You might also like

- Basel III norms summaryDocument14 pagesBasel III norms summarynidazaidi1989No ratings yet

- POSITIVIST IntitutionalismDocument13 pagesPOSITIVIST IntitutionalismRiesel TumangNo ratings yet

- Chile - The Latin American Tiger - v1 1Document17 pagesChile - The Latin American Tiger - v1 1Ramyaa RameshNo ratings yet

- The Federalist PeriodDocument39 pagesThe Federalist Periodapi-328120679No ratings yet

- Imf & SDRDocument48 pagesImf & SDRAprajita SharmaNo ratings yet

- Latin American Integration Organizations ComparedDocument51 pagesLatin American Integration Organizations ComparedAndres AguileraNo ratings yet

- Part 3 Neoclassical Economic Thought and Its CriticsDocument35 pagesPart 3 Neoclassical Economic Thought and Its CriticsFe MagbooNo ratings yet

- PPTDocument21 pagesPPTRazan TataiNo ratings yet

- MercantilismDocument30 pagesMercantilismadeel499No ratings yet

- 09 Institutionalist SchoolDocument36 pages09 Institutionalist SchoolHeap Ke XinNo ratings yet

- Cuba and U SDocument20 pagesCuba and U Sapi-316953628No ratings yet

- Market Vs State DebateDocument30 pagesMarket Vs State Debatehuzefaratawala2No ratings yet

- David RicardoDocument41 pagesDavid RicardoEduardo AcostaNo ratings yet

- Chapter 3Document22 pagesChapter 3Akash JainNo ratings yet

- Presentation - John Stuart MillDocument21 pagesPresentation - John Stuart Millmaam5a_93No ratings yet

- The Clash of The Cabinet: USHC 1.6Document25 pagesThe Clash of The Cabinet: USHC 1.6yomomslilybuums100% (1)

- InterrelatedDocument2 pagesInterrelatedRaz MahariNo ratings yet

- Chapter03 Central+BankDocument13 pagesChapter03 Central+BankInamullah KhanNo ratings yet

- The European Central BankDocument12 pagesThe European Central BankhishamsaukNo ratings yet

- Early Republic - WashingtonDocument12 pagesEarly Republic - Washingtonapi-305127889No ratings yet

- Macroeconomics and Say's LawDocument20 pagesMacroeconomics and Say's Lawrajarshi raghuvanshiNo ratings yet

- Govt R.C College of Commerce & Management International BusinessDocument17 pagesGovt R.C College of Commerce & Management International BusinessManasa PuttaswamyNo ratings yet

- Financialsation & CrisisDocument20 pagesFinancialsation & CrisissushilkhannaNo ratings yet

- Latin AmericaDocument169 pagesLatin AmericaAakashAgrawal_01No ratings yet

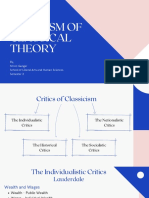

- Criticism of Classical TheoryDocument28 pagesCriticism of Classical TheoryShruti Gangar100% (1)

- Evolution of Money and BankingDocument17 pagesEvolution of Money and BankingUmar HayatNo ratings yet

- Money, The Price Level, and InflationDocument61 pagesMoney, The Price Level, and InflationGianella Zoraya Torres AscurraNo ratings yet

- Contribution Adam SmithDocument33 pagesContribution Adam SmithLohith N ReddyNo ratings yet

- MERCANTILIST (5 Basic Questions)Document25 pagesMERCANTILIST (5 Basic Questions)Kuang Yong NgNo ratings yet

- Structure of Indian EconomyDocument18 pagesStructure of Indian Economykartii_123No ratings yet

- Multiplier EffectDocument25 pagesMultiplier EffecteuwillaNo ratings yet

- Interview Questions EconomicsDocument1 pageInterview Questions EconomicsManoj KNo ratings yet

- Aggregate Demand and Aggregate SupplyDocument24 pagesAggregate Demand and Aggregate SupplyAri HaranNo ratings yet

- Unit 1 Criticism of The Neo-Classical Theory of The Firm The Marginalist ControversyDocument74 pagesUnit 1 Criticism of The Neo-Classical Theory of The Firm The Marginalist ControversySaim IjazNo ratings yet

- Revealed Preference TheoremDocument10 pagesRevealed Preference TheoremelinexaxaNo ratings yet

- Eco - Ed. 428 Nepalese EconomyDocument7 pagesEco - Ed. 428 Nepalese EconomyHari PrasadNo ratings yet

