You might also like

- An MBA in a Book: Everything You Need to Know to Master Business - In One Book!From EverandAn MBA in a Book: Everything You Need to Know to Master Business - In One Book!No ratings yet

- Accnts Projest - BajajDocument24 pagesAccnts Projest - BajajAprajita SaxenaNo ratings yet

- MANAGERIAL ACCOUNTING Assignment (Ratio Analysis)Document14 pagesMANAGERIAL ACCOUNTING Assignment (Ratio Analysis)Agniv BasuNo ratings yet

- Boosting Capital Efficiency and ROEDocument2 pagesBoosting Capital Efficiency and ROERicardo Jáquez CortésNo ratings yet

- PRESENTATION ON Finincial Statement FinalDocument28 pagesPRESENTATION ON Finincial Statement FinalNollecy Takudzwa Bere100% (2)

- Problem 6-7: Asset Utilization Ratios Measure How Efficient A Business Is at Using Its Assets To Make MoneyDocument11 pagesProblem 6-7: Asset Utilization Ratios Measure How Efficient A Business Is at Using Its Assets To Make MoneyMinza JahangirNo ratings yet

- Business Finance Week 4: Financial Ratios Analysis and Interpretation Background Information For LearnersDocument8 pagesBusiness Finance Week 4: Financial Ratios Analysis and Interpretation Background Information For LearnersCarl Daniel DoromalNo ratings yet

- Ratio Analysis of The CompanyDocument21 pagesRatio Analysis of The CompanyZahid Khan BabaiNo ratings yet

- Leverages FinalDocument26 pagesLeverages FinalVijendra GopaNo ratings yet

- Accounting KFC Holdings Financial Ratio Analysis of Year 2009Document16 pagesAccounting KFC Holdings Financial Ratio Analysis of Year 2009Malathi Sundrasaigaran100% (6)

- BEKARDocument6 pagesBEKARck124881No ratings yet

- Fund Management and Profitability With Reference To APMDCDocument5 pagesFund Management and Profitability With Reference To APMDCthesijNo ratings yet

- LOVISA V PANDORA FINANCIAL ANALYSIS RATIODocument30 pagesLOVISA V PANDORA FINANCIAL ANALYSIS RATIOpipahNo ratings yet

- Profitability Ratio PDFDocument37 pagesProfitability Ratio PDFSiddharth Arora100% (2)

- Tutorial - Week6 AnsDocument8 pagesTutorial - Week6 AnsAnis AshsiffaNo ratings yet

- KFC Company PlanDocument14 pagesKFC Company Planvishalini naiker100% (1)

- Analyzing Financial Ratios to Evaluate a CompanyDocument38 pagesAnalyzing Financial Ratios to Evaluate a Companymuzaire solomon100% (1)

- FMCG Profit AnalysisDocument8 pagesFMCG Profit AnalysisTarun BhatiaNo ratings yet

- Pyq Ch 2-Goodwill (1) (1)Document13 pagesPyq Ch 2-Goodwill (1) (1)hk6206131516No ratings yet

- Corporate-Finance-AM-STDocument5 pagesCorporate-Finance-AM-STAash RedmiNo ratings yet

- Financial Ratio Analysis Final-No in TextDocument32 pagesFinancial Ratio Analysis Final-No in TextMini8912No ratings yet

- Financial Analysis Through RatiosDocument8 pagesFinancial Analysis Through RatiosChandramouli KolavasiNo ratings yet

- Working Capital Management Guide for Improving Company Cash FlowDocument23 pagesWorking Capital Management Guide for Improving Company Cash FlowPankhuri SullereNo ratings yet

- ITC Financial Analysis Using Accounting RatiosDocument32 pagesITC Financial Analysis Using Accounting RatiosSuman GillNo ratings yet

- Ratio Analysis of HR TextilesDocument26 pagesRatio Analysis of HR TextilesOptimistic Eye100% (1)

- Ratio Analysis 19mco014Document11 pagesRatio Analysis 19mco014emmanual cheeranNo ratings yet

- Group 7 FINANCIAL ANALYSIS & ACCOUNTING TechnoDocument27 pagesGroup 7 FINANCIAL ANALYSIS & ACCOUNTING TechnoKezia Tre-intaNo ratings yet

- Af4S31 - Assessment 1 (Av2) Af4S31 - Strategic Financial ManagementDocument13 pagesAf4S31 - Assessment 1 (Av2) Af4S31 - Strategic Financial ManagementugochiNo ratings yet

