You might also like

- Managing Britannia: Culture and Management in Modern BritainFrom EverandManaging Britannia: Culture and Management in Modern BritainRating: 4 out of 5 stars4/5 (1)

- Chapter 6Document33 pagesChapter 6Muhammad SufyanNo ratings yet

- Value Chain Management Capability A Complete Guide - 2020 EditionFrom EverandValue Chain Management Capability A Complete Guide - 2020 EditionNo ratings yet

- Chapter 3Document36 pagesChapter 3Nouman MujahidNo ratings yet

- Cavusgil Fwib1 PPT 11Document33 pagesCavusgil Fwib1 PPT 11Dramba Silvia FlorinaNo ratings yet

- Banana WarDocument19 pagesBanana WarNiket SinhaNo ratings yet

- Chapter 5 UpdatedDocument68 pagesChapter 5 UpdatedLaniana GiniginiNo ratings yet

- Chapter 11Document24 pagesChapter 11Samina KhanNo ratings yet

- Management of Transaction ExposureDocument10 pagesManagement of Transaction ExposuredediismeNo ratings yet

- Business Ethics, Stakeholder ManagementDocument17 pagesBusiness Ethics, Stakeholder ManagementRempeyekNo ratings yet

- Global Marketing Management - Planning and OrganizationDocument14 pagesGlobal Marketing Management - Planning and OrganizationShihab MuhammedNo ratings yet

- Crafting Brand PositioningDocument15 pagesCrafting Brand PositioningalisamiyaNo ratings yet

- Kotler MM 14e 06 IpptDocument25 pagesKotler MM 14e 06 IpptriskaprkasitaNo ratings yet

- Topic 1 Introduction To Corporate FinanceDocument26 pagesTopic 1 Introduction To Corporate FinancelelouchNo ratings yet

- International Business-Ec505Document5 pagesInternational Business-Ec505Siddharth Singh TomarNo ratings yet

- Fundamentals of Investments. Chapter1: A Brief History of Risk and ReturnDocument34 pagesFundamentals of Investments. Chapter1: A Brief History of Risk and ReturnNorina100% (1)

- Balance Scorecard and BenchmarkingDocument12 pagesBalance Scorecard and BenchmarkingGaurav Sharma100% (1)

- Icfai ExamDocument3 pagesIcfai Examtripathi.shantanu3778No ratings yet

- Chapter 2 International Trade and InvestmentDocument8 pagesChapter 2 International Trade and InvestmentMhyr Pielago Camba100% (1)

- IM Lecture 7 - CHP 7 - Global Alliances and Strategy ImplementationDocument25 pagesIM Lecture 7 - CHP 7 - Global Alliances and Strategy ImplementationRayanna Golding100% (1)

- LGDocument3 pagesLGmister_t101No ratings yet

- Toyota Case StydyDocument6 pagesToyota Case Stydytom agazhieNo ratings yet

- Regional and Global StrategyDocument32 pagesRegional and Global Strategycooljani01No ratings yet

- Chapter 3 - InsuranceDocument30 pagesChapter 3 - InsuranceAhmed NaserNo ratings yet

- Business PlanDocument16 pagesBusiness PlanFrOzen HeArtNo ratings yet

- IFM - Chapter 1Document20 pagesIFM - Chapter 1Annapurna VasireddyNo ratings yet

- PWCDocument2 pagesPWCKomang Ratih TunjungsariNo ratings yet

- International Financial MarketsDocument42 pagesInternational Financial MarketsVamsi Kumar0% (1)

- Barringer E4 PPT 10GEDocument40 pagesBarringer E4 PPT 10GEPutera FirdausNo ratings yet

- Shoaib Akhtar Assignment-1 Marketting Research On Mochari Shoes BrandDocument5 pagesShoaib Akhtar Assignment-1 Marketting Research On Mochari Shoes BrandSHOAIB AKHTARNo ratings yet

- Case 6 GoogleDocument13 pagesCase 6 Googleshoeb1276No ratings yet

- Chap-17-Lending Policies and ProceduresDocument30 pagesChap-17-Lending Policies and ProceduresNazmul H. PalashNo ratings yet

- Chapter 1Document29 pagesChapter 1Amr ElkholyNo ratings yet

- Volkswagen Case Study International FinanceDocument15 pagesVolkswagen Case Study International FinanceLena PhanNo ratings yet

