You might also like

- Final ISO IEC FDIS 17065 2012 E Conformity AssDocument77 pagesFinal ISO IEC FDIS 17065 2012 E Conformity AssahmadNo ratings yet

- UntitledDocument9 pagesUntitledKirk anthony TripoleNo ratings yet

- Deloitte Financial Statement AnalysisDocument4 pagesDeloitte Financial Statement AnalysisAjit AgarwalNo ratings yet

- Financial Accounting Assignment 2Document6 pagesFinancial Accounting Assignment 2kirubelNo ratings yet

- Discounted Cash Flow (DCF) Definition - InvestopediaDocument2 pagesDiscounted Cash Flow (DCF) Definition - Investopedianaviprasadthebond9532No ratings yet

- Itm Quiz 1 Updated Draft 1Document4 pagesItm Quiz 1 Updated Draft 1Nesha ArasuNo ratings yet

- What Is The Difference Between Book Value and Market ValueDocument12 pagesWhat Is The Difference Between Book Value and Market ValueAinie Intwines100% (1)

- Managerial Accounting-Answers For Module and Journal Critique - NuevodocxDocument8 pagesManagerial Accounting-Answers For Module and Journal Critique - NuevodocxKirk anthony TripoleNo ratings yet

- Equity Valuation:: Applications and ProcessesDocument21 pagesEquity Valuation:: Applications and ProcessesMohid SaleemNo ratings yet

- Financial Statement Ratio Analysis PresentationDocument27 pagesFinancial Statement Ratio Analysis Presentationkarimhisham100% (1)

- LIM JournalcritiqueDocument4 pagesLIM JournalcritiqueKirk anthony TripoleNo ratings yet

- Hedge FundsDocument59 pagesHedge FundsjinalvikamseyNo ratings yet

- Ratio AnalysisDocument33 pagesRatio AnalysisJhagantini PalaniveluNo ratings yet

- Eco-Elasticity of DD & SPDocument20 pagesEco-Elasticity of DD & SPSandhyaAravindakshanNo ratings yet

- Module1 Prelim Activity&CaseAnalysisDocument8 pagesModule1 Prelim Activity&CaseAnalysisKirk anthony TripoleNo ratings yet

- Cold Storage Finance RohitDocument11 pagesCold Storage Finance RohitRohitGuleriaNo ratings yet

- Rental Volatility in UK Commercial Market - Assignment (REE) - 2010-FinalDocument11 pagesRental Volatility in UK Commercial Market - Assignment (REE) - 2010-Finaldhruvjjani100% (1)

- Case Presentation Managerial AccountingDocument16 pagesCase Presentation Managerial Accountinggelly studiesNo ratings yet

- PDFDocument5 pagesPDFMa Josielyn Quiming0% (1)

- Financial Statement AnalysisDocument3 pagesFinancial Statement AnalysisUrooj FatimaNo ratings yet

- Twelve Cases of AccountingDocument152 pagesTwelve Cases of AccountingregiscardosoNo ratings yet

- Comparable Company Analysis GuideDocument11 pagesComparable Company Analysis GuideRamesh Chandra DasNo ratings yet

- MNCs PDFDocument13 pagesMNCs PDFOmkar MohiteNo ratings yet

- Interpretation of Ratio Analysis of Novartis PharmaceuticalsDocument28 pagesInterpretation of Ratio Analysis of Novartis PharmaceuticalsumerhameedNo ratings yet

- CA FINAL SFM DERIVATIVES Futures SUMMARYDocument9 pagesCA FINAL SFM DERIVATIVES Futures SUMMARYsujeet mauryaNo ratings yet

- Session 33-34 Meralco Student Spreadsheet - 1556507703Document31 pagesSession 33-34 Meralco Student Spreadsheet - 1556507703Alexander Jason LumantaoNo ratings yet

- Government Accounting FrameworkDocument24 pagesGovernment Accounting FrameworkFrancis TumamaoNo ratings yet

- Assignment 3 - Financial Case StudyDocument1 pageAssignment 3 - Financial Case StudySenura SeneviratneNo ratings yet

- Capital StructureDocument59 pagesCapital StructureRajendra MeenaNo ratings yet

- Incremental AnalysisDocument25 pagesIncremental AnalysisAngel MallariNo ratings yet

