You might also like

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- How To Recognize Great Performing Stocks: Your Guide To Spot The Double Bottom Chart PatternDocument16 pagesHow To Recognize Great Performing Stocks: Your Guide To Spot The Double Bottom Chart PatternKoteswara Rao CherukuriNo ratings yet

- Paris Climate Agreement SummaryDocument3 pagesParis Climate Agreement SummaryDorian Grey100% (1)

- Deed of Conditional Sale Sample 13Document4 pagesDeed of Conditional Sale Sample 13Bng100% (1)

- Cir V SLMC DigestDocument3 pagesCir V SLMC DigestYour Public ProfileNo ratings yet

- Dennis Redmond Adorno MicrologiesDocument14 pagesDennis Redmond Adorno MicrologiespatriceframbosaNo ratings yet

- Research On DemonetizationDocument61 pagesResearch On DemonetizationHARSHITA CHAURASIYANo ratings yet

- Economics Environment: National Income AccountingDocument54 pagesEconomics Environment: National Income AccountingRajeev TripathiNo ratings yet

- Ten Principles of UN Global CompactDocument2 pagesTen Principles of UN Global CompactrisefoxNo ratings yet

- The Pioneer 159 EnglishDocument14 pagesThe Pioneer 159 EnglishMuhammad AfzaalNo ratings yet

- Political Economy of Media - A Short IntroductionDocument5 pagesPolitical Economy of Media - A Short Introductionmatthewhandy100% (1)

- PAMI Asia Balanced Fund Product Primer v3 Intro TextDocument1 pagePAMI Asia Balanced Fund Product Primer v3 Intro Textgenie1970No ratings yet

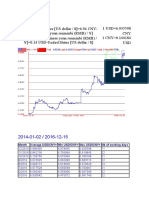

- Month Average USD/CNY Min USD/CNY Max USD/CNY NB of Working DaysDocument3 pagesMonth Average USD/CNY Min USD/CNY Max USD/CNY NB of Working DaysZahid RizvyNo ratings yet

- H 01846769Document418 pagesH 01846769AmirNo ratings yet

- Wedding BlissDocument16 pagesWedding BlissThe Myanmar TimesNo ratings yet

- Data Sheet Machines & MaterialDocument2,407 pagesData Sheet Machines & MaterialPratham BhardwajNo ratings yet

- Fees and ChecklistDocument3 pagesFees and ChecklistAdenuga SantosNo ratings yet

- SLC-Contract Status-20080601-20080630-ALL-REPORTWMDocument37 pagesSLC-Contract Status-20080601-20080630-ALL-REPORTWMbnp2tkidotgodotid100% (1)

- Sustainability in The Built Environment Factors AnDocument7 pagesSustainability in The Built Environment Factors AnGeorges DoungalaNo ratings yet

- Sustainability at Whole FoodsDocument13 pagesSustainability at Whole FoodsHannah Erickson100% (1)

- Family Dollar ReleaseDocument1 pageFamily Dollar ReleaseNewzjunkyNo ratings yet

- Chapter 7 - Valuation and Characteristics of Bonds KEOWNDocument9 pagesChapter 7 - Valuation and Characteristics of Bonds KEOWNKeeZan Lim100% (1)

- No. 3 CambodiaDocument2 pagesNo. 3 CambodiaKhot SovietMrNo ratings yet

- Chapter 01 - PowerPoint - Introduction To Taxation in Canada - 2013Document32 pagesChapter 01 - PowerPoint - Introduction To Taxation in Canada - 2013melsun007No ratings yet

- 12 CONFUCIUS SY 2O23 For Insurance GPA TemplateDocument9 pages12 CONFUCIUS SY 2O23 For Insurance GPA TemplateIris Kayte Huesca EvicnerNo ratings yet

- Lack of Modern Technology in Agriculture System in PakistanDocument4 pagesLack of Modern Technology in Agriculture System in PakistanBahiNo ratings yet

- Nabl 500Document142 pagesNabl 500Vinay SimhaNo ratings yet

- Delegation of Powers As Per DPE GuidelinesDocument23 pagesDelegation of Powers As Per DPE GuidelinesVIJAYAKUMARMPLNo ratings yet

- Mock Meeting Perhentian Kecil IslandDocument3 pagesMock Meeting Perhentian Kecil IslandMezz ShiemaNo ratings yet

- Antwerp Dimamond CaseDocument5 pagesAntwerp Dimamond Casechiranjeeb mitra100% (1)

- Peso Appreciation SeminarDocument3 pagesPeso Appreciation SeminarKayzer SabaNo ratings yet