- Mercantilism Vs Physiocracy: The Brief Intro, Contribution, Pros & ConsDocument8 pagesMercantilism Vs Physiocracy: The Brief Intro, Contribution, Pros & ConsDaniyaNaiduNo ratings yet

- IFM5 Exc Rate Theories Parity ConditionsDocument42 pagesIFM5 Exc Rate Theories Parity Conditionsashu khetan100% (1)

- Geopolitics in Latin AmericaDocument35 pagesGeopolitics in Latin AmericaLö Räine AñascoNo ratings yet

- Central BankingDocument28 pagesCentral Bankingneha16septNo ratings yet

- Recrdian Theory of RentDocument1 pageRecrdian Theory of Rentkumarrohit007No ratings yet

- Major Difference Between Micro and Macro EconomicsDocument7 pagesMajor Difference Between Micro and Macro EconomicsHaren ShylakNo ratings yet

- Cash Transactions Approach To MoneyDocument8 pagesCash Transactions Approach To MoneyAppan Kandala Vasudevachary100% (2)

- Notes - EconomicsDocument69 pagesNotes - EconomicsHaktan OdabasiNo ratings yet

- 3 (1) .How Did Adam Smith Criticize MercantilismDocument18 pages3 (1) .How Did Adam Smith Criticize Mercantilismbarouyrtek100% (1)

- CH-2 Basic Concept of Macroeconomics PDFDocument16 pagesCH-2 Basic Concept of Macroeconomics PDF1630 Gursimran Saluja ANo ratings yet

- Definition of Barter SystemDocument10 pagesDefinition of Barter Systemzeeshan 3240No ratings yet

- The World Bank and Its CriticsDocument14 pagesThe World Bank and Its CriticsNayana SinghNo ratings yet

- Unit 3 Classical Theory of Employment.Document54 pagesUnit 3 Classical Theory of Employment.Anshumaan PatroNo ratings yet

- Balanced Growth TheoryDocument18 pagesBalanced Growth TheorySWETCHCHA MISKA100% (1)

- International Marketing, Customs Union, Free Trade Area, Common Market!!Document14 pagesInternational Marketing, Customs Union, Free Trade Area, Common Market!!Jas777100% (1)

- High Powered MoneyDocument9 pagesHigh Powered MoneyVikas BhaduNo ratings yet

- International Economics ExplainedDocument82 pagesInternational Economics ExplainedS. Shanmugasundaram100% (1)

- New ECONOMICS NEP Syllabus Revised 2Document25 pagesNew ECONOMICS NEP Syllabus Revised 2Chotu KumarNo ratings yet

- CIE Igcse E (0455) : ConomicsDocument15 pagesCIE Igcse E (0455) : ConomicsChutiaNo ratings yet

- Gruber4e ch07Document28 pagesGruber4e ch07Ummi RahmawatiNo ratings yet

- The Politics of Inflation: A Comparative AnalysisFrom EverandThe Politics of Inflation: A Comparative AnalysisRichard MedleyNo ratings yet

- Macroeconomics-I (Chapter 1 & 2)Document80 pagesMacroeconomics-I (Chapter 1 & 2)S Tariku GarseNo ratings yet

- Founding Fathers of MacroeconomicsDocument25 pagesFounding Fathers of Macroeconomicsmonster_newinNo ratings yet

- Restful Web Services: National Institute of Technology, RourkelaDocument10 pagesRestful Web Services: National Institute of Technology, RourkelamohitNo ratings yet

- SolutionsDocument9 pagesSolutionsmohitNo ratings yet

- Rahul Banerji (Samsung Open Source Team) : (O-RAN - WG3.E2AP-v01.01)Document14 pagesRahul Banerji (Samsung Open Source Team) : (O-RAN - WG3.E2AP-v01.01)mohitNo ratings yet

- O-DU High Sprint 4 DemoDocument18 pagesO-DU High Sprint 4 DemomohitNo ratings yet

- Philosophiæ Naturalis Principia Mathematica by Isaac Newton Sectio 1Document11 pagesPhilosophiæ Naturalis Principia Mathematica by Isaac Newton Sectio 1mohitNo ratings yet

- Strategy To Calculate LimitsDocument2 pagesStrategy To Calculate LimitsmohitNo ratings yet

- Moment of Inertia of Various Sysytems Iit JeeDocument1 pageMoment of Inertia of Various Sysytems Iit JeetrurturtNo ratings yet

- 30 2 CarsonDocument14 pages30 2 Carsonrussell_mahmoodNo ratings yet

- Chapter-8 Work, Power & Energy (II)Document14 pagesChapter-8 Work, Power & Energy (II)mohitNo ratings yet