- Cost of CapitalDocument18 pagesCost of CapitalyukiNo ratings yet

- The Role of Chief Financial Officers in Managing InnovationDocument10 pagesThe Role of Chief Financial Officers in Managing InnovationNestaNo ratings yet

- Assumptions: DCF ModelDocument3 pagesAssumptions: DCF Modelniraj kumarNo ratings yet

- Brealey. Myers. Allen Chapter 32 SolutionDocument5 pagesBrealey. Myers. Allen Chapter 32 SolutionHassanSheikhNo ratings yet

- Air Care in IndiaDocument8 pagesAir Care in Indiasaurav_eduNo ratings yet

- Case Study BDODocument2 pagesCase Study BDOSaumya GoelNo ratings yet

- Analysis Report On Macquarie GroupDocument55 pagesAnalysis Report On Macquarie GroupBruce BartonNo ratings yet

- Home Capital Group Initiating Coverage (HCG-T)Document68 pagesHome Capital Group Initiating Coverage (HCG-T)Zee MaqsoodNo ratings yet

- Extra WorkDocument3 pagesExtra WorkSarfaraj OviNo ratings yet

- Preliminary Steps in Mergers & Achieving SynergiesDocument16 pagesPreliminary Steps in Mergers & Achieving SynergiesdaterajNo ratings yet

- Framework For Business AnalysisDocument10 pagesFramework For Business AnalysismkhanmajlisNo ratings yet

- GICSDocument17 pagesGICSJuanManuelTorreHuertaNo ratings yet

- 3 Significance of Working CapitalDocument4 pages3 Significance of Working CapitalShruti SehgalNo ratings yet

- Discounted Cash Flow (DCF) ModellingDocument43 pagesDiscounted Cash Flow (DCF) Modellingjasonccheng25No ratings yet

- Investment Decision MethodDocument44 pagesInvestment Decision MethodashwathNo ratings yet

- A Transparency Disclosure Index Measuring Disclosures (Eng)Document31 pagesA Transparency Disclosure Index Measuring Disclosures (Eng)AndriNo ratings yet

- Lambda IndexDocument9 pagesLambda IndexTamanna ShaonNo ratings yet

- A Precisely Practical Measure of The Total Cost of Debt For Determining The Optimal Capital StructureDocument20 pagesA Precisely Practical Measure of The Total Cost of Debt For Determining The Optimal Capital StructureAyudya Puti RamadhantyNo ratings yet

- Ayda EliasDocument104 pagesAyda EliasYayew MaruNo ratings yet

- Final Thesis IntanDocument77 pagesFinal Thesis IntanKarina RusmanNo ratings yet

- Equity ResearchDocument4 pagesEquity ResearchDevangi KothariNo ratings yet

- EPS-bank profit linkDocument10 pagesEPS-bank profit linkchudamaniNo ratings yet

- Discounted Cash Flow Valuation The Inputs: K.ViswanathanDocument47 pagesDiscounted Cash Flow Valuation The Inputs: K.ViswanathanHardik VibhakarNo ratings yet

- Mergers and Acquisitions Strategy AnalysisDocument13 pagesMergers and Acquisitions Strategy AnalysisAnmol GuptaNo ratings yet

- Starboard Darden Sept 2014 294 Slide Deck PPT PDF PresentationDocument294 pagesStarboard Darden Sept 2014 294 Slide Deck PPT PDF PresentationAla BasterNo ratings yet

- Case Study Analysis: 'Michael Hill International: Controlled Expansion and Sustainable Growth'Document14 pagesCase Study Analysis: 'Michael Hill International: Controlled Expansion and Sustainable Growth'steveparker123456No ratings yet

- Assignment - Corporate Finance Capital Budgeting Case Study Project Details Year Project A Project BDocument4 pagesAssignment - Corporate Finance Capital Budgeting Case Study Project Details Year Project A Project BAnshum SethiNo ratings yet

- Chapter 02 Investment AppraisalDocument3 pagesChapter 02 Investment AppraisalMarzuka Akter KhanNo ratings yet

- Critical Financial Review: Understanding Corporate Financial InformationFrom EverandCritical Financial Review: Understanding Corporate Financial InformationNo ratings yet

- Week1b IntroductionDocument34 pagesWeek1b Introductionyow jing peiNo ratings yet

