You might also like

- md021 Topic05 ProcessSelectionFacilityLayoutDocument52 pagesmd021 Topic05 ProcessSelectionFacilityLayoutsouvik.icfaiNo ratings yet

- GKDocument1 pageGKsouvik.icfaiNo ratings yet

- India'S Future: 29 January 2007 R B Roy Choudhury Memorial Lecture MumbaiDocument60 pagesIndia'S Future: 29 January 2007 R B Roy Choudhury Memorial Lecture Mumbaisouvik.icfaiNo ratings yet

- Service Level AgreementDocument8 pagesService Level Agreementsouvik.icfaiNo ratings yet

- Classifications Mergers and AcquisitionsDocument8 pagesClassifications Mergers and Acquisitionssouvik.icfaiNo ratings yet

- Definition of A BondDocument16 pagesDefinition of A Bondsouvik.icfaiNo ratings yet

- Bond ValuationDocument13 pagesBond Valuationsouvik.icfaiNo ratings yet

- Indian ITES MarketDocument12 pagesIndian ITES Marketsouvik.icfaiNo ratings yet

- Arbitage Pricing ModelDocument54 pagesArbitage Pricing Modelsouvik.icfai0% (1)

- Business Strategy I & Ii Made Easy Full CourseDocument299 pagesBusiness Strategy I & Ii Made Easy Full Coursesouvik.icfaiNo ratings yet

- Job AnalysisDocument21 pagesJob Analysissouvik.icfai75% (4)

- Course Handout - S.A (Filled)Document7 pagesCourse Handout - S.A (Filled)souvik.icfaiNo ratings yet

- Hire PurchaseDocument14 pagesHire Purchasesouvik.icfai50% (4)

- MCIS 11 & 12 Transfer Pricing - 11Document11 pagesMCIS 11 & 12 Transfer Pricing - 11souvik.icfaiNo ratings yet

- Turn Arround and Numerator and Denominator IN BUSINESS STRATEGY IIDocument21 pagesTurn Arround and Numerator and Denominator IN BUSINESS STRATEGY IIsouvik.icfaiNo ratings yet

- Introduction To Equipment LeasingDocument6 pagesIntroduction To Equipment Leasingsouvik.icfaiNo ratings yet

- Business Strategy I & Ii Made Easy Full CourseDocument299 pagesBusiness Strategy I & Ii Made Easy Full Coursesouvik.icfaiNo ratings yet

- Introduction To Management Control Information SystemDocument13 pagesIntroduction To Management Control Information Systemsouvik.icfai100% (4)

- Lease Evaluation From Lessor AngleDocument32 pagesLease Evaluation From Lessor Anglesouvik.icfaiNo ratings yet

- MCISDocument76 pagesMCISsouvik.icfaiNo ratings yet

- Factoring & ForfaitingDocument19 pagesFactoring & Forfaitingsouvik.icfaiNo ratings yet

- Attributes of A SystemDocument7 pagesAttributes of A Systemsouvik.icfaiNo ratings yet

- Cash & Treasury MGTDocument5 pagesCash & Treasury MGTsouvik.icfaiNo ratings yet

- Lease Evaluation From Lessee AngleDocument22 pagesLease Evaluation From Lessee Anglesouvik.icfaiNo ratings yet

- Legal & Taxation Aspect of LeaseDocument7 pagesLegal & Taxation Aspect of Leasesouvik.icfaiNo ratings yet

- Financial ServicesDocument2 pagesFinancial Servicessouvik.icfaiNo ratings yet

- Legal & Taxation Aspect of LeaseDocument7 pagesLegal & Taxation Aspect of Leasesouvik.icfaiNo ratings yet

- Evolution of Financial ServicesDocument15 pagesEvolution of Financial Servicessouvik.icfai50% (2)

- Investment Banking & Financial Services IDocument407 pagesInvestment Banking & Financial Services Iapi-371582583% (18)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5784)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (72)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Process Sale Use CaseDocument8 pagesProcess Sale Use CaseEminOzNo ratings yet

- SAP in House Cash With MySAP ERPDocument28 pagesSAP in House Cash With MySAP ERPulanaro100% (1)