- Presentation 1Document14 pagesPresentation 1mohit100% (1)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- Literature Study of HospitalDocument18 pagesLiterature Study of HospitalJasleen KaurNo ratings yet

- Mathematics I A (EM) BLM 2021-22Document130 pagesMathematics I A (EM) BLM 2021-22Pranav AdithyaNo ratings yet

- Kareem Shagar Formation An Oil Field Located in Ras Gharib DevelopmentDocument53 pagesKareem Shagar Formation An Oil Field Located in Ras Gharib Developmentwisam alkhooryNo ratings yet

- Lab Manual: Shree Ramchandra College of Engineering, Lonikand, Pune - 412 216Document43 pagesLab Manual: Shree Ramchandra College of Engineering, Lonikand, Pune - 412 216jatindraNo ratings yet

- Propp MorphologyDocument10 pagesPropp MorphologyFilippo CostanzoNo ratings yet

- SS 18 Home ScienceDocument8 pagesSS 18 Home ScienceJaswant SharmaNo ratings yet

- Subject Centered - Correlational DesignDocument13 pagesSubject Centered - Correlational DesignWarrenBualoySayagoNo ratings yet

- Book QuantLibDocument40 pagesBook QuantLibPradeep Srivatsava ManikondaNo ratings yet

- Cast StudyDocument5 pagesCast StudyFrancisco Rodriguez0% (3)

- Macintosh 12" Monochrome Display Service ManualDocument61 pagesMacintosh 12" Monochrome Display Service ManualAnatoli KrasilnikovNo ratings yet

- Twilio Best Practices Sample ChapterDocument36 pagesTwilio Best Practices Sample ChapterPackt Publishing100% (1)

- KK Apuntes Sap 01Document3 pagesKK Apuntes Sap 01Smith F. JohnNo ratings yet

- Toyota TVIP System ProgrammingDocument11 pagesToyota TVIP System Programmingcheerios353No ratings yet

- Instructions Before Starting The Test: WWW - Cuims.inDocument3 pagesInstructions Before Starting The Test: WWW - Cuims.inYogeshNo ratings yet

- Material Didáctico Unidades 7 A 9Document122 pagesMaterial Didáctico Unidades 7 A 9Romina Soledad KondratiukNo ratings yet

- Experiment 2 Post LabDocument7 pagesExperiment 2 Post LabM ReyNo ratings yet

- IDBC-TS-MTTDS-FGR623304 Rev 50 Production Flowline Pig ReceiverDocument18 pagesIDBC-TS-MTTDS-FGR623304 Rev 50 Production Flowline Pig ReceiverTifano KhristiyantoNo ratings yet

- The Philippine Tourism Master Plan 1991-2010Document7 pagesThe Philippine Tourism Master Plan 1991-2010Zcephra MalsiNo ratings yet

- p640 1Document21 pagesp640 1Mark CheneyNo ratings yet

- Articulator Selection For Restorative DentistryDocument9 pagesArticulator Selection For Restorative DentistryAayushi VaidyaNo ratings yet

- Chapter 3 Developing The Whole PersonDocument15 pagesChapter 3 Developing The Whole PersonRocel DomingoNo ratings yet

- 09931017A Clarus SQ8 MS Hardware GuideDocument162 pages09931017A Clarus SQ8 MS Hardware GuidePaola Cardozo100% (2)

- Antiviral Agents and Infection ControlDocument94 pagesAntiviral Agents and Infection ControlKimberly GeorgeNo ratings yet

- RazorCMS Theme GuideDocument14 pagesRazorCMS Theme GuideAngela HolmesNo ratings yet

- 13 Chapter7Document19 pages13 Chapter7Bharg KaleNo ratings yet

- Design and Construction of A Tower Crane: June 2009Document6 pagesDesign and Construction of A Tower Crane: June 2009Beza GetachewNo ratings yet

- The Problem and Its SettingDocument20 pagesThe Problem and Its SettingChing DialomaNo ratings yet

- Calculating Cost of Goods Sold and Gross Profit From Financial Statements</bDocument8 pagesCalculating Cost of Goods Sold and Gross Profit From Financial Statements</bGrace A. Manalo100% (1)

- Catalogo Weichai 2020Document106 pagesCatalogo Weichai 2020Jose AntonioNo ratings yet

- Bus Conductor Design and ApplicationsDocument70 pagesBus Conductor Design and ApplicationsJithinNo ratings yet