You might also like

- KSOILS Investor PresentationDocument71 pagesKSOILS Investor Presentationaimran_amirNo ratings yet

- Palm Oil (Edible Oil) : "Swad Jo Apka Dil Dhadak Dey"Document11 pagesPalm Oil (Edible Oil) : "Swad Jo Apka Dil Dhadak Dey"asdNo ratings yet

- Future of CSPO TradeDocument15 pagesFuture of CSPO TradeizzatizulaikhaNo ratings yet

- Olive Oil ReportDocument7 pagesOlive Oil ReportSarah StricklandNo ratings yet

- A Pragmatic Study On Buyers of Edible OilsDocument36 pagesA Pragmatic Study On Buyers of Edible OilsVaishnaviNo ratings yet

- Future of POL RetailingDocument18 pagesFuture of POL RetailingSuresh MalodiaNo ratings yet

- Strategic Analysis: Marico LimitedDocument8 pagesStrategic Analysis: Marico LimitedShobhit BhatnagarNo ratings yet

- Project PPT Recovered)Document18 pagesProject PPT Recovered)Pawan Puroli100% (1)

- MS Investor Presentation Jun 2011 v1Document26 pagesMS Investor Presentation Jun 2011 v1gautam_s_kNo ratings yet

- Mudranki FileDocument78 pagesMudranki Filedrashyagarg7No ratings yet

- A Pragmatic Study On Buyers of Edible OilsDocument36 pagesA Pragmatic Study On Buyers of Edible OilsNeha Motwani100% (3)

- Marico Investor Presentation - Feb14Document27 pagesMarico Investor Presentation - Feb14Tushar PatilNo ratings yet

- Mba Finance Projet 23456789101112Document58 pagesMba Finance Projet 23456789101112aryabhatmathsNo ratings yet

- Group 2Document13 pagesGroup 2Deepak SahaNo ratings yet

- A Project Report On On Indian Oil Out Lets and Bazzar Traders On Servo Lubricants at IOCLDocument58 pagesA Project Report On On Indian Oil Out Lets and Bazzar Traders On Servo Lubricants at IOCLBabasab Patil (Karrisatte)No ratings yet

- Analysis of Various Brands of Soyabean Refined Oil in The MarketDocument38 pagesAnalysis of Various Brands of Soyabean Refined Oil in The MarketDouglas OrtizNo ratings yet

- Analyst PresentationDocument20 pagesAnalyst PresentationroselilygirlNo ratings yet

- GRP - 3 - Supply Chain Edible OilDocument14 pagesGRP - 3 - Supply Chain Edible OilBhagesh KumarNo ratings yet

- Retail penetration of edible oils in HyderabadDocument27 pagesRetail penetration of edible oils in HyderabadsadafshariqueNo ratings yet

- Marketing StrategyDocument16 pagesMarketing StrategyPraveen Kumar100% (1)

- RetailDocument25 pagesRetailvmktptNo ratings yet

- Channel Conflict-Lubricant Markets-Petroleum IndustryDocument12 pagesChannel Conflict-Lubricant Markets-Petroleum IndustryNikhil100% (1)

- DIL India InvConf May 2010Document33 pagesDIL India InvConf May 2010Puneet KumarNo ratings yet

- Abhinav Srivastava By-Abhinav SrivastavaDocument76 pagesAbhinav Srivastava By-Abhinav SrivastavaAbhishek JallanNo ratings yet

- Category Attarctiveness Analysis Toilet SoapDocument26 pagesCategory Attarctiveness Analysis Toilet Soapkrunal3726No ratings yet

- Marico's brands and businessDocument26 pagesMarico's brands and businesstanyaNo ratings yet

- KNL Report - IIM IndoreDocument24 pagesKNL Report - IIM Indoredearssameer6270No ratings yet

- Marketing Management: Marico: Company AnalysisDocument14 pagesMarketing Management: Marico: Company AnalysismitulsangoiNo ratings yet

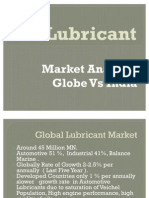

- Lubricant Market Globe Vs IndiaDocument19 pagesLubricant Market Globe Vs IndiaSandeep Walke100% (1)

- Stylol Jeans CompanyyDocument59 pagesStylol Jeans CompanyyPriyanka_Verma_103No ratings yet