- MesaDocument12 pagesMesanarang.gp5704No ratings yet

- Financial Analysis of GSK Consumer HealthcareDocument36 pagesFinancial Analysis of GSK Consumer Healthcareadnan424100% (1)

- PPTDocument35 pagesPPTShivam ChauhanNo ratings yet

- 03 Working Capital ManagementDocument55 pages03 Working Capital ManagementRachel R BravoNo ratings yet

- East Coast YachtsDocument7 pagesEast Coast Yachtsdoraemon80100% (1)

- Sample Assignment Analysis HSIB AZRBDocument35 pagesSample Assignment Analysis HSIB AZRBhaznawi100% (1)

- Guinness Anchor Berhad (GAB)Document12 pagesGuinness Anchor Berhad (GAB)mr.balaNo ratings yet

- Financial Ratio Analysis AssignmentDocument10 pagesFinancial Ratio Analysis AssignmentRahim BakhshNo ratings yet

- Apollo Tyres' Financial Performance Analysis from 2004-2009Document65 pagesApollo Tyres' Financial Performance Analysis from 2004-2009Mitisha GaurNo ratings yet

- Aviation Industry: Financial Statement AnalysisDocument62 pagesAviation Industry: Financial Statement AnalysisParul BhusriNo ratings yet

- Corporate Finance:: School of Economics and ManagementDocument13 pagesCorporate Finance:: School of Economics and ManagementNgouem LudovicNo ratings yet

- Fundamentals of Accountancy, Business, and Management 2 SY 2020-2021 QTR1 WK 7 Financial Statement (FS) Analysis MELC/sDocument8 pagesFundamentals of Accountancy, Business, and Management 2 SY 2020-2021 QTR1 WK 7 Financial Statement (FS) Analysis MELC/sAlma Dimaranan-AcuñaNo ratings yet

- Financial Ratio AnalysisDocument2 pagesFinancial Ratio Analysisjjay_santosNo ratings yet

- Xaviers Institute of Business Management StudiesDocument2 pagesXaviers Institute of Business Management StudiesJay KrishnaNo ratings yet

- Chapter 2 Review of Financial Statement Preparation Analysis InterpretationDocument46 pagesChapter 2 Review of Financial Statement Preparation Analysis InterpretationMark DavidNo ratings yet

- Ratio Analysis Reveals LG Display's Financial PerformanceDocument10 pagesRatio Analysis Reveals LG Display's Financial PerformanceSahal Ahmed SyedNo ratings yet

- Financial Ratios Analysis of Coca Cola CompanyDocument42 pagesFinancial Ratios Analysis of Coca Cola Companyhaseeb ahmadNo ratings yet

- Order Number 550 Final (Edited)Document27 pagesOrder Number 550 Final (Edited)Joseph KariukiNo ratings yet

- Assignment On Financial Statement Analysis: Topic: Ratio Analysis and Interpretation ofDocument14 pagesAssignment On Financial Statement Analysis: Topic: Ratio Analysis and Interpretation ofRajashree MuktiarNo ratings yet

- 20090827120835BBFA2203 Topic 1Document22 pages20090827120835BBFA2203 Topic 1adwin_thomasNo ratings yet

- Financial Analysis of ASOSDocument21 pagesFinancial Analysis of ASOSDerayo Biz Amod0% (1)

- Fabm 2 - Module 6Document8 pagesFabm 2 - Module 6Kelvin SaplaNo ratings yet

- Tutorial 1 Financial AccountingDocument4 pagesTutorial 1 Financial AccountingharutotsukassaNo ratings yet

- Financial Ratio Analysis-IIDocument12 pagesFinancial Ratio Analysis-IISivaraj MbaNo ratings yet

- Pantaloon Retail Financial AnalysisDocument18 pagesPantaloon Retail Financial AnalysisSandeep VargheseNo ratings yet

- Assignment On Financial Statement Analysis Berger Paints: School of Management StudiesDocument26 pagesAssignment On Financial Statement Analysis Berger Paints: School of Management StudiesAlkesh Mishra50% (2)

- Guidance For America's Best Businesses: 2009 Annual ReportDocument90 pagesGuidance For America's Best Businesses: 2009 Annual Reportbrlam10011021No ratings yet

- Module 6 - Asset-Based ValuationDocument42 pagesModule 6 - Asset-Based Valuationnatalie clyde matesNo ratings yet

- Ratio Analysis of "Altas Battery": TitleDocument15 pagesRatio Analysis of "Altas Battery": TitleahmadkamranNo ratings yet