- International Business by Daniels and Radebaugh SlidesDocument16 pagesInternational Business by Daniels and Radebaugh SlidesSaad AliNo ratings yet

- Introduction To Business - Chapter 3 - Entrepreneurship, Franchising and Small BusinessDocument26 pagesIntroduction To Business - Chapter 3 - Entrepreneurship, Franchising and Small BusinessHamidul Islam100% (1)

- Global Finance Na PamatayDocument193 pagesGlobal Finance Na PamatayMary Joy Villaflor HepanaNo ratings yet

- Financial Accounting: A Managerial Perspective: Sixth EditionDocument15 pagesFinancial Accounting: A Managerial Perspective: Sixth EditionKARISHMA SANGHAINo ratings yet

- International Business: by Charles W.L. HillDocument47 pagesInternational Business: by Charles W.L. HillKlaseekNo ratings yet

- pp04Document83 pagespp04sadiaNo ratings yet

- FOF Seminar Activities Topic 4 SolutionsDocument7 pagesFOF Seminar Activities Topic 4 Solutionsmuller1234No ratings yet

- Chapter 8 Corporate FinanceDocument34 pagesChapter 8 Corporate FinancediaNo ratings yet

- The E Marketing MixDocument29 pagesThe E Marketing MixSatish KumarNo ratings yet

- ModelDocument22 pagesModelArchana DeepakNo ratings yet

- Assigment-1 NewDocument115 pagesAssigment-1 NewNuwani ManasingheNo ratings yet

- Lecture Notes Consumer Behavior TextbookDocument185 pagesLecture Notes Consumer Behavior TextbookSao Nguyễn ToànNo ratings yet

- Export Import CH 15Document6 pagesExport Import CH 15zahirahmed89No ratings yet

- MB0036 - Strategic Management and Business PolicyDocument297 pagesMB0036 - Strategic Management and Business Policysuahik100% (2)

- International Martketing Practice Questions: Keegan 8e Ch08Document7 pagesInternational Martketing Practice Questions: Keegan 8e Ch08PandaNo ratings yet

- Global Business NOTESDocument20 pagesGlobal Business NOTESShane DalyNo ratings yet

- 4 Ps For TouchéDocument13 pages4 Ps For TouchéShivangi TanejaNo ratings yet

- Work Life Balance: BBA-1 SemesterDocument8 pagesWork Life Balance: BBA-1 Semesterkapil gargNo ratings yet

- Literature ReviewDocument19 pagesLiterature ReviewRonak BhandariNo ratings yet

- Critical Environmental Concerns in Wine Production An Integrative ReviewDocument11 pagesCritical Environmental Concerns in Wine Production An Integrative Reviewasaaca123No ratings yet

- Green Marketing in India Challenges andDocument13 pagesGreen Marketing in India Challenges andAmirul FathiNo ratings yet

- The Nature of Project Selection ModelsDocument13 pagesThe Nature of Project Selection ModelsGopalsamy SelvaduraiNo ratings yet

- Chapter 4 - International Marketing Research and Opportunity AnalysisDocument17 pagesChapter 4 - International Marketing Research and Opportunity Analysiskingsley okohNo ratings yet

- Global Finance With E-BankingDocument13 pagesGlobal Finance With E-BankingTessa AriateNo ratings yet

- Chapter 13Document52 pagesChapter 13Nouman Mujahid100% (1)

- Chapter 5Document54 pagesChapter 5Nouman MujahidNo ratings yet

- Notes On Inventory ValuationDocument7 pagesNotes On Inventory ValuationNouman Mujahid100% (2)

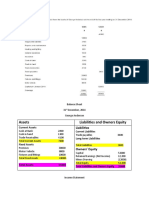

- Assets Liabilities and Owners EquityDocument9 pagesAssets Liabilities and Owners EquityNouman MujahidNo ratings yet

- Quiz of DividendDocument1 pageQuiz of DividendNouman Mujahid0% (1)

- Quiz On DepreciationDocument1 pageQuiz On DepreciationNouman MujahidNo ratings yet

- Merger: Acquiring CompanyDocument3 pagesMerger: Acquiring CompanyNouman MujahidNo ratings yet

- Assignment On DepreciationDocument4 pagesAssignment On DepreciationNouman MujahidNo ratings yet

- Depreciation and Carrying AmountDocument12 pagesDepreciation and Carrying AmountNouman MujahidNo ratings yet

