You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- CH 8Document68 pagesCH 8sultan sultanNo ratings yet

- Incoterms® 2010, Will Be Launched in September and Come Into Effect On 1 January 2011Document3 pagesIncoterms® 2010, Will Be Launched in September and Come Into Effect On 1 January 2011Neha SinghNo ratings yet

- 11 Accounting For Merchandising Businesses Part 1Document15 pages11 Accounting For Merchandising Businesses Part 1Aple Balisi100% (1)

- Chapter 10 - Intermediate AccountingDocument4 pagesChapter 10 - Intermediate AccountingPrincess PriyaNo ratings yet

- A141 Tutorial 4 Bkal1013Document6 pagesA141 Tutorial 4 Bkal1013CyrilraincreamNo ratings yet

- Audit of InventoriesDocument2 pagesAudit of InventoriesJenny BernardinoNo ratings yet

- Test Bank Chap 1 14Document200 pagesTest Bank Chap 1 14Ánh Lê Thị NgọcNo ratings yet

- Chapter 3 Effects of Contract When The Thing Sold Has Been LostDocument4 pagesChapter 3 Effects of Contract When The Thing Sold Has Been LostApple Ke-eNo ratings yet

- Insul8 BarDocument12 pagesInsul8 BarRichard DeNijsNo ratings yet

- Damodaram Sanjivayya Sabbavaram, Visakhapatnam, Ap., India.: National Law UniversityDocument17 pagesDamodaram Sanjivayya Sabbavaram, Visakhapatnam, Ap., India.: National Law UniversityJahnavi GopaluniNo ratings yet

- Vics 850Document138 pagesVics 850EdNo ratings yet

- Corrected Draft 0215 PDFDocument4 pagesCorrected Draft 0215 PDFNadia Akhter AakhiNo ratings yet

- Oracle Purchasing User's Guide-3Document23 pagesOracle Purchasing User's Guide-3nanindwNo ratings yet

- Steam Coal Price: Indonesian Version Product ListDocument4 pagesSteam Coal Price: Indonesian Version Product ListIrfan Nasution MhdNo ratings yet

- Module 4 Loans and ReceivablesDocument55 pagesModule 4 Loans and Receivableschuchu tvNo ratings yet

- Manual - Cable Reels 1200 SeriesDocument22 pagesManual - Cable Reels 1200 Seriesjray1982No ratings yet

- PDF 2014 05 PRTC Audp Lecs Ap1601 Audit of InventoriespdfDocument10 pagesPDF 2014 05 PRTC Audp Lecs Ap1601 Audit of InventoriespdfCpaNo ratings yet

- Anu-291-Yunus Textile-Karachi-Fabric-1050tc-Cvc-Poly Cotton-40-Dbk-IcdDocument3 pagesAnu-291-Yunus Textile-Karachi-Fabric-1050tc-Cvc-Poly Cotton-40-Dbk-IcdthetaauNo ratings yet

- FAR Freight ChargesDocument2 pagesFAR Freight ChargesJaybie John Palco Eralino100% (1)

- Exam On Foreign Currency Transaction 40Document6 pagesExam On Foreign Currency Transaction 40nigusNo ratings yet

- ACC 1 Quiz No. 14 Answer KeyDocument9 pagesACC 1 Quiz No. 14 Answer Keynicole bancoroNo ratings yet

- Practice To Chapter 6 Part 1-4Document22 pagesPractice To Chapter 6 Part 1-4Gulzhan AmanbaikyzyNo ratings yet

- Chapter 8 Part 1-Accounts Receivables: Don Honorio Ventura State University College of Business StudiesDocument4 pagesChapter 8 Part 1-Accounts Receivables: Don Honorio Ventura State University College of Business StudiesKyleRhayneDiazCaliwagNo ratings yet

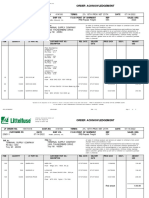

- Order Acknowledgement: Customer Po Date Ship Via F.O.B Point of Shipment REP Sales Org LF Order No. Cust - No. Terms: DateDocument2 pagesOrder Acknowledgement: Customer Po Date Ship Via F.O.B Point of Shipment REP Sales Org LF Order No. Cust - No. Terms: DateJe-Ann Tabo-taboNo ratings yet

- C 5 & 6 F Modes of Delivery Actual Delivery Constructive DeliveryDocument5 pagesC 5 & 6 F Modes of Delivery Actual Delivery Constructive DeliveryKrystoffer YapNo ratings yet

- Weygandt J (2019) - Accounting Principles IFRS Version c06Document46 pagesWeygandt J (2019) - Accounting Principles IFRS Version c06Kirsten Rae SuaverdezNo ratings yet

- MMSDocument23 pagesMMSDrBollapu SudarshanNo ratings yet

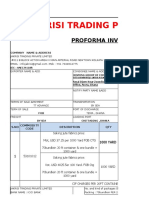

- Export Proforma Ghana 24.4.2019 JKPL 003Document5 pagesExport Proforma Ghana 24.4.2019 JKPL 003SAMRAT SILNo ratings yet

- DocxDocument25 pagesDocxPhilip Castro67% (3)

- Inventories: Chapter 8: Theory of Accounts ReviewerDocument25 pagesInventories: Chapter 8: Theory of Accounts ReviewerYuki100% (1)