You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Class Action Lawsuit Against Johnson & JohnsonDocument49 pagesClass Action Lawsuit Against Johnson & JohnsonAnonymous GF8PPILW575% (4)

- Computer-Aided Administration of Registration Department (CARD), Hyderabad, Andhra PradeshDocument2 pagesComputer-Aided Administration of Registration Department (CARD), Hyderabad, Andhra PradeshtechiealyyNo ratings yet

- KEPITAL-POM - KEPITAL F20-03 LOF - en - RoHSDocument8 pagesKEPITAL-POM - KEPITAL F20-03 LOF - en - RoHSEnzo AscañoNo ratings yet

- C. Rules of Adminissibility - Documentary Evidence - Best Evidence Rule - Loon Vs Power Master Inc, 712 SCRADocument1 pageC. Rules of Adminissibility - Documentary Evidence - Best Evidence Rule - Loon Vs Power Master Inc, 712 SCRAJocelyn Yemyem Mantilla VelosoNo ratings yet

- Competition Law: Anirban MazumderDocument21 pagesCompetition Law: Anirban MazumdertoabhishekpalNo ratings yet

- Company LawDocument76 pagesCompany LawtoabhishekpalNo ratings yet

- Constitutional Law: Anirban Mazumder National University of Juridical Sciences CalcuttaDocument9 pagesConstitutional Law: Anirban Mazumder National University of Juridical Sciences CalcuttatoabhishekpalNo ratings yet

- Portfolio TheoryDocument9 pagesPortfolio TheorytoabhishekpalNo ratings yet

- Capabilities-Driven Strategy: IMI Kolkata 22nd February 2012 Rudra ChatterjeeDocument25 pagesCapabilities-Driven Strategy: IMI Kolkata 22nd February 2012 Rudra ChatterjeetoabhishekpalNo ratings yet

- Session 1 - What Is StrategyDocument15 pagesSession 1 - What Is StrategytoabhishekpalNo ratings yet

- Project Planning and Capital BudgetingDocument16 pagesProject Planning and Capital BudgetingtoabhishekpalNo ratings yet

- Asian PaintsDocument15 pagesAsian PaintstoabhishekpalNo ratings yet

- Dividend DecisionsDocument3 pagesDividend DecisionstoabhishekpalNo ratings yet

- Print Order # 100000299Document2 pagesPrint Order # 100000299toabhishekpalNo ratings yet

- Learn SAP QM in 4 DaysDocument17 pagesLearn SAP QM in 4 DaystoabhishekpalNo ratings yet

- SAP SRM TCodes PDFDocument6 pagesSAP SRM TCodes PDFtoabhishekpalNo ratings yet

- Sap SRM TcodesDocument6 pagesSap SRM TcodestoabhishekpalNo ratings yet

- Session 12: Implementation and Maintenance StrategiesDocument18 pagesSession 12: Implementation and Maintenance StrategiestoabhishekpalNo ratings yet

- Session 6Document5 pagesSession 6toabhishekpalNo ratings yet

- Object Oriented Modeling: Sessions 8 and 9Document9 pagesObject Oriented Modeling: Sessions 8 and 9toabhishekpalNo ratings yet

- Levis Project ReportDocument12 pagesLevis Project Reportjibran-khan-7355100% (2)

- Presentation: Pradhan Mantri Gram Sadak YojanaDocument25 pagesPresentation: Pradhan Mantri Gram Sadak Yojanaamitmishra50100% (1)

- Tabang vs. National Labor Relations CommissionDocument6 pagesTabang vs. National Labor Relations CommissionRMC PropertyLawNo ratings yet

- OSHAD-SF - TG - Managament of Contractors v3.0 EnglishDocument18 pagesOSHAD-SF - TG - Managament of Contractors v3.0 EnglishGirish GopalakrishnanNo ratings yet

- Mathematical Solutions - Part ADocument363 pagesMathematical Solutions - Part ABikash ThapaNo ratings yet

- Suggested Solution Far 660 Final Exam December 2019Document6 pagesSuggested Solution Far 660 Final Exam December 2019Nur ShahiraNo ratings yet

- DBQ 1 - MissionsDocument3 pagesDBQ 1 - Missionsapi-284740735No ratings yet

- Credit Operations and Risk Management in Commercial BanksDocument4 pagesCredit Operations and Risk Management in Commercial Bankssn nNo ratings yet

- India Mineral Report PDFDocument38 pagesIndia Mineral Report PDFRohan KumarNo ratings yet

- Pra05 TMP-301966624 PR002Document3 pagesPra05 TMP-301966624 PR002Pilusa AguirreNo ratings yet

- Eacsb PDFDocument297 pagesEacsb PDFTai ThomasNo ratings yet

- Branch - QB Jan 22Document40 pagesBranch - QB Jan 22Nikitaa SanghviNo ratings yet

- Powerpoint - The Use of Animals in FightingDocument18 pagesPowerpoint - The Use of Animals in Fightingcyc5326No ratings yet

- Commercial Banking Operations:: Types of Commercial BanksDocument6 pagesCommercial Banking Operations:: Types of Commercial BanksKhyell PayasNo ratings yet

- 96boards Iot Edition: Low Cost Hardware Platform SpecificationDocument15 pages96boards Iot Edition: Low Cost Hardware Platform SpecificationSapta AjieNo ratings yet

- Ratio AnalysisDocument36 pagesRatio AnalysisHARVENDRA9022 SINGHNo ratings yet

- The PassiveDocument12 pagesThe PassiveCliver Rusvel Cari SucasacaNo ratings yet

- Beebe ME Chain HoistDocument9 pagesBeebe ME Chain HoistDan VekasiNo ratings yet

- CIR v. CTA and Smith Kline, G.R. No. L-54108, 1984Document4 pagesCIR v. CTA and Smith Kline, G.R. No. L-54108, 1984JMae MagatNo ratings yet

- DocumentsRB - PSS - SMD - EMEA2022 V 01.0 06.04.22 08.00 - REGIDocument74 pagesDocumentsRB - PSS - SMD - EMEA2022 V 01.0 06.04.22 08.00 - REGIRegina TschernitzNo ratings yet

- Solvency PPTDocument1 pageSolvency PPTRITU SINHA MBA 2019-21 (Kolkata)No ratings yet

- Farm Animal Fun PackDocument12 pagesFarm Animal Fun PackDedeh KhalilahNo ratings yet

- Dictatorship in Pakistan PDFDocument18 pagesDictatorship in Pakistan PDFAsad khanNo ratings yet

- Od126200744691887000 4Document1 pageOd126200744691887000 4Swyam SaxenaNo ratings yet

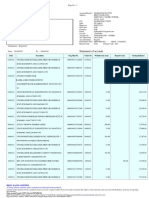

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument3 pagesStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceHiten AhirNo ratings yet

- 201908021564725703-Pension RulesDocument12 pages201908021564725703-Pension RulesanassaleemNo ratings yet