- FMCG Industry Competition in IndiaDocument14 pagesFMCG Industry Competition in IndiaKshitij KatiyarNo ratings yet

- Castrol Submission TemplateDocument7 pagesCastrol Submission Templatekshitij mundra50% (2)

- Total Lubricants - Marketing StrategyDocument15 pagesTotal Lubricants - Marketing StrategyBenson Almeida82% (17)

- Presentation On Big Bazaar: Presentation by - Gurdeep Singh - Pushpak Pandey - Shaleen Agarwal - Rohan Tandon - Richa KohliDocument40 pagesPresentation On Big Bazaar: Presentation by - Gurdeep Singh - Pushpak Pandey - Shaleen Agarwal - Rohan Tandon - Richa KohliBabu SeeworldNo ratings yet

- Food WorldDocument23 pagesFood WorldGarima Jha100% (2)

- New Report RELIANCE RETAIL LTDDocument43 pagesNew Report RELIANCE RETAIL LTDPartha SarathyNo ratings yet

- Saffola Oil Marketing PlanDocument6 pagesSaffola Oil Marketing PlanPreet KapadiaNo ratings yet

- Future Outlook Indian Lub MarketDocument20 pagesFuture Outlook Indian Lub MarketPrabhu AgrawalNo ratings yet

- Healthy Oils IndiaDocument37 pagesHealthy Oils IndiabeingindraniNo ratings yet

- Company Analysis: Hindustan Uniliver LTDDocument21 pagesCompany Analysis: Hindustan Uniliver LTDmaximus077No ratings yet

- Seminar On Rice Bran OilDocument11 pagesSeminar On Rice Bran OilRahul Garg100% (2)

- in 2 Years: Hot Drinks Soft Drinks Home Care Personal Care Packaged FoodDocument4 pagesin 2 Years: Hot Drinks Soft Drinks Home Care Personal Care Packaged Foodyowan1302No ratings yet

- The Retail Niche in IndiaDocument71 pagesThe Retail Niche in IndiaPratick TibrewalaNo ratings yet

- Swot AnalysisDocument3 pagesSwot AnalysisAbhishek GuptaNo ratings yet

- Edible Oil Marketing StrategiesDocument60 pagesEdible Oil Marketing StrategiesVidya Sonawane0% (1)

- Hair Oil Note - On A Slippery Slope PDFDocument42 pagesHair Oil Note - On A Slippery Slope PDFGnanasundaram Saminathan100% (1)

- THE 4 Ps OF MARKET MIXDocument5 pagesTHE 4 Ps OF MARKET MIXGitanshNo ratings yet

- SCM - Kohinoor FoodsDocument58 pagesSCM - Kohinoor Foodszakzakzak12345No ratings yet

- Marico's journey as a leading FMCG company in IndiaDocument13 pagesMarico's journey as a leading FMCG company in IndiaYuktesh PawarNo ratings yet

- Anagha Refineries Marketting Startegy FinalDocument43 pagesAnagha Refineries Marketting Startegy FinalDeepak kNo ratings yet

- Castor Oil Derivatives: Reaching The Next OrbitDocument21 pagesCastor Oil Derivatives: Reaching The Next Orbitdkhatri01No ratings yet

- Adani Wilmar IPO NoteDocument19 pagesAdani Wilmar IPO NoteTejesh GoudNo ratings yet

- IB Report My PartDocument4 pagesIB Report My PartFurion2No ratings yet

- IIM Indore - Tough MudderDocument27 pagesIIM Indore - Tough MudderVinoRaviNo ratings yet

- RCM 09Document21 pagesRCM 09Priyajit ChandaNo ratings yet

- Model Answer: Launch of a laundry liquid detergent in Sri LankaFrom EverandModel Answer: Launch of a laundry liquid detergent in Sri LankaNo ratings yet

- Lubrication Tactics for Industries Made Simple, 8th Discipline of World Class Maintenance Management: 1, #6From EverandLubrication Tactics for Industries Made Simple, 8th Discipline of World Class Maintenance Management: 1, #6Rating: 5 out of 5 stars5/5 (1)

- 2017 International Comparison Program for Asia and the Pacific: Purchasing Power Parities and Real Expenditures—Results and MethodologyFrom Everand2017 International Comparison Program for Asia and the Pacific: Purchasing Power Parities and Real Expenditures—Results and MethodologyNo ratings yet

