You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- Training Design SKMTDocument4 pagesTraining Design SKMTKelvin Jay Cabreros Lapada67% (9)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- (Defamation) Cassidy V Daily Mirror NewspapersDocument4 pages(Defamation) Cassidy V Daily Mirror NewspapersHoey Lee100% (4)

- SWANCOR 901-3: Epoxy Vinyl Ester ResinsDocument2 pagesSWANCOR 901-3: Epoxy Vinyl Ester ResinsSofya Andarina100% (1)

- Draft Observations For Tax Audit ReportDocument5 pagesDraft Observations For Tax Audit Reportravirockz128No ratings yet

- WWW - Csc.gov - PH - Phocadownload - MC2021 - MC No. 16, S. 2021Document6 pagesWWW - Csc.gov - PH - Phocadownload - MC2021 - MC No. 16, S. 2021esmie distorNo ratings yet

- Entering and Leaving The Traffic Separation SchemeDocument2 pagesEntering and Leaving The Traffic Separation SchemeAjay KumarNo ratings yet

- Heirs dispute over lands owned by their fatherDocument23 pagesHeirs dispute over lands owned by their fatherVeraNataaNo ratings yet

- Confidential: Infosys 29-08-2016 JUN 9 R Anvesh Banda 0 Designation Software EngineerDocument1 pageConfidential: Infosys 29-08-2016 JUN 9 R Anvesh Banda 0 Designation Software EngineerAbdul Nayeem100% (1)

- Ownership Dispute Over Corporation's RecordsDocument2 pagesOwnership Dispute Over Corporation's RecordsFrancisco Ashley AcedilloNo ratings yet

- Anarchy (c.1)Document33 pagesAnarchy (c.1)Hidde WeeversNo ratings yet

- Financial Accounting and Reporting: HTU CPA In-House Review (HCIR)Document4 pagesFinancial Accounting and Reporting: HTU CPA In-House Review (HCIR)AnonymousNo ratings yet

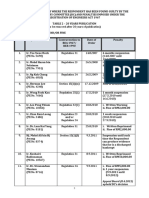

- LIST OF HEARING CASES WHERE THE RESPONDENT HAS BEEN FOUND GUILTYDocument1 pageLIST OF HEARING CASES WHERE THE RESPONDENT HAS BEEN FOUND GUILTYDarrenNo ratings yet

- The Boone and Crockett Club HistoryDocument48 pagesThe Boone and Crockett Club HistoryAmmoLand Shooting Sports NewsNo ratings yet

- ST TuesDocument34 pagesST Tuesdoug smitherNo ratings yet

- PR-1947 - Electrical Safety RulesDocument58 pagesPR-1947 - Electrical Safety Rulesjinyuan74No ratings yet

- Bicol Medical Center vs. BotorDocument4 pagesBicol Medical Center vs. BotorKharrel GraceNo ratings yet

- EPIRA (R.a 9136) - DOE - Department of Energy PortalDocument4 pagesEPIRA (R.a 9136) - DOE - Department of Energy PortalJc AlvarezNo ratings yet

- CEILLI Trial Ques EnglishDocument15 pagesCEILLI Trial Ques EnglishUSCNo ratings yet

- VDS 2095 Guidelines For Automatic Fire Detection and Fire Alarm Systems - Planning and InstallationDocument76 pagesVDS 2095 Guidelines For Automatic Fire Detection and Fire Alarm Systems - Planning and Installationjavikimi7901No ratings yet

- Why Discovery Garden Is The Right Choice For Residence and InvestmentsDocument3 pagesWhy Discovery Garden Is The Right Choice For Residence and InvestmentsAleem Ahmad RindekharabatNo ratings yet

- Feast of TrumpetsDocument4 pagesFeast of TrumpetsSonofManNo ratings yet

- San Miguel CorpDocument6 pagesSan Miguel CorpMonster BebeNo ratings yet

- Final Exam - 2013 BTC1110Document3 pagesFinal Exam - 2013 BTC1110ThomasMann100% (1)

- Chapter 2 - National Difference in Political EconomyDocument52 pagesChapter 2 - National Difference in Political EconomyTroll Nguyễn VănNo ratings yet

- Vol 4Document96 pagesVol 4rc2587No ratings yet

- FR EssayDocument3 pagesFR EssayDavid YamNo ratings yet

- COA DBM JOINT CIRCULAR NO 1 S, 2022Document7 pagesCOA DBM JOINT CIRCULAR NO 1 S, 2022AnnNo ratings yet

- Academic Test 147-2Document12 pagesAcademic Test 147-2Muhammad Usman HaiderNo ratings yet

- 4 2 Pure BendingDocument13 pages4 2 Pure BendingRubayet AlamNo ratings yet

- Philippines Supreme Court Upholds Murder ConvictionDocument4 pagesPhilippines Supreme Court Upholds Murder ConvictionJoy NavalesNo ratings yet