You might also like

- Introduction To Corporate FinanceDocument42 pagesIntroduction To Corporate FinanceshahbazNo ratings yet

- Lec 1 Finance FunctionDocument39 pagesLec 1 Finance FunctionShabrina ShaNo ratings yet

- FMCF-unit 1Document57 pagesFMCF-unit 1shagun.2224mba1003No ratings yet

- Chapter 01-The Role and Environment of Managerial FinanceDocument24 pagesChapter 01-The Role and Environment of Managerial FinancemmtusharNo ratings yet

- Introduction To Corporate FinanceDocument42 pagesIntroduction To Corporate FinancepiyushNo ratings yet

- Lecture 1 Corporate FinanceDocument5 pagesLecture 1 Corporate FinanceMd. Abdul HaiNo ratings yet

- Introduction To Corporate Finance: Chapter OneDocument25 pagesIntroduction To Corporate Finance: Chapter OneVvkps SonarNo ratings yet

- CF Topic 1Document37 pagesCF Topic 1chakri474No ratings yet

- MB20202 Corporate Finance Unit I Study MaterialsDocument17 pagesMB20202 Corporate Finance Unit I Study MaterialsSarath kumar CNo ratings yet

- Unit - I Introduction To FinanceDocument49 pagesUnit - I Introduction To FinanceShivam PalNo ratings yet

- Financial Management-2014Document114 pagesFinancial Management-2014kirankumarkakumaniNo ratings yet

- FIN3212 Lecture (Topic 1)Document10 pagesFIN3212 Lecture (Topic 1)Ooi Kean SengNo ratings yet

- FM MbaDocument77 pagesFM Mbakamalyadav5907No ratings yet

- PBF 01Document24 pagesPBF 01Masum BillahNo ratings yet

- Nature and Scope of FinanceDocument52 pagesNature and Scope of FinanceangaNo ratings yet

- Presentation 01 - Financial Manager, Goal of The Firm and Measuring Value 2013.09.20Document24 pagesPresentation 01 - Financial Manager, Goal of The Firm and Measuring Value 2013.09.20SantaAgataNo ratings yet

- Financial Management Lectures - VietnameseDocument50 pagesFinancial Management Lectures - VietnameseBình An NguyễnNo ratings yet

- Financial Management and Accounting - 1Document26 pagesFinancial Management and Accounting - 1ssmodakNo ratings yet

- Corporate FinanceDocument5 pagesCorporate FinanceHarshitKumarNo ratings yet

- Fundamental Concepts and Tools of BusineDocument51 pagesFundamental Concepts and Tools of Busineroselyn espinosaNo ratings yet

- Finance CompletedDocument9 pagesFinance CompletedJaved MemonNo ratings yet

- Financial Management: by Prof. Bhoomika TalrejaDocument43 pagesFinancial Management: by Prof. Bhoomika TalrejassmodakNo ratings yet

- Financial Management: Financial Management Refers To That Part of TheDocument19 pagesFinancial Management: Financial Management Refers To That Part of TheMayuraa ShekatkarNo ratings yet

- Course 6: The Management of CapitalDocument26 pagesCourse 6: The Management of CapitalAlif Rachmad Haidar SabiafzahNo ratings yet

- Introduction of FMDocument8 pagesIntroduction of FMMayuraa ShekatkarNo ratings yet

- Financial Management - PPT - Pgdm2010Document94 pagesFinancial Management - PPT - Pgdm2010Prabhakar Patnaik100% (1)

- Entrepreneurial FINANCE Part 1Document34 pagesEntrepreneurial FINANCE Part 1Mohammed Awwal NdayakoNo ratings yet

- Chapter 1 - Introduction To Financial ManagementDocument12 pagesChapter 1 - Introduction To Financial ManagementKarabo CollenNo ratings yet

- mb0045 FinancialManagementDocument9 pagesmb0045 FinancialManagementSaravanan VelayuthamNo ratings yet

- Corporate Finance MBA20022013Document244 pagesCorporate Finance MBA20022013Ibrahim ShareefNo ratings yet

- AccountingDocument18 pagesAccountingMursalin RabbiNo ratings yet

- Financial ManagementDocument11 pagesFinancial ManagementMadhusudhan GowdaNo ratings yet