- Amazon 2004 Annual ReportDocument104 pagesAmazon 2004 Annual ReportqwertixNo ratings yet

- Thesis Ratio AnalysisDocument8 pagesThesis Ratio Analysisclaudiabrowndurham100% (2)

- TOR Insurance CommitteeDocument5 pagesTOR Insurance CommitteeUsman Aziz KhanNo ratings yet

- Ruiz - Final Internship ReportDocument11 pagesRuiz - Final Internship ReportSuri KenNo ratings yet

- Silver Star Insurance Company Limited Scheme For CLIS LISB &TLISDocument1 pageSilver Star Insurance Company Limited Scheme For CLIS LISB &TLISUsman Aziz KhanNo ratings yet

- UntitledDocument1 pageUntitledUsman Aziz KhanNo ratings yet

- Ruiz - Final Internship ReportDocument11 pagesRuiz - Final Internship ReportSuri KenNo ratings yet

- RegulationDocument7 pagesRegulationnawalNawazNo ratings yet

- Insure Bank Furniture & FixturesDocument1 pageInsure Bank Furniture & FixturesUsman Aziz KhanNo ratings yet

- Insurance Scheme of Crop, Livestock and Tractor For World BankDocument4 pagesInsurance Scheme of Crop, Livestock and Tractor For World BankUsman Aziz KhanNo ratings yet

- Insurance of Vehicles and Calculation of Their AccidentDocument4 pagesInsurance of Vehicles and Calculation of Their AccidentUsman Aziz KhanNo ratings yet

- Revalidation Company PDFDocument2 pagesRevalidation Company PDFHaseebNo ratings yet

- AD Post Material NHMPDocument1 pageAD Post Material NHMPUsman Aziz KhanNo ratings yet

- Isalmic Banking Vs Conventional BankingDocument59 pagesIsalmic Banking Vs Conventional BankingMuhammad Hijab80% (5)

- 2072 15 IpcDocument89 pages2072 15 IpcUsman Aziz KhanNo ratings yet

- System of Financial Control and Budgeting in PakistanDocument47 pagesSystem of Financial Control and Budgeting in Pakistanjamilkiani70% (10)

- Revalidation Company PDFDocument2 pagesRevalidation Company PDFHaseebNo ratings yet

- Vlookup ExamplesDocument5 pagesVlookup ExamplesUsman Aziz KhanNo ratings yet

- WhartonDocument3 pagesWhartonНэСЛиХaН NesNo ratings yet

- Leadership by Daft 5/edDocument14 pagesLeadership by Daft 5/edXahRa MirNo ratings yet

- Building Brands in Emerging MarketsDocument8 pagesBuilding Brands in Emerging MarketsAbhishek MohantyNo ratings yet

- Abbriviations and CapitalsDocument5 pagesAbbriviations and CapitalsUsman Aziz KhanNo ratings yet

- Data Envelopment AnalysisDocument4 pagesData Envelopment AnalysisUsman Aziz KhanNo ratings yet

- Let Your Customers Persuade ThemselvesDocument4 pagesLet Your Customers Persuade ThemselvesUsman Aziz KhanNo ratings yet

- BankDocument1 pageBankUsman Aziz KhanNo ratings yet

- SM Final ReportDocument18 pagesSM Final ReportUsman Aziz KhanNo ratings yet

- Project Financing-Lenders PerspectiveDocument26 pagesProject Financing-Lenders PerspectiveUsman Aziz Khan100% (1)

- Goals, Processes and Rationality: A Parable and A Framework: Marc Le MenestrelDocument23 pagesGoals, Processes and Rationality: A Parable and A Framework: Marc Le MenestrelUsman Aziz KhanNo ratings yet

- Defining and Measuring VariablesDocument24 pagesDefining and Measuring VariablesUsman Aziz KhanNo ratings yet

- IMPORTANCE OF COMMUNICATION IN ENGLISH FOR BUSINESS IN PAKISTAN English ProjectDocument29 pagesIMPORTANCE OF COMMUNICATION IN ENGLISH FOR BUSINESS IN PAKISTAN English ProjectUsman Aziz KhanNo ratings yet

- Business Finance Ratio AbbotDocument35 pagesBusiness Finance Ratio AbbotUsman Aziz KhanNo ratings yet

- Understanding Manufacturing CostsDocument42 pagesUnderstanding Manufacturing CostsOmar Bani-KhalafNo ratings yet