- PLM TAX 2 2016-2017 List of Cases & Assigned StrudentsDocument19 pagesPLM TAX 2 2016-2017 List of Cases & Assigned StrudentsCharlie Pein100% (1)

- DigiPay v1Document18 pagesDigiPay v1KAVEEN PRASANNAMOORTHYNo ratings yet

- Central New York NY April 20XX: Sample Accounts Sheet-Congregation Bank VersionDocument2 pagesCentral New York NY April 20XX: Sample Accounts Sheet-Congregation Bank VersionAbel ServinNo ratings yet

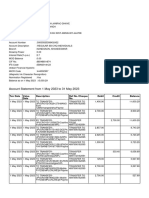

- Account Statement From 1 May 2023 To 31 May 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument10 pagesAccount Statement From 1 May 2023 To 31 May 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit Balanceavinashdeshmukh7027No ratings yet

- Trade Import Export DeclarationDocument7 pagesTrade Import Export DeclarationErik TreasuryvalaNo ratings yet

- Ossc Apply Online For 878 Ayurvedic Assistant Homeopathic Assistant Posts Advt Details PDFDocument14 pagesOssc Apply Online For 878 Ayurvedic Assistant Homeopathic Assistant Posts Advt Details PDFNiroj Kumar SahooNo ratings yet

- Voucher and VRET Format For Payment 12.06.19Document2 pagesVoucher and VRET Format For Payment 12.06.19RahulNo ratings yet

- Essay On The Influence of Microfinance On The Business Development of Merchants in The San José International Market in The City of JuliacaDocument4 pagesEssay On The Influence of Microfinance On The Business Development of Merchants in The San José International Market in The City of JuliacaEvelyn CastilloNo ratings yet

- IDFC First Bank Merges with Capital First to Form Combined EntityDocument6 pagesIDFC First Bank Merges with Capital First to Form Combined EntityMIDHUN ANOOP 17220340% (1)

- ExpressPay DetailsDocument5 pagesExpressPay DetailsSai PastranaNo ratings yet

- Letter of CreditDocument25 pagesLetter of CreditNoone ItdoesntexistNo ratings yet

- Audit of Cash and Cash Equivalents PDFDocument4 pagesAudit of Cash and Cash Equivalents PDFRandyNo ratings yet

- Icici Brochure - PENSION PLAN ULIPDocument10 pagesIcici Brochure - PENSION PLAN ULIPAbhishek PrabhakarNo ratings yet

- Final AcctsDocument7 pagesFinal AcctsSyed ShabirNo ratings yet

- IIFL - Rollover Action - Feb-21 T Expiry DayDocument6 pagesIIFL - Rollover Action - Feb-21 T Expiry DayRomelu MartialNo ratings yet

- Swot AnalysisDocument4 pagesSwot AnalysisMariel TinolNo ratings yet

- Credit Transactions Part 2Document3 pagesCredit Transactions Part 2Mary Ann IsananNo ratings yet

- Audit 2 Week 6 AssignmentDocument11 pagesAudit 2 Week 6 AssignmentDewi RenitasariNo ratings yet

- Negotiation of Export-Import DocumentsDocument16 pagesNegotiation of Export-Import Documentsramneet15866443100% (1)

- Constitution of Mutungo Community AssociationDocument9 pagesConstitution of Mutungo Community AssociationRobert Baguma MwesigwaNo ratings yet

- Cashless Eco SystemDocument43 pagesCashless Eco SystemAnirudh PrabhuNo ratings yet

- Money, The Price Level, and InflationDocument167 pagesMoney, The Price Level, and Inflationoakashler100% (1)

- Account StatementDocument3 pagesAccount StatementJobz ForuNo ratings yet

- Dollar-Consolidated Routing Detail of FundDocument1 pageDollar-Consolidated Routing Detail of Fundcedar1015No ratings yet

- Illustration Cash and Cash EquivalentsDocument2 pagesIllustration Cash and Cash EquivalentsRiyhu DelamercedNo ratings yet

- MCLR Linked Interest RatesDocument8 pagesMCLR Linked Interest RatesAjoydeep DasNo ratings yet

- Ketan Parekh ScamDocument6 pagesKetan Parekh ScamRaunaq BagadeNo ratings yet

- Comp ProjectDocument28 pagesComp Projectavram johnNo ratings yet