You might also like

- Credit Rating FinalDocument32 pagesCredit Rating FinaldevrajkinjalNo ratings yet

- Sebi GuidelinesDocument16 pagesSebi GuidelinesJerome P100% (1)

- Statutory AuditDocument20 pagesStatutory Auditkalpesh mhatreNo ratings yet

- Syllabus of Shivaji University MBADocument24 pagesSyllabus of Shivaji University MBAmaheshlakade755No ratings yet

- Capital Adequacy 148Document11 pagesCapital Adequacy 148Bindal Heena100% (1)

- Management Accounting 5th SemDocument24 pagesManagement Accounting 5th SemNeha firdoseNo ratings yet

- Working Capital Two Mark QuestionsDocument4 pagesWorking Capital Two Mark QuestionsHimaja SridharNo ratings yet

- Note On Public IssueDocument9 pagesNote On Public IssueKrish KalraNo ratings yet

- Assignment of AuditingDocument8 pagesAssignment of AuditingMrinal BishtNo ratings yet

- Corporate Finance Current Papers of Final Term PDFDocument35 pagesCorporate Finance Current Papers of Final Term PDFZahid UsmanNo ratings yet

- SEBI Role & FunctionsDocument27 pagesSEBI Role & FunctionsGayatri MhalsekarNo ratings yet

- Responsibility CentersDocument6 pagesResponsibility CentersNitesh Pandita100% (1)

- 203 HRMDocument37 pages203 HRMshubhamatilkar04No ratings yet

- Syllabus - Acc215 - Auditing and Corporate GovernanceDocument2 pagesSyllabus - Acc215 - Auditing and Corporate GovernanceDr. Navneet RajNo ratings yet

- ABC Wealth AdvisorsDocument5 pagesABC Wealth AdvisorsUjwalsagar Sagar33% (3)

- IADR Report On Maruti SuzukiDocument61 pagesIADR Report On Maruti SuzukiHardik AgarwalNo ratings yet

- UNIT-4 Mergers, Diversification and Performance EvaluationDocument13 pagesUNIT-4 Mergers, Diversification and Performance EvaluationRavalika PathipatiNo ratings yet

- Indian Business Environment IntroductionDocument42 pagesIndian Business Environment Introductionsamrulezzz75% (4)

- Icra PPTDocument17 pagesIcra PPTSandeep ReddyNo ratings yet

- Final Accounts of Banking Company - Lecture 01 - 21-08-2020Document8 pagesFinal Accounts of Banking Company - Lecture 01 - 21-08-2020akash gautamNo ratings yet

- Credit Rating Agency in IndiaDocument24 pagesCredit Rating Agency in IndiaAditya50% (2)

- Indian Insight Into TQMDocument13 pagesIndian Insight Into TQMSrinivas Reddy RondlaNo ratings yet

- Sharpe Index Model - Prof. S S PatilDocument36 pagesSharpe Index Model - Prof. S S Patilraj rajyadav100% (1)

- Balance of Payments: International FinanceDocument42 pagesBalance of Payments: International FinanceSoniya Rht0% (1)

- Nature and Significance of Capital Market ClsDocument20 pagesNature and Significance of Capital Market ClsSneha Bajpai100% (2)

- Meaning and Importance of Financial Services 1&2 UNITDocument11 pagesMeaning and Importance of Financial Services 1&2 UNITAvinash KumarNo ratings yet

- Strategic Management PPT by Akshaya KumarDocument23 pagesStrategic Management PPT by Akshaya KumarAkshaya KumarNo ratings yet

- Titan Case StudyDocument19 pagesTitan Case StudyRohitSharmaNo ratings yet

- Question Bank On Financial PlanningDocument2 pagesQuestion Bank On Financial Planningfiiimpact50% (2)

- SAPM I Unit Anna UniversityDocument28 pagesSAPM I Unit Anna UniversitystandalonembaNo ratings yet

- Unit 12 Sick Industrial UnitDocument17 pagesUnit 12 Sick Industrial UnitGinu George VargheseNo ratings yet

