating Financial Ratios and Figuresanks0909100% (2)

- Sourcing Strategies - ITDocument29 pagesSourcing Strategies - ITanks09090% (1)

- Modeling Financial Performance of NBFCsDocument44 pagesModeling Financial Performance of NBFCsgaurav kulkarni100% (2)

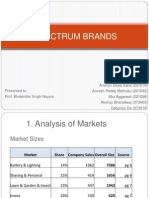

- Group 4 analysis of Spectrum Brands markets, competitors, and impact of changes on sales staffDocument7 pagesGroup 4 analysis of Spectrum Brands markets, competitors, and impact of changes on sales staffanks0909No ratings yet

- FMG 22A Idea TreeDocument3 pagesFMG 22A Idea Treeanks0909No ratings yet

- Assembly Line Balancing Example - Assembly of Electric IronDocument2 pagesAssembly Line Balancing Example - Assembly of Electric Ironanks0909No ratings yet

- Anurag IdeaTree221031Document3 pagesAnurag IdeaTree221031anks0909No ratings yet

- Assembly Line Balancing Example - Assembly of Electric IronDocument2 pagesAssembly Line Balancing Example - Assembly of Electric Ironanks0909No ratings yet

- ITC Financial Statement AnalysisDocument19 pagesITC Financial Statement Analysisanks0909No ratings yet

- Current Ratio Current Asset/current Liabilities Current Ratio 862.09/1120.81Document1 pageCurrent Ratio Current Asset/current Liabilities Current Ratio 862.09/1120.81anks0909No ratings yet

- Credit Management HandbookDocument48 pagesCredit Management HandbookNauman Rashid67% (6)

- Financial Institutions and Market: Commercial BankDocument60 pagesFinancial Institutions and Market: Commercial BankJayashree KowtalNo ratings yet

- Financial Analysis: Cross-sectional and time-series analysisDocument15 pagesFinancial Analysis: Cross-sectional and time-series analysisPooja MehraNo ratings yet

- Financial Management LEVERAGE PDFDocument28 pagesFinancial Management LEVERAGE PDFArmand RoblesNo ratings yet

- CFA Level I 2019 2020 Program ChangesDocument2 pagesCFA Level I 2019 2020 Program Changesweeliyen5754No ratings yet

- Toilet Case Study Final V1.0Document9 pagesToilet Case Study Final V1.0Rajas ShahadeNo ratings yet

- Question and Answer - 53Document30 pagesQuestion and Answer - 53acc-expertNo ratings yet

- Financial Ratios Topic (MFP 1) PDFDocument9 pagesFinancial Ratios Topic (MFP 1) PDFsrinivasa annamayyaNo ratings yet

- CHP 5-Week 6Document3 pagesCHP 5-Week 6farah aliNo ratings yet

- Phil Mosley and Rolando Shannon Financial RatiosDocument12 pagesPhil Mosley and Rolando Shannon Financial Ratiosapi-282888108No ratings yet

- ACC501 Solved MCQsDocument19 pagesACC501 Solved MCQsZeshan HaiderNo ratings yet

- Barclays SELLDocument16 pagesBarclays SELLbrucepackard3948No ratings yet

- Project Report ON A Comprehensive Study of Indian Banking SystemDocument55 pagesProject Report ON A Comprehensive Study of Indian Banking Systemkaushal2442No ratings yet

- Allagapp Dde SylabusDocument304 pagesAllagapp Dde SylabusAmol MahajanNo ratings yet

- Indias Leading BFSI Companies 2017Document244 pagesIndias Leading BFSI Companies 2017rohit sharma100% (1)

- Pershing Square Q1 12 Investor LetterDocument14 pagesPershing Square Q1 12 Investor LetterVALUEWALK LLCNo ratings yet

- RAP 20 ChobeDocument34 pagesRAP 20 ChobeSusan GomezNo ratings yet

- Assignment 1 Islamic Vs Conventional Banks Performance AnalysisDocument8 pagesAssignment 1 Islamic Vs Conventional Banks Performance AnalysisWali AfridiNo ratings yet

- Condensed Chapter 11 SlidesDocument20 pagesCondensed Chapter 11 SlidesrabharaNo ratings yet

- Antipodes Global Investment Company Limited prospectus for up to 200 million sharesDocument100 pagesAntipodes Global Investment Company Limited prospectus for up to 200 million sharesAnonymous FiAN6MiuNo ratings yet

- Zaini Zain (BAF2009012) Adv. Fin. Acc Group Assignment (UPDATED)Document23 pagesZaini Zain (BAF2009012) Adv. Fin. Acc Group Assignment (UPDATED)Zaini ZainNo ratings yet

- Sid - Sbi Magnum Equity Esg Fund PDFDocument90 pagesSid - Sbi Magnum Equity Esg Fund PDFTushar KZNo ratings yet