- Objectives of Financial ManagementDocument23 pagesObjectives of Financial ManagementnarunsankarNo ratings yet

- Topic 1 Corporate FinanceDocument8 pagesTopic 1 Corporate FinanceAbdallah SadikiNo ratings yet

- Corporate Finance SummaryDocument17 pagesCorporate Finance SummaryJessyNo ratings yet

- What Is Corporate Finance? Corporate Finance Is The Field of Finance Dealing With Financial Decisions BusinessDocument26 pagesWhat Is Corporate Finance? Corporate Finance Is The Field of Finance Dealing With Financial Decisions BusinessAkhilesh PanwarNo ratings yet

- Unit 1 Introduction To Financial ManagementDocument12 pagesUnit 1 Introduction To Financial ManagementPRIYA KUMARINo ratings yet

- Assignment 1: Fundamentals: of Financial Management (FIBA 201)Document8 pagesAssignment 1: Fundamentals: of Financial Management (FIBA 201)Kshitij NegiNo ratings yet

- MGMT2023-Lecture 1-Intro To Financial ManagementDocument23 pagesMGMT2023-Lecture 1-Intro To Financial ManagementIsmadth2918388No ratings yet

- Group Four (4) Question 1 (2) Why Strategic Financial Managers Are Interested in Expected Cash Flows From A SecurityDocument10 pagesGroup Four (4) Question 1 (2) Why Strategic Financial Managers Are Interested in Expected Cash Flows From A SecurityEMMANUEL ADOVORNo ratings yet

- Lecture 1 - Nature and Scope of Financial ManagementDocument6 pagesLecture 1 - Nature and Scope of Financial ManagementAli DoyoNo ratings yet

- Assignment Financial ManagementDocument5 pagesAssignment Financial Managementhoneyverma3010No ratings yet

- Business FinanceDocument5 pagesBusiness FinanceShamim Ahmed AshikNo ratings yet

- Chapter - 1: Financial Management An IntroductionDocument21 pagesChapter - 1: Financial Management An IntroductionKrishna ChaitanyaNo ratings yet

- Fundamentals of Corporate Finance, SlideDocument250 pagesFundamentals of Corporate Finance, SlideYIN SOKHENG100% (4)

- Afm TheoryDocument4 pagesAfm TheoryMd YusufNo ratings yet

- Lecture 1-2 CF UMT Spring 2020Document32 pagesLecture 1-2 CF UMT Spring 2020ASAD ULLAHNo ratings yet

- Managing Financial Resources and DecisionsDocument18 pagesManaging Financial Resources and DecisionsAbdullahAlNomunNo ratings yet

- Overview of Financial Management: Sarita YadavDocument27 pagesOverview of Financial Management: Sarita YadavRohit SinghNo ratings yet

- Financial Management and Capital StructureDocument38 pagesFinancial Management and Capital StructureSitaKumariNo ratings yet

- Cima C04v1.5Document104 pagesCima C04v1.5amer328No ratings yet

- Corporate Finance: An: Financial Management: An Overview 1Document19 pagesCorporate Finance: An: Financial Management: An Overview 1nithish patkarNo ratings yet

- Financial Management Full NotesDocument30 pagesFinancial Management Full Notessaadsaaid0% (1)

- Unit 1 FMDocument7 pagesUnit 1 FMpurvang selaniNo ratings yet

- What Is Financial ManagementDocument7 pagesWhat Is Financial ManagementAbdul Basit ChaudhryNo ratings yet

- Debt Service Coverage Ratio (DSCR) : ValuationDocument17 pagesDebt Service Coverage Ratio (DSCR) : ValuationRh MeNo ratings yet

- FM1 IntroDocument27 pagesFM1 IntroZenedel De JesusNo ratings yet

- Financial Management - PPT - 2011Document134 pagesFinancial Management - PPT - 2011Bhanu Prakash100% (1)

- 45MB 0045-Financial ManagementDocument4 pages45MB 0045-Financial ManagementAbdullah AzadNo ratings yet

- Research Proposal PresentationDocument12 pagesResearch Proposal PresentationjahkuttaNo ratings yet