- Week1a.introduction To CourseDocument7 pagesWeek1a.introduction To Courseyow jing peiNo ratings yet

- Mid SemesterExam.Q ADocument4 pagesMid SemesterExam.Q Ayow jing pei100% (4)

- Week3a.journals LedgersDocument10 pagesWeek3a.journals Ledgersyow jing peiNo ratings yet

- Week1c.introduction - Exercises WithoutAnswersDocument8 pagesWeek1c.introduction - Exercises WithoutAnswersyow jing peiNo ratings yet

- List of Companies ASSIGNMENT 1Document2 pagesList of Companies ASSIGNMENT 1yow jing peiNo ratings yet

- LedgerDocument4 pagesLedgeryow jing peiNo ratings yet

- CHAPTER 3 - Accounting EquationDocument16 pagesCHAPTER 3 - Accounting Equationyow jing pei100% (2)

- Ebf1013 Assignment 1 RatiosDocument2 pagesEbf1013 Assignment 1 Ratiosyow jing peiNo ratings yet

- Ebf1013 Assignment 1 RatiosDocument3 pagesEbf1013 Assignment 1 Ratiosyow jing peiNo ratings yet

- Week2a ManualDoubleEntrySystem PPTTPDocument40 pagesWeek2a ManualDoubleEntrySystem PPTTPyow jing peiNo ratings yet

- Week2b.manualDoubleEntrySystem - Exercises WithoutAnswersDocument4 pagesWeek2b.manualDoubleEntrySystem - Exercises WithoutAnswersyow jing peiNo ratings yet

- Week6 SampleExamQuestionDocument16 pagesWeek6 SampleExamQuestionyow jing pei67% (3)

- Week11 BudgetingDocument38 pagesWeek11 Budgetingyow jing peiNo ratings yet

- Cash Flow StatementsDocument19 pagesCash Flow Statementsyow jing peiNo ratings yet

- Warehouse Study Management ProjectDocument46 pagesWarehouse Study Management Projectyow jing peiNo ratings yet

- Week12 AccountingEthicsDocument15 pagesWeek12 AccountingEthicsyow jing peiNo ratings yet

- Week8b.financialStatementsAnalysis Performance - ExercisesDocument12 pagesWeek8b.financialStatementsAnalysis Performance - Exercisesyow jing peiNo ratings yet

- Property, Plant & Equipment (Fixed Assets) : Reeve Warren DuchacDocument33 pagesProperty, Plant & Equipment (Fixed Assets) : Reeve Warren Duchacyow jing peiNo ratings yet

- Week7.Partnerships Corporations OtherOrganisationsDocument40 pagesWeek7.Partnerships Corporations OtherOrganisationsyow jing peiNo ratings yet

- Week6 AComprehensiveIllustrationDocument86 pagesWeek6 AComprehensiveIllustrationyow jing pei89% (28)

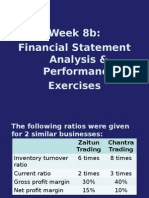

- Week 8: Financial Statement Analysis & PerformanceDocument41 pagesWeek 8: Financial Statement Analysis & Performanceyow jing peiNo ratings yet

- Pleting The Accounting CycleDocument65 pagesPleting The Accounting Cycleyow jing peiNo ratings yet

- Bank Reconciliation StatementDocument17 pagesBank Reconciliation Statementyow jing pei100% (1)

- Week4 ClosingTheAccounts TheAdjustingProcessDocument49 pagesWeek4 ClosingTheAccounts TheAdjustingProcessyow jing peiNo ratings yet

- Supply Chain Management: A Presentation by A.V. VedpuriswarDocument54 pagesSupply Chain Management: A Presentation by A.V. Vedpuriswarramasb4uNo ratings yet

- Week3c ReceivablesDocument14 pagesWeek3c Receivablesyow jing peiNo ratings yet

- Supply Chain Management (3rd Edition)Document17 pagesSupply Chain Management (3rd Edition)Shashank SharmaNo ratings yet

- Supplier Relationship Management in The Context of Supply Chain ManagementDocument12 pagesSupplier Relationship Management in The Context of Supply Chain Managementyow jing peiNo ratings yet

- SP Manual RevisedDocument279 pagesSP Manual Revisedkjkrishnan100% (1)

