You might also like

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Chapter 12, Globalization: 2001 Prentice Hall, Inc. All Rights ReservedDocument36 pagesChapter 12, Globalization: 2001 Prentice Hall, Inc. All Rights ReservedJennifer Gabrielle IrawanNo ratings yet

- Chapter 16, Online Banking and Investing: OutlineDocument42 pagesChapter 16, Online Banking and Investing: OutlineJennifer Gabrielle IrawanNo ratings yet

- Chapter 14, Accessibility: OutlineDocument51 pagesChapter 14, Accessibility: OutlineJennifer Gabrielle IrawanNo ratings yet

- Chapter 18, E-Publishing: 2001 Prentice Hall, Inc. All Rights ReservedDocument21 pagesChapter 18, E-Publishing: 2001 Prentice Hall, Inc. All Rights ReservedJennifer Gabrielle IrawanNo ratings yet

- Chapter 19, Online Entertainment: 2001 Prentice Hall, Inc. All Rights ReservedDocument23 pagesChapter 19, Online Entertainment: 2001 Prentice Hall, Inc. All Rights ReservedJennifer Gabrielle IrawanNo ratings yet

- Chapter 20, Online Career Services: 2001 Prentice Hall, Inc. All Rights ReservedDocument22 pagesChapter 20, Online Career Services: 2001 Prentice Hall, Inc. All Rights ReservedJennifer Gabrielle IrawanNo ratings yet

- Capital: Microeconomic TheoryDocument67 pagesCapital: Microeconomic TheoryJennifer Gabrielle IrawanNo ratings yet

- KOTCHA06Document9 pagesKOTCHA06Jennifer Gabrielle IrawanNo ratings yet

- Externalities and Public Goods: Microeconomic TheoryDocument71 pagesExternalities and Public Goods: Microeconomic TheoryJennifer Gabrielle IrawanNo ratings yet

- Political Economics: Microeconomic TheoryDocument67 pagesPolitical Economics: Microeconomic TheoryJennifer Gabrielle IrawanNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

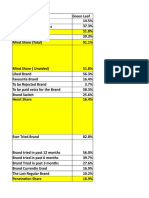

- Brand Health Analysis TemplateDocument4 pagesBrand Health Analysis Templateanon_493704527No ratings yet

- PindoudouDocument10 pagesPindoudouthuyanhnguyen164.workNo ratings yet

- Bursa Malaysia Report PDFDocument9 pagesBursa Malaysia Report PDFIeyrah Rah ElisyaNo ratings yet

- Finance pt2 QB NEWDocument71 pagesFinance pt2 QB NEWBharath BMNo ratings yet

- Dendrite International: Group No-5 Alok Pratap Singh (23NMP05) Mohan Murari (23NMP19) Sudhansu Senapati (23NMP31)Document7 pagesDendrite International: Group No-5 Alok Pratap Singh (23NMP05) Mohan Murari (23NMP19) Sudhansu Senapati (23NMP31)Rahul NiranwalNo ratings yet

- Vodacoin Is The Product Selected To Implement in The Rwandese MarketDocument3 pagesVodacoin Is The Product Selected To Implement in The Rwandese MarketHamza ZainNo ratings yet

- USJ-R College of Commerce - Acctg 101 RM 403 MWF 8:30 AM - 10:30 AM - NEF, CPADocument3 pagesUSJ-R College of Commerce - Acctg 101 RM 403 MWF 8:30 AM - 10:30 AM - NEF, CPAJerah Marie PepitoNo ratings yet

- Customer Service in Supply Chain ManagementDocument9 pagesCustomer Service in Supply Chain ManagementRaghavendra KaladiNo ratings yet

- Marketing & Brand Building of Educomp Leap PVT LTD: (Summer Internship Project Report ON)Document63 pagesMarketing & Brand Building of Educomp Leap PVT LTD: (Summer Internship Project Report ON)Shiraz MalhotraNo ratings yet

- Business Proposal-Sisal FarmersDocument1 pageBusiness Proposal-Sisal FarmersSCHAEFFER CAPITAL ADVISORSNo ratings yet

- Entrepreneur Development NotesDocument20 pagesEntrepreneur Development NotesAnish YadavNo ratings yet

- Chapter 6 Noncurrent Asset Held For SaleDocument6 pagesChapter 6 Noncurrent Asset Held For SaleCarrie DangNo ratings yet

- Please Use The Sharing Tools Found Via The Share Button at The Top or Side of ArticlesDocument2 pagesPlease Use The Sharing Tools Found Via The Share Button at The Top or Side of ArticlesMarcela FernandezNo ratings yet

- Essay Test ECO 111 - IB1717Document4 pagesEssay Test ECO 111 - IB1717Phan Thị Thanh ThảoNo ratings yet

- Future GroupDocument7 pagesFuture GroupAbhay Pratap SinghNo ratings yet

- Aos287-2951631991 (ABET)Document9 pagesAos287-2951631991 (ABET)Elisabet Permata SariNo ratings yet

- Amazon Wholefood MergerDocument4 pagesAmazon Wholefood MergerGemaAkbarRamadhaniNo ratings yet

- Corporate Governance in India: Recent Developments in Governance Practice in Indian CorporatesDocument42 pagesCorporate Governance in India: Recent Developments in Governance Practice in Indian CorporatesArcha ShajiNo ratings yet

- Airborne Express Case StudyDocument10 pagesAirborne Express Case StudyNotesfreeBookNo ratings yet

- Technical Analysis of The Financial Markets - A Comprehensive Guide To Trading Methods and Applications by John J. Murphy (1999)Document582 pagesTechnical Analysis of The Financial Markets - A Comprehensive Guide To Trading Methods and Applications by John J. Murphy (1999)gss34gs432gw2agNo ratings yet

- SWOT Analysis For A BankDocument2 pagesSWOT Analysis For A BankAndrew Hoth KangNo ratings yet

- Product Life CycleDocument3 pagesProduct Life CycleHarry LobleNo ratings yet

- BCG and GeDocument30 pagesBCG and GeNishikant RanaNo ratings yet

- Assignment On Launching Aarong in Canada: Submitted ToDocument14 pagesAssignment On Launching Aarong in Canada: Submitted ToEnaiya IslamNo ratings yet

- Business Plan Giga Bubble by AsmilDocument3 pagesBusiness Plan Giga Bubble by AsmilAnonymous cu5JFkINo ratings yet

- Samsung GalaxyDocument1 pageSamsung Galaxykumar gaurav100% (2)

- Chapter 3 E28093 Analysing The Market EnvironmentDocument2 pagesChapter 3 E28093 Analysing The Market EnvironmentAbdullah100% (1)

- Inventory Management Technique in Pharma Industry..Document14 pagesInventory Management Technique in Pharma Industry..Ilayaraja BoopathyNo ratings yet

- 2M00155Document7 pages2M00155Dhiraj PalNo ratings yet

- CHAPTER 10 - Inventory ManagementDocument15 pagesCHAPTER 10 - Inventory ManagementAaminah BeathNo ratings yet