- IFM Notes Full Rudramurthy SirDocument96 pagesIFM Notes Full Rudramurthy Sirsagar_us100% (1)

- EX - NO:1 Company Creation Query:: Computerized Accounting PracticalDocument15 pagesEX - NO:1 Company Creation Query:: Computerized Accounting PracticalJinson K JNo ratings yet

- Insurance IntermediariesDocument9 pagesInsurance IntermediariesarmailgmNo ratings yet

- Unit 4 by Ravi Recent TrendsDocument43 pagesUnit 4 by Ravi Recent TrendsChintan Kalpesh Modi100% (2)

- Foreign Institutional InvestorsDocument15 pagesForeign Institutional InvestorsJagritiChhabraNo ratings yet

- HindustanDocument73 pagesHindustanGuman Singh0% (1)

- Nature and Objectives of Management AccountingDocument13 pagesNature and Objectives of Management AccountingpfungwaNo ratings yet

- Small Industries Development Organisation:, Mahesh.PDocument12 pagesSmall Industries Development Organisation:, Mahesh.Pharidinesh100% (1)

- International BusinessDocument2 pagesInternational BusinessPrateek Sinha0% (2)

- Business Ethics: An Indian PerspectiveDocument21 pagesBusiness Ethics: An Indian Perspectivepuja kanoiNo ratings yet

- Chapter 5 Digital Marketing Strategy Definition - Fundamentals of Digital Marketing, 2 - e - Dev TutorialsDocument54 pagesChapter 5 Digital Marketing Strategy Definition - Fundamentals of Digital Marketing, 2 - e - Dev TutorialsViruchika PahujaNo ratings yet

- NSTEDBDocument9 pagesNSTEDBSweta SinhaNo ratings yet

- Canara BankDocument15 pagesCanara BankeswariNo ratings yet

- MCQsDocument9 pagesMCQsNareshNo ratings yet

- MBA Logistics ManagementDocument13 pagesMBA Logistics ManagementNaresh GuduruNo ratings yet

- International LiquidityDocument19 pagesInternational LiquidityAnu Narayanankutty100% (2)

- Credit RatingDocument15 pagesCredit RatingKrishna Chandran PallippuramNo ratings yet

- SebiDocument13 pagesSebiNishat ShaikhNo ratings yet

- Unit 5: Emerging Trends in HRMDocument27 pagesUnit 5: Emerging Trends in HRManuradhakampli100% (1)

- Osmania University Guideliness or Research For BbaDocument17 pagesOsmania University Guideliness or Research For BbaattaullahNo ratings yet

- Assignment Rubric Financial Management PFN1223Document2 pagesAssignment Rubric Financial Management PFN1223NURUL FATIN NABILA BINTI MOHD FADZIL (BG)No ratings yet

- Empowerment of Women Through EntrepreneurshipDocument39 pagesEmpowerment of Women Through EntrepreneurshipClassic PrintersNo ratings yet

- Bba VDocument2 pagesBba VkunalbrabbitNo ratings yet

- Project Appraisal Under RiskDocument2 pagesProject Appraisal Under RiskSigei LeonardNo ratings yet

- Chap3 SMBP KazmiDocument15 pagesChap3 SMBP KazmiAnkit Verma100% (1)

- EADR SyllabusDocument2 pagesEADR SyllabussanzitNo ratings yet

- Product Mix StrategiesDocument17 pagesProduct Mix StrategiesDr Rushen SinghNo ratings yet

- Indian Banking System Syllabus PDFDocument2 pagesIndian Banking System Syllabus PDFMahek BaigNo ratings yet

- Economic Impact of Margaret ThatcherDocument4 pagesEconomic Impact of Margaret Thatchertaufeek_irawan7201No ratings yet

- Difference Between EVA and ROIDocument6 pagesDifference Between EVA and ROINik PatelNo ratings yet

- Syllabus in Acctg. 13 Management Consultancy BSADocument10 pagesSyllabus in Acctg. 13 Management Consultancy BSAAnonymous Vng49z7hNo ratings yet