- AuditingDocument5 pagesAuditingJona Mae Milla0% (1)

- Annual Report Analysis Highlights Infosys' Growth DriversDocument9 pagesAnnual Report Analysis Highlights Infosys' Growth DriversAbhishek PaulNo ratings yet

- Financial Statements OverviewDocument36 pagesFinancial Statements OverviewIrvin OngyacoNo ratings yet

- Esmeralda Springs SurpriseDocument8 pagesEsmeralda Springs Surpriseflorinmen1No ratings yet

- Chapter One Accounting For Income TaxesDocument55 pagesChapter One Accounting For Income TaxestalilaNo ratings yet

- Starbucks Case StudyDocument40 pagesStarbucks Case StudyJohnny Page97% (34)

- Income StatementDocument4 pagesIncome StatementBurhan AzharNo ratings yet

- 11 - Financial Analysis and Accounting BasicsDocument21 pages11 - Financial Analysis and Accounting BasicsJay G. Lopez BSEE 1-A100% (2)

- Financial Accounting Canadian 6th Edition Harrison Solutions Manual DownloadDocument79 pagesFinancial Accounting Canadian 6th Edition Harrison Solutions Manual DownloadDarla Escudero100% (23)

- Review QuizDocument200 pagesReview QuizmsjoyevangelistaNo ratings yet

- Transaction Cycle - Audit SeparateDocument4 pagesTransaction Cycle - Audit SeparateNoj Werdna50% (2)

- 14 A Study On Financial Performance of Ponlait, PuducherryDocument69 pages14 A Study On Financial Performance of Ponlait, PuducherrySaravanan Sankari40% (5)

- Analisis Kinerja Keuangan Ditinjau Dari Rasio Solvabilitas, Aktivitas Dan Profitabilitas PT Akasha Wira Internasional TBKDocument9 pagesAnalisis Kinerja Keuangan Ditinjau Dari Rasio Solvabilitas, Aktivitas Dan Profitabilitas PT Akasha Wira Internasional TBKiraNo ratings yet

- ADP Pershing Square 8.17.2017Document168 pagesADP Pershing Square 8.17.2017marketfolly.com100% (2)

- Research Methodology - Worksheet PDFDocument3 pagesResearch Methodology - Worksheet PDFDenisa NedelcuNo ratings yet

- Solution To Chapter 21Document25 pagesSolution To Chapter 21Gab Gab MalgapoNo ratings yet

- La Opala RGDocument19 pagesLa Opala RGrahulmkguptaNo ratings yet

- Literature Review on Financial Ratio AnalysisDocument10 pagesLiterature Review on Financial Ratio AnalysisLaarnie PantinoNo ratings yet

- NATIONAL INTERNAL REVENUE CODEDocument6 pagesNATIONAL INTERNAL REVENUE CODEErica Mae GuzmanNo ratings yet

- New Heritage Doll CompanyDocument12 pagesNew Heritage Doll CompanyRafael Bosch60% (5)

- Financial Statements Trial Balance CheckDocument9 pagesFinancial Statements Trial Balance CheckprashantsdpikiNo ratings yet

- MCS Practical For StudentsDocument10 pagesMCS Practical For StudentsrohitkoliNo ratings yet

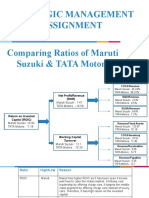

- Strategic Management Assignment Comparing Ratios of Maruti Suzuki & TATA MotorsDocument4 pagesStrategic Management Assignment Comparing Ratios of Maruti Suzuki & TATA MotorsNamanNo ratings yet

- Accounting StandardsDocument24 pagesAccounting Standardslakhan619No ratings yet

- The Process of Express Delivery Service of Indochina Domestics and International Shipping Joint Stock CompanyDocument29 pagesThe Process of Express Delivery Service of Indochina Domestics and International Shipping Joint Stock Companyviet dung NguyenNo ratings yet

- Easy Method Institute: Adjusting EntriesDocument6 pagesEasy Method Institute: Adjusting EntriesKader Jewel100% (1)

- ACCOUNTINGDocument27 pagesACCOUNTINGUzzal HaqueNo ratings yet

- BANK OF BARODA PROPOSAL FOR CREDIT FACILITIESDocument127 pagesBANK OF BARODA PROPOSAL FOR CREDIT FACILITIESgeetaNo ratings yet

- 22sm1e0017 ProjectDocument22 pages22sm1e0017 ProjectEswarnaidu PalliNo ratings yet