- Chapter#7 (Evaluation of Training)Document21 pagesChapter#7 (Evaluation of Training)Sadakalo ShopnooNo ratings yet

- 1 Presentation by MR Chowdhury Bangladesh FinalDocument58 pages1 Presentation by MR Chowdhury Bangladesh FinalSadakalo ShopnooNo ratings yet

- Aangul Kata Jaglu by Humayun Ahmed PDFDocument105 pagesAangul Kata Jaglu by Humayun Ahmed PDFSadakalo ShopnooNo ratings yet

- Aaj Himu-R Biye by Humayum AhmedDocument45 pagesAaj Himu-R Biye by Humayum AhmedPhysio RoNGoNNo ratings yet

- 200 Word Meaning With Synonym PDFDocument4 pages200 Word Meaning With Synonym PDFSadakalo ShopnooNo ratings yet

- RGRGRGHDocument34 pagesRGRGRGHAbdalla Mohamed AbdallaNo ratings yet

- Mid Term 2Document35 pagesMid Term 2Sadakalo ShopnooNo ratings yet

- Succession Planning ID - 153Document16 pagesSuccession Planning ID - 153Sadakalo ShopnooNo ratings yet

- 1 Presentation by MR Chowdhury Bangladesh FinalDocument58 pages1 Presentation by MR Chowdhury Bangladesh FinalSadakalo ShopnooNo ratings yet

- Socialism Capitalism and Mixed EconomyDocument7 pagesSocialism Capitalism and Mixed EconomySadakalo ShopnooNo ratings yet

- Bulmash SampleChapter2Document27 pagesBulmash SampleChapter2Raja ManiNo ratings yet

- Lecture 3 - Recruitment and SelectionDocument7 pagesLecture 3 - Recruitment and SelectionSadakalo ShopnooNo ratings yet

- Human Resource Strategies: Lecture - 4Document19 pagesHuman Resource Strategies: Lecture - 4Sadakalo ShopnooNo ratings yet

- HR StrategiesDocument16 pagesHR StrategiesGuy BrownNo ratings yet

- Successation Planning ID 158Document31 pagesSuccessation Planning ID 158Sadakalo ShopnooNo ratings yet

- Lecture - 3 Concept of S HRMDocument38 pagesLecture - 3 Concept of S HRMSadakalo ShopnooNo ratings yet

- Lecture - 5 Strategic HRM in ActionDocument27 pagesLecture - 5 Strategic HRM in ActionSadakalo Shopnoo67% (3)

- E. SKill InVentoRy............ NoteDocument6 pagesE. SKill InVentoRy............ NoteSadakalo ShopnooNo ratings yet

- Chapter#6 (Exe of T&D)Document19 pagesChapter#6 (Exe of T&D)Sadakalo ShopnooNo ratings yet

- Lecture - 2 Strategy, and Sttrategic ManagementDocument26 pagesLecture - 2 Strategy, and Sttrategic ManagementSadakalo ShopnooNo ratings yet

- Chapter - 3: RecruitmentDocument73 pagesChapter - 3: RecruitmentMaulik ModiNo ratings yet

- Demand Forecasting and Supply ForecastinDocument6 pagesDemand Forecasting and Supply ForecastinSadakalo ShopnooNo ratings yet

- Chapter#3 SocializationDocument46 pagesChapter#3 SocializationSadakalo ShopnooNo ratings yet

- Chapter 1 Introduction To TrainingDocument16 pagesChapter 1 Introduction To TrainingSadakalo Shopnoo100% (1)

- Career ManagementDocument5 pagesCareer ManagementSadakalo ShopnooNo ratings yet

- Lesson: 7 Human Resource Planning: Process, Methods, and TechniquesDocument36 pagesLesson: 7 Human Resource Planning: Process, Methods, and Techniquesranjann349No ratings yet

- Chap 7 Compensation Management2 PDFDocument12 pagesChap 7 Compensation Management2 PDFGanesh SornapudiNo ratings yet

- Chapter 8 - Orientation, TrainingDocument31 pagesChapter 8 - Orientation, TrainingSadakalo Shopnoo100% (2)

