You might also like

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Fidelity Multi-Sector Bond Fund - ENDocument3 pagesFidelity Multi-Sector Bond Fund - ENdpbasicNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- 2016 WB 2578 QuantInsti ImplementAlgoTradingCodedinPythonNotesDocument40 pages2016 WB 2578 QuantInsti ImplementAlgoTradingCodedinPythonNotesBartoszSowulNo ratings yet

- Trading Plan Small ACCOUNTDocument62 pagesTrading Plan Small ACCOUNTAndrew100% (3)

- BFS L0 Ques464Document360 pagesBFS L0 Ques464Aayush AgrawalNo ratings yet

- Evaluation Chapter 11 LBO M&ADocument32 pagesEvaluation Chapter 11 LBO M&AShan KumarNo ratings yet

- Pertemuan 11 - EkuitasDocument34 pagesPertemuan 11 - EkuitasCristian Kumara PutraNo ratings yet

- AMFI Mutual Fund (Advisor) Module: Preparatory Training ProgramDocument231 pagesAMFI Mutual Fund (Advisor) Module: Preparatory Training Programallmutualfund100% (5)

- Kalyan Jewellers HSBC 3oct2022Document33 pagesKalyan Jewellers HSBC 3oct2022Ankk Tenderz100% (1)

- Investment OverviewDocument6 pagesInvestment OverviewPinkyChoudharyNo ratings yet

- Efficient Front. Capital Market LineDocument5 pagesEfficient Front. Capital Market LinePinkyChoudharyNo ratings yet

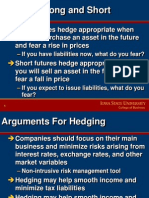

- HedgingDocument11 pagesHedgingPinkyChoudhary50% (2)

- Portfolio Return and RiskDocument4 pagesPortfolio Return and RiskPinkyChoudharyNo ratings yet

- CTPDocument12 pagesCTPPinkyChoudharyNo ratings yet

- Assignment FDDocument1 pageAssignment FDPinkyChoudharyNo ratings yet

- Group Dynamics: Ajay Kumar SainiDocument45 pagesGroup Dynamics: Ajay Kumar SainiPinkyChoudharyNo ratings yet

- Question On SMDocument1 pageQuestion On SMPinkyChoudharyNo ratings yet

- Single Index ModelDocument3 pagesSingle Index ModelPinkyChoudhary100% (1)

- Group Dynamics: Ajay Kumar SainiDocument45 pagesGroup Dynamics: Ajay Kumar SainiPinkyChoudharyNo ratings yet

- Portfolio Return and RiskDocument4 pagesPortfolio Return and RiskPinkyChoudharyNo ratings yet

- Project ReportDocument73 pagesProject ReportPinkyChoudharyNo ratings yet

- Systematic Risk Unsystematic Risk: Market-Wide Company-WideDocument2 pagesSystematic Risk Unsystematic Risk: Market-Wide Company-WidePinkyChoudharyNo ratings yet

- A Study of Application of ERP Software ForDocument8 pagesA Study of Application of ERP Software ForPinkyChoudharyNo ratings yet

- Efficient Front. Capital Market LineDocument5 pagesEfficient Front. Capital Market LinePinkyChoudharyNo ratings yet

- South AfricaDocument14 pagesSouth AfricaPinkyChoudharyNo ratings yet

- Chapter 7-10Document8 pagesChapter 7-10Jolina T. OrongNo ratings yet

- AxasxDocument26 pagesAxasxГал БадрахNo ratings yet

- Metallgesellschaft Brief SolutionsDocument2 pagesMetallgesellschaft Brief SolutionsarunzexyNo ratings yet

- BMAN23000 Online Exam 2019-20Document5 pagesBMAN23000 Online Exam 2019-20Munkbileg MunkhtsengelNo ratings yet

- Busi431 - Formative Assessment 1Document4 pagesBusi431 - Formative Assessment 1hamzaNo ratings yet

- Chapter 19 - OptionsDocument23 pagesChapter 19 - OptionsSehrish Atta0% (1)

- Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument65 pagesDate Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceMohan KumarNo ratings yet

- ER - Assignment # 2 - VaibhavGuptaDocument3 pagesER - Assignment # 2 - VaibhavGuptaVaibhav Gupta0% (1)

- Postal Ballot Notice - ZELDocument10 pagesPostal Ballot Notice - ZELCSNo ratings yet

- 5301 Ch. 7-14 Additional Multiple Choice QuestionsDocument9 pages5301 Ch. 7-14 Additional Multiple Choice QuestionsZhou Tian YangNo ratings yet

- International Journal of Business and Management Invention (IJBMI)Document8 pagesInternational Journal of Business and Management Invention (IJBMI)inventionjournalsNo ratings yet

- Security Analysis and Portfolio Management: Question BankDocument12 pagesSecurity Analysis and Portfolio Management: Question BankgiteshNo ratings yet

- CEDDIA TAYLOR - ClassworkDocument2 pagesCEDDIA TAYLOR - ClassworkCeddia TaylorNo ratings yet

- Tybbi Ibf Sem V Khushbu RuparelDocument22 pagesTybbi Ibf Sem V Khushbu RuparelNandhini0% (1)

- FM 01 04Document14 pagesFM 01 04maaz01888No ratings yet

- The Philippine Financial SystemDocument39 pagesThe Philippine Financial Systemathena100% (1)

- FIN2424 - BFN2034 Chapter 5 Risk and ReturnsDocument42 pagesFIN2424 - BFN2034 Chapter 5 Risk and ReturnsPratap RavichandranNo ratings yet

- DSE 20 Index 2001-2012Document30 pagesDSE 20 Index 2001-2012sazzad_ßĨdNo ratings yet

- Prospectus Msinvf EnluDocument238 pagesProspectus Msinvf EnluDesaulus swtorNo ratings yet

- HBJ Capital's - The Millionaire Portfolio (TMP) Update - Latest SampleDocument19 pagesHBJ Capital's - The Millionaire Portfolio (TMP) Update - Latest SampleHBJ Capital Services Private Limited100% (1)

- Finance Exercise BondDocument2 pagesFinance Exercise Bonddinoo1898No ratings yet

- Spinoff Splitoff Splitup CarveoutDocument2 pagesSpinoff Splitoff Splitup CarveouttransitxyzNo ratings yet