- Strong Supply Chains Through Resilient Operations: Five Principles for Leaders to Win in a Volatile WorldFrom EverandStrong Supply Chains Through Resilient Operations: Five Principles for Leaders to Win in a Volatile WorldNo ratings yet

- High-Frequency Trading: A Practical Guide to Algorithmic Strategies and Trading SystemsFrom EverandHigh-Frequency Trading: A Practical Guide to Algorithmic Strategies and Trading SystemsRating: 2 out of 5 stars2/5 (1)

- Neat Slides On Communication SkillsDocument19 pagesNeat Slides On Communication Skillsrajma2006No ratings yet

- Implementing Formal Project Management Process 9 Lessons LearnedDocument6 pagesImplementing Formal Project Management Process 9 Lessons LearnedyoskidavidNo ratings yet

- 10 Golden Rules of Project Risk ManagementDocument4 pages10 Golden Rules of Project Risk ManagementAlan Lisboa100% (1)

- 10 Golden Rules of Project Risk ManagementDocument4 pages10 Golden Rules of Project Risk ManagementAlan Lisboa100% (1)

- Syllabus For QTP 11 (HPO-M47) Certification Exam: o o o oDocument14 pagesSyllabus For QTP 11 (HPO-M47) Certification Exam: o o o orajma2006No ratings yet

- PM Checklist Large Projects v2.1Document4 pagesPM Checklist Large Projects v2.1Carlos Vizcarra100% (1)

- Project status reporting and stakeholder managementDocument20 pagesProject status reporting and stakeholder managementPrakash_11No ratings yet

- 10 Golden Rules of Project Risk ManagementDocument4 pages10 Golden Rules of Project Risk ManagementAlan Lisboa100% (1)

- 10 Golden Rules of Project Risk ManagementDocument4 pages10 Golden Rules of Project Risk ManagementAlan Lisboa100% (1)

- PMP Certification Exam Outline PDFDocument15 pagesPMP Certification Exam Outline PDFTemo MontyNo ratings yet

- Syllabus For QTP 11 (HPO-M47) Certification Exam: o o o oDocument14 pagesSyllabus For QTP 11 (HPO-M47) Certification Exam: o o o orajma2006No ratings yet

- Descriptive ProgrammingDocument9 pagesDescriptive Programmingrajma2006No ratings yet

- Project ManagementDocument97 pagesProject ManagementSubaruNo ratings yet

- 4do7m9tkrmgzgos6x3or Signature Poli 140901081148 Phpapp02Document1 page4do7m9tkrmgzgos6x3or Signature Poli 140901081148 Phpapp02rajma2006No ratings yet

- PMBOK UltraDocument27 pagesPMBOK Ultrapipe_182bkn100% (1)

- t-12 Sachdeva Paper PDFDocument22 pagest-12 Sachdeva Paper PDFrajma2006No ratings yet

- Test Metrics and Kpi'S: White PaperDocument14 pagesTest Metrics and Kpi'S: White Paperp.subramaniyanNo ratings yet

- 54 Fetal Death of A Twin PDFDocument3 pages54 Fetal Death of A Twin PDFrajma2006No ratings yet

- 1401 5830 PDFDocument14 pages1401 5830 PDFrajma2006No ratings yet

- TofleDocument1 pageToflerajma2006No ratings yet

- Answers ListeningDocument2 pagesAnswers Listeningrajma2006No ratings yet

- Useful Automated Software Testing MetricsDocument17 pagesUseful Automated Software Testing MetricsLê Trung TínNo ratings yet

- Firm and Fair-LeadershipDocument2 pagesFirm and Fair-Leadershiprajma2006No ratings yet

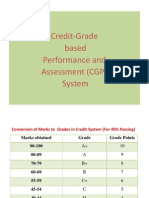

- CGPA system for credit-based performance assessmentDocument6 pagesCGPA system for credit-based performance assessmentCharles WesleyNo ratings yet

- FBI New Haven Field OfficeDocument2 pagesFBI New Haven Field Officerajma20060% (1)

- Aetnainformationsecurityassuranceprogram 140126024515 Phpapp02Document18 pagesAetnainformationsecurityassuranceprogram 140126024515 Phpapp02rajma2006No ratings yet

- Capt Khan leadership challengesDocument2 pagesCapt Khan leadership challengesrajma2006No ratings yet

- Capt Khan leadership challengesDocument2 pagesCapt Khan leadership challengesrajma2006No ratings yet