- 543534534534534Document51 pages543534534534534thanhhai5791No ratings yet

- Diagnostic Level 3 AccountingDocument17 pagesDiagnostic Level 3 AccountingRobert CastilloNo ratings yet

- Account Analysis Statement GuideDocument6 pagesAccount Analysis Statement GuideCr CryptoNo ratings yet

- ProtectionismDocument11 pagesProtectionismM. MassabNo ratings yet

- Footwear Industry in NepalDocument76 pagesFootwear Industry in Nepalsubham jaiswalNo ratings yet

- PCI Professional Training Course DescriptionDocument2 pagesPCI Professional Training Course DescriptionChristian AquinoNo ratings yet

- Co OperativeSocietiesAct12of1997Document49 pagesCo OperativeSocietiesAct12of1997opulitheNo ratings yet

- SAP Plant Maintenance Training PDFDocument5 pagesSAP Plant Maintenance Training PDFRAMRAJA RAMRAJANo ratings yet

- Sales Processes (BBC) ..Document6 pagesSales Processes (BBC) ..Mav RONAKNo ratings yet

- Engineering Marketing and EntrepreneurshipDocument41 pagesEngineering Marketing and Entrepreneurshipimma coverNo ratings yet

- Case Study BookDocument106 pagesCase Study BookshubhaomNo ratings yet

- Cvs Caremark Vs WalgreensDocument17 pagesCvs Caremark Vs Walgreensapi-316819120No ratings yet

- NCERT Solutions For Class 11 Accountancy Financial Accounting Part-1 Chapter 4Document29 pagesNCERT Solutions For Class 11 Accountancy Financial Accounting Part-1 Chapter 4Ioanna Maria MonopoliNo ratings yet

- Mini Project II Instructions Segmentation and RegressionDocument6 pagesMini Project II Instructions Segmentation and RegressionSyed Anns Ali0% (1)

- Problem Solving: A: What Is The Capital Balance of Bea On December 31, 2022?Document6 pagesProblem Solving: A: What Is The Capital Balance of Bea On December 31, 2022?Actg SolmanNo ratings yet

- CHARTERED ACCOUNTANTS EXAMINATIONS T5: TAXATIONDocument21 pagesCHARTERED ACCOUNTANTS EXAMINATIONS T5: TAXATIONMosesNo ratings yet

- Modern business challenges and budgeting rolesDocument10 pagesModern business challenges and budgeting rolesSiare AntoneNo ratings yet

- The Law and Business Administration in Canada 14th Edition SolutionDocument32 pagesThe Law and Business Administration in Canada 14th Edition SolutiontestbanklooNo ratings yet

- Cestui Que Vie TERMINATION THE PERMANENT ESCAPE FROM SLAVERYDocument1 pageCestui Que Vie TERMINATION THE PERMANENT ESCAPE FROM SLAVERYQiydar The KingNo ratings yet

- Kellogg's Case Study AnalysisDocument3 pagesKellogg's Case Study Analysissalil1235667% (3)

- OMB Memo Re: Reducing Regulatory Burden For Federal AgenciesDocument12 pagesOMB Memo Re: Reducing Regulatory Burden For Federal AgenciesFedSmith Inc.100% (1)

- Technical Delivery Manager IT EDM 040813Document2 pagesTechnical Delivery Manager IT EDM 040813Jagadish GaglaniNo ratings yet

- Favourite 3rd Party Transfer: SuccessfulDocument1 pageFavourite 3rd Party Transfer: SuccessfulMizibalya ImanismailNo ratings yet

- Buku2 Ref Ujian WMIDocument3 pagesBuku2 Ref Ujian WMIEndy JupriansyahNo ratings yet

- Supply Chain Management Part 1 Lecture OutlineDocument17 pagesSupply Chain Management Part 1 Lecture OutlineEmmanuel Cocou kounouhoNo ratings yet

- SKF Group10Document21 pagesSKF Group10Shashikumar UdupaNo ratings yet

- Steve Jobs' Three Managerial StylesDocument10 pagesSteve Jobs' Three Managerial StylesMisha12 Misha12No ratings yet

- Aus Tin 20104493Document166 pagesAus Tin 20104493david_llewellyn_smithNo ratings yet

- MB4 - Compliance Requirements 010615Document12 pagesMB4 - Compliance Requirements 010615ninja980117No ratings yet