- The Role of Managerial Finance: All Rights ReservedDocument45 pagesThe Role of Managerial Finance: All Rights ReservedmoonaafreenNo ratings yet

- A Project Report On Ratio Analysis in ParulDocument37 pagesA Project Report On Ratio Analysis in Parulmunna00016No ratings yet

- Deductions Under Chapter VIDocument4 pagesDeductions Under Chapter VIMonisha ParekhNo ratings yet

- Ekonomi Moneter 2: - Literatur: Ekonomi Uang, Perbankan, Dan Pasar Keuangan Frederic S. Mishkin Edisi 9Document27 pagesEkonomi Moneter 2: - Literatur: Ekonomi Uang, Perbankan, Dan Pasar Keuangan Frederic S. Mishkin Edisi 9Afrian Yuzhar FadhilaNo ratings yet

- Runescape Insider To MillionsDocument51 pagesRunescape Insider To MillionsPaul CoteNo ratings yet

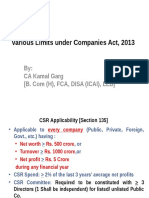

- Various Limits Under Companies Act, 2013 (CA Final)Document61 pagesVarious Limits Under Companies Act, 2013 (CA Final)Asim JavedNo ratings yet

- T1 BookDocument22 pagesT1 BookDavin PathNo ratings yet

- Time Value of MoneyDocument9 pagesTime Value of Moneyelarabel abellareNo ratings yet

- BPI Vs PosadasDocument2 pagesBPI Vs PosadasCarlota Nicolas VillaromanNo ratings yet

- Scope City IncDocument11 pagesScope City IncMd.Akther UddinNo ratings yet

- Export GuidanceDocument45 pagesExport GuidanceRomi PatelNo ratings yet

- Comparative Analysis of Mutual Fund of HDFC ICICIDocument33 pagesComparative Analysis of Mutual Fund of HDFC ICICIAniket Ramteke100% (1)

- Understanding Money and Financial InstitutionsDocument36 pagesUnderstanding Money and Financial InstitutionsHasan Tahir SubhaniNo ratings yet

- Resumen Chapter 19 - Intermediate AccountingDocument7 pagesResumen Chapter 19 - Intermediate AccountingDianaa Lagunes BlancoNo ratings yet

- Handbookoflondon 00 PricuoftDocument490 pagesHandbookoflondon 00 Pricuoftchickenlickenhennypenny0% (1)

- Mcs 035Document256 pagesMcs 035Urvashi Roy100% (1)

- Sinco Vs Longa & Tevez 1928 (Guardianship) Facts:: Specpro Digest - MidtermDocument2 pagesSinco Vs Longa & Tevez 1928 (Guardianship) Facts:: Specpro Digest - MidtermAngelic ArcherNo ratings yet

- IE CH 05-AnsDocument4 pagesIE CH 05-AnsHuo ZenNo ratings yet

- Central Bank of Sri Lanka: Selected Weekly Economic IndicatorsDocument12 pagesCentral Bank of Sri Lanka: Selected Weekly Economic IndicatorsRandora LkNo ratings yet

- Negosyo Center LaunchedDocument3 pagesNegosyo Center LaunchedVanessaClaireTeroPleñaNo ratings yet

- EphremDocument3 pagesEphremsamuel debebeNo ratings yet

- ICAP Cost Past PaperDocument9 pagesICAP Cost Past Paperfarooqshah4uNo ratings yet

- MPS LTD Valuation ReportDocument1 pageMPS LTD Valuation ReportSiddharth ShahNo ratings yet

- Project On Resort Cum HotelDocument13 pagesProject On Resort Cum Hotelsunilsony12376% (21)

- Wave Fearless Accounting GuideDocument114 pagesWave Fearless Accounting GuideRenata Chiquelho100% (1)

- Financial Policy and Procedure Manual TemplateDocument31 pagesFinancial Policy and Procedure Manual TemplatevanausabNo ratings yet