- MareskDocument23 pagesMareskrajma2006No ratings yet

- RC'S Catering MenuDocument6 pagesRC'S Catering MenuJohnmark RoblesNo ratings yet

- Effect of Television Food Advertisement On Children's Food Purchasing RequestsDocument8 pagesEffect of Television Food Advertisement On Children's Food Purchasing RequestsImran RafiqNo ratings yet

- Red Velvet Cupcake RecipeDocument3 pagesRed Velvet Cupcake RecipeAmicah Frances AntonioNo ratings yet

- Printable Recipe Book TemplateDocument54 pagesPrintable Recipe Book TemplateAgnesNo ratings yet

- Look at The Picture and Complete The PhrasesDocument5 pagesLook at The Picture and Complete The PhrasesFaisal33% (3)

- Guidance On Unruly Passenger Prevention and ManagementDocument70 pagesGuidance On Unruly Passenger Prevention and ManagementMedTaïebBenTekayaNo ratings yet

- Three Days of HappinessDocument217 pagesThree Days of Happinessnazrul2islam_1100% (3)

- Classification of VegetablesDocument41 pagesClassification of VegetablesRoselleAntonioVillajuanLinsangan100% (2)

- Sanjay Routray: General Manager, 12Document4 pagesSanjay Routray: General Manager, 12Sanjaya RoutrayNo ratings yet

- Etilism Cronic - Chiriță David, Ilie-Constantinescu Alexandru, Ipatov Antonie, Sukkar Shady PDFDocument3 pagesEtilism Cronic - Chiriță David, Ilie-Constantinescu Alexandru, Ipatov Antonie, Sukkar Shady PDFDavid ChiritaNo ratings yet

- Density LabDocument2 pagesDensity LababdallaaNo ratings yet

- Grappa HandbookDocument66 pagesGrappa HandbookPetr CiglerNo ratings yet

- Tips On Growing Up!Document13 pagesTips On Growing Up!lels1323No ratings yet

- Indian School Muscat: Department of Arabic Class:Ix Lessons TranslationDocument4 pagesIndian School Muscat: Department of Arabic Class:Ix Lessons TranslationDeepak RameshNo ratings yet

- Spindrift Brand AnalysisDocument6 pagesSpindrift Brand Analysisapi-260100515No ratings yet

- Amul IcecreamDocument8 pagesAmul IcecreamParas PathelaNo ratings yet

- Kissan Squash Uses Preservatives and High Amount of Sugar Which at This Covid-19 Situation Is Not Commendable As at This Time Everyone Needs Immunity ProductsDocument2 pagesKissan Squash Uses Preservatives and High Amount of Sugar Which at This Covid-19 Situation Is Not Commendable As at This Time Everyone Needs Immunity Productsharendra choudharyNo ratings yet

- PetrenDocument55 pagesPetrenJoanna PiekarskaNo ratings yet

- Trader Joe's unique product differentiation strategyDocument1 pageTrader Joe's unique product differentiation strategyrcbcsk cskNo ratings yet

- Joint and by Products Costing 11012019Document74 pagesJoint and by Products Costing 11012019Christine Mae MataNo ratings yet

- Sims Recycling CenterDocument12 pagesSims Recycling Centerapi-285693263No ratings yet

- The Dirty Glass ChordsDocument3 pagesThe Dirty Glass ChordsSHANENo ratings yet

- Funnyjunk Items ChecklistDocument11 pagesFunnyjunk Items Checklistb8ee1No ratings yet

- My Accidental Love Is You Chapter 1Document12 pagesMy Accidental Love Is You Chapter 1Brithania Zelvira ZelviraNo ratings yet

- Gueridon Service Reference BookletDocument53 pagesGueridon Service Reference BookletManolo Solano100% (2)

- Napoleon's Oraculum and Dream BookDocument68 pagesNapoleon's Oraculum and Dream Booksocratesplato100% (2)

- Burnside PS students make 1200 paper cranes for injured teacherDocument7 pagesBurnside PS students make 1200 paper cranes for injured teacherashmitashrivasNo ratings yet

- The Golden HarvestDocument3 pagesThe Golden HarvestMark Angelo DiazNo ratings yet

- Methylated SpiritDocument7 pagesMethylated SpiritPiNo ratings yet

- Origins and Evolution of Our Fellowship Volume 1Document110 pagesOrigins and Evolution of Our Fellowship Volume 1Jay Smith100% (2)