- When Market Risk Plus Own Company Debt Risk Adds It Becomes Beta LeveredDocument5 pagesWhen Market Risk Plus Own Company Debt Risk Adds It Becomes Beta LeveredNouman MujahidNo ratings yet

- Notes On Working Capital ManagementDocument11 pagesNotes On Working Capital ManagementNouman MujahidNo ratings yet

- Ebit EBIT Q P-FC-VC Q: Find EBIT Price Quantity Sales - Fixed Cost - VC Per Unit Quantity TVCDocument6 pagesEbit EBIT Q P-FC-VC Q: Find EBIT Price Quantity Sales - Fixed Cost - VC Per Unit Quantity TVCNouman MujahidNo ratings yet

- Q13Document1 pageQ13Nouman MujahidNo ratings yet

- Ebit EBIT Q P-FC-VC Q: Find EBIT Price Quantity Sales - Fixed Cost - VC Per Unit Quantity TVCDocument6 pagesEbit EBIT Q P-FC-VC Q: Find EBIT Price Quantity Sales - Fixed Cost - VC Per Unit Quantity TVCNouman MujahidNo ratings yet

- Dividends: Factors Affecting Dividend PolicyDocument7 pagesDividends: Factors Affecting Dividend PolicyNouman MujahidNo ratings yet

- Breakeven Analysis: EBIT $0Document5 pagesBreakeven Analysis: EBIT $0Nouman MujahidNo ratings yet

- Beta Levered and UnleveredDocument3 pagesBeta Levered and UnleveredNouman MujahidNo ratings yet

- Ebit EBIT Q P-FC-VC Q: Find EBIT Price Quantity Sales - Fixed Cost - VC Per Unit Quantity TVCDocument6 pagesEbit EBIT Q P-FC-VC Q: Find EBIT Price Quantity Sales - Fixed Cost - VC Per Unit Quantity TVCNouman MujahidNo ratings yet

- Accounts Payable ManagementDocument3 pagesAccounts Payable ManagementNouman MujahidNo ratings yet

- Bahvioral FinanceDocument14 pagesBahvioral FinanceNouman MujahidNo ratings yet

- CH 17Document39 pagesCH 17Nouman MujahidNo ratings yet

- Averageinvestment Under Proposed /actual Plan (Total Variable Cost) / (Turnover of Accounts Receivable)Document1 pageAverageinvestment Under Proposed /actual Plan (Total Variable Cost) / (Turnover of Accounts Receivable)Nouman MujahidNo ratings yet

- What Is Behavioral FinanceDocument4 pagesWhat Is Behavioral FinanceNouman MujahidNo ratings yet

- How To Calculate The Beta of A Private CompanyDocument3 pagesHow To Calculate The Beta of A Private CompanyDuaa TahirNo ratings yet

- When Market Risk Plus Own Company Debt Risk Adds It Becomes Beta LeveredDocument5 pagesWhen Market Risk Plus Own Company Debt Risk Adds It Becomes Beta LeveredNouman MujahidNo ratings yet

- Initial Cash FlowDocument3 pagesInitial Cash FlowNouman Mujahid50% (2)

- Madina Medical StoreDocument29 pagesMadina Medical StoreNouman MujahidNo ratings yet

- How To Write Effective Introduction of An ArticleDocument14 pagesHow To Write Effective Introduction of An ArticleNouman MujahidNo ratings yet

- Beta Levered and UnleveredDocument3 pagesBeta Levered and UnleveredNouman MujahidNo ratings yet

- Chapter# 7Document43 pagesChapter# 7Nouman MujahidNo ratings yet

- Finance Interview Questions: Carey CompassDocument2 pagesFinance Interview Questions: Carey CompassNouman MujahidNo ratings yet

- W W W W W: Writing StrategiesDocument59 pagesW W W W W: Writing StrategiesHenao LuciaNo ratings yet

- Trip ID: 230329124846: New Delhi To Gorakhpur 11:15 GOPDocument2 pagesTrip ID: 230329124846: New Delhi To Gorakhpur 11:15 GOPRishu KumarNo ratings yet

- Petron Corporation and Peter Milagro v. National Labor Relations Commission and Chito MantosDocument2 pagesPetron Corporation and Peter Milagro v. National Labor Relations Commission and Chito MantosRafaelNo ratings yet