- MAC Summary of FormulasDocument25 pagesMAC Summary of FormulasRuNo ratings yet

- Sample Marketing Plan 2 - Bitis Hunter PDFDocument52 pagesSample Marketing Plan 2 - Bitis Hunter PDFMi ThưNo ratings yet

- BOB PO General Awareness Question PaperDocument6 pagesBOB PO General Awareness Question Paperkapeed_supNo ratings yet

- Arnold Van Den Berg Power Point Jan 29 2020Document60 pagesArnold Van Den Berg Power Point Jan 29 2020Gonzalo Vera MirandaNo ratings yet

- Relief Granted To Home BuyersDocument8 pagesRelief Granted To Home BuyersAkanksha DhyaniNo ratings yet

- Q3 2023 Finance Offers V1Document1 pageQ3 2023 Finance Offers V1Ad000121No ratings yet

- 06a. Information MemoDocument116 pages06a. Information Memolector_961No ratings yet

- Session 5 NewDocument79 pagesSession 5 NewFasih RehmanNo ratings yet

- Net National Product and Net Domestic IncomeDocument3 pagesNet National Product and Net Domestic IncomeLalithya Sannitha MeesalaNo ratings yet

- Signature of Depositor Signature of DepositorDocument1 pageSignature of Depositor Signature of DepositorSai Swetha KVNo ratings yet

- Chapter One: Dividend and Dividend PolicyDocument34 pagesChapter One: Dividend and Dividend PolicyEyayaw AshagrieNo ratings yet

- Purchase in The Open MarketDocument11 pagesPurchase in The Open MarketAshishNo ratings yet

- Module 2 Sources of Intermediate and Long-Term FinancingDocument24 pagesModule 2 Sources of Intermediate and Long-Term Financingcha11No ratings yet

- Forwards Futures and OptionsDocument11 pagesForwards Futures and OptionsSHELIN SHAJI 1621038No ratings yet

- Finmar FormulaDocument2 pagesFinmar FormulaCPAs AccountNo ratings yet

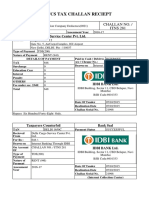

- PDF IDBI 07-10-2015 Maj Head 0021Document237 pagesPDF IDBI 07-10-2015 Maj Head 0021sunilNo ratings yet

- Assignment IDocument3 pagesAssignment IAparna RajasekharanNo ratings yet

- Unifi - Invoice Bulan 2020Document25 pagesUnifi - Invoice Bulan 2020Mich SpikeNo ratings yet

- MCom - Accounts Ch-3 Topic7Document20 pagesMCom - Accounts Ch-3 Topic7Sameer GoyalNo ratings yet

- Direct and Indirect InvestmentDocument3 pagesDirect and Indirect InvestmentShariful IslamNo ratings yet

- History: MoneyDocument68 pagesHistory: MoneyDomenico BevilacquaNo ratings yet

- NEPAL BANK LIMITED (Ram Bahadur Thapa)Document16 pagesNEPAL BANK LIMITED (Ram Bahadur Thapa)Sarose ThapaNo ratings yet

- Acknowledgement Letter Templates #03Document2 pagesAcknowledgement Letter Templates #03Ericka Grace De CastroNo ratings yet

- Er Diagram For Banking EnterpriseDocument1 pageEr Diagram For Banking EnterpriseShion K Babu50% (2)

- Perpetual Non Cumulative Preference ShareDocument11 pagesPerpetual Non Cumulative Preference ShareSiddhartha YadavNo ratings yet

- Financial Decision Making For Managers Assignment BriefDocument3 pagesFinancial Decision Making For Managers Assignment BriefAdil MahmudNo ratings yet

- CFA InstituteDocument4 pagesCFA InstituteJaya MuruganNo ratings yet

- SEBI Order On Sahara India Real Estate (June 23, 2011)Document99 pagesSEBI Order On Sahara India Real Estate (June 23, 2011)Canary TrapNo ratings yet

- LeveragesDocument9 pagesLeveragesShrinivasan IyengarNo ratings yet

- Vietnam at A Glance 4 Jan 2023Document8 pagesVietnam at A Glance 4 Jan 2023Nguyen Hoang ThoNo ratings yet