- The Nature of LoveDocument97 pagesThe Nature of LoveMiguel Garcia Herrera100% (1)

- Week 13 - Local Government (Ra 7160) and DecentralizationDocument4 pagesWeek 13 - Local Government (Ra 7160) and DecentralizationElaina JoyNo ratings yet

- Robert Brissette A Local Massage Therapist Decided To Sell His PDFDocument1 pageRobert Brissette A Local Massage Therapist Decided To Sell His PDFTaimour HassanNo ratings yet

- Document - 2019-12-20T133208.945 PDFDocument2 pagesDocument - 2019-12-20T133208.945 PDFMina JoonNo ratings yet

- Case Study On Tata NanoDocument12 pagesCase Study On Tata NanoChandel Manuj100% (1)

- DOLE - DO 174 RenewalDocument5 pagesDOLE - DO 174 Renewalamadieu50% (2)

- Core ScientificDocument8 pagesCore ScientificRob PortNo ratings yet

- Factura ComercialDocument4 pagesFactura ComercialErick Limpias Rios BridouxNo ratings yet

- Presenters GuidelinesDocument9 pagesPresenters GuidelinesAl Dustur JurnalNo ratings yet

- Why Baptists Are Not ProtestantsDocument4 pagesWhy Baptists Are Not ProtestantsRyan Bladimer Africa RubioNo ratings yet

- Review - Phippine Arch Post WarDocument34 pagesReview - Phippine Arch Post WariloilocityNo ratings yet

- Overview of Data Tiering Options in SAP HANA and Sap Hana CloudDocument38 pagesOverview of Data Tiering Options in SAP HANA and Sap Hana Cloudarban bNo ratings yet

- 10 Overseas Bank Vs CA & Tapia PDFDocument10 pages10 Overseas Bank Vs CA & Tapia PDFNicoleAngeliqueNo ratings yet

- Cda Change Name Locality enDocument2 pagesCda Change Name Locality enBiñan Metropolitan ChorusNo ratings yet

- Turban Kurta Topee - in Light of Sunnah and Practice of The Sahaba and TabieenDocument18 pagesTurban Kurta Topee - in Light of Sunnah and Practice of The Sahaba and Tabieenadilayub1No ratings yet

- The Analysis of Foreign PolicyDocument24 pagesThe Analysis of Foreign PolicyMikael Dominik AbadNo ratings yet

- List of Books WrittenEdited by DR - Asghar Ali EngineerDocument2 pagesList of Books WrittenEdited by DR - Asghar Ali EngineerFarman AliNo ratings yet

- App3 Flexographic Ink Formulations and StructuresDocument58 pagesApp3 Flexographic Ink Formulations and StructuresMilos Papic100% (2)

- Money and Banking Q&ADocument9 pagesMoney and Banking Q&AKrrish WaliaNo ratings yet

- Analysis of NPADocument31 pagesAnalysis of NPApremlal1989No ratings yet

- Hydrolics-Ch 4Document21 pagesHydrolics-Ch 4solxNo ratings yet

- G.R. No. 202039. August 14, 2019. ANGELITA SIMUNDAC-KEPPEL, Petitioner, vs. GEORG KEPPEL, Respondent. FactsDocument2 pagesG.R. No. 202039. August 14, 2019. ANGELITA SIMUNDAC-KEPPEL, Petitioner, vs. GEORG KEPPEL, Respondent. FactsAngela Marie Almalbis80% (5)

- Trump Presidency 33 - May 5th, 2018 To May 14th, 2018Document513 pagesTrump Presidency 33 - May 5th, 2018 To May 14th, 2018FW040100% (1)

- Interchange FeeDocument3 pagesInterchange FeeAnkita SrivastavaNo ratings yet

- The Missing Children in Public Discourse On Child Sexual AbuseDocument8 pagesThe Missing Children in Public Discourse On Child Sexual AbuseJane Gilgun100% (1)

- Evolution of Hotel Management Agreements and Rise of Alternative AgreementsDocument14 pagesEvolution of Hotel Management Agreements and Rise of Alternative AgreementsSharif Fayiz AbushaikhaNo ratings yet

- Company: ManufacturingDocument8 pagesCompany: Manufacturingzain khalidNo ratings yet

- Dansart Security Force v. BagoyDocument4 pagesDansart Security Force v. BagoyAyo LapidNo ratings yet