You might also like

- T R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)From EverandT R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)No ratings yet

- Microfinance: The New Dimension in Financial SectorDocument10 pagesMicrofinance: The New Dimension in Financial SectorGaurav ParekhNo ratings yet

- Banking India: Accepting Deposits for the Purpose of LendingFrom EverandBanking India: Accepting Deposits for the Purpose of LendingNo ratings yet

- Muslim Commercial BankDocument20 pagesMuslim Commercial BankMBA...KID100% (4)

- Understanding Commerce: A High School Student’S CompanionFrom EverandUnderstanding Commerce: A High School Student’S CompanionNo ratings yet

- Submitted By: Mahesh Raut IB Anand - Iim JammuDocument9 pagesSubmitted By: Mahesh Raut IB Anand - Iim JammuAnandNo ratings yet

- Banking in Africa: Delivering on Financial Inclusion, Supporting Financial StabilityFrom EverandBanking in Africa: Delivering on Financial Inclusion, Supporting Financial StabilityNo ratings yet

- Financial System of China: Lecturer - Oleg Deev Oleg@mail - Muni.czDocument37 pagesFinancial System of China: Lecturer - Oleg Deev Oleg@mail - Muni.czSaurabh BhirudNo ratings yet

- Analysis of Financial Statements Arif Habib BankDocument18 pagesAnalysis of Financial Statements Arif Habib BankMBA...KIDNo ratings yet

- Rural Banking - 1Document16 pagesRural Banking - 1Ye' Thi HaNo ratings yet

- Islamic Banking: Presented By: Neha RafiqueDocument18 pagesIslamic Banking: Presented By: Neha RafiqueAli JumaniNo ratings yet

- Banking Sector in IndiaDocument29 pagesBanking Sector in Indiahahire0% (1)

- Bank Alfalah FinalDocument62 pagesBank Alfalah FinalSaba AzharNo ratings yet

- Banking N Session-4 & 5Document49 pagesBanking N Session-4 & 5Vaibhav AggarwalNo ratings yet

- Final HBL PresentationDocument75 pagesFinal HBL PresentationShehzaib Sunny100% (4)

- Marketing Plan For YES AccountDocument52 pagesMarketing Plan For YES AccountVame ApiNo ratings yet

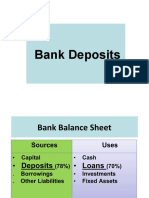

- DepositsDocument37 pagesDepositsHarshita SahiNo ratings yet

- NBP Presentation (Final)Document62 pagesNBP Presentation (Final)Mudassir Saeed0% (1)

- Developing Products For Rural Markets: Annie Duflo Centre For Micro Finance at IFMR February 14, 2007Document57 pagesDeveloping Products For Rural Markets: Annie Duflo Centre For Micro Finance at IFMR February 14, 2007sharmi8No ratings yet

- Help Us To Help You!!!: A Presentation By: JasleenDocument20 pagesHelp Us To Help You!!!: A Presentation By: Jasleenjasleen1No ratings yet

- Managing Credit Risk and Loan PoliciesDocument81 pagesManaging Credit Risk and Loan PoliciesSubhajit KarmakarNo ratings yet

- Call Money Market: Features, Participants and Role of RBIDocument21 pagesCall Money Market: Features, Participants and Role of RBIjames40440No ratings yet

- Icici BankDocument59 pagesIcici BankChetan JanardhanaNo ratings yet

- Microfinanc E: Iobm PakistanDocument44 pagesMicrofinanc E: Iobm Pakistanfujimukazu100% (1)

- Microfinanc E: By: Fariha & ArsalanDocument44 pagesMicrofinanc E: By: Fariha & ArsalanSushil KarnaNo ratings yet

- SBI & The Banking IndustryDocument12 pagesSBI & The Banking IndustryIshita JainNo ratings yet

- Banking Industry AnalysisDocument33 pagesBanking Industry Analysismjibran_1100% (1)

- Problems Faced by Commercial BanksDocument29 pagesProblems Faced by Commercial BanksPantula ChandanaNo ratings yet

- Latest Trends in BankingDocument98 pagesLatest Trends in BankingViji Ranga0% (1)

- Final Presentation on The Power to Lead HBL Products and ServicesDocument75 pagesFinal Presentation on The Power to Lead HBL Products and ServicesWajiha AliNo ratings yet

- Industry Reports - ISB Consulting Casebook 2021Document36 pagesIndustry Reports - ISB Consulting Casebook 2021BalajiNo ratings yet

- Bank AlfalahDocument46 pagesBank AlfalahSaba AzharNo ratings yet

- Topic 013: Introduction To Financial EnvironmentDocument21 pagesTopic 013: Introduction To Financial EnvironmentsarahNo ratings yet

- Liquidity Management by Islamic BanksDocument9 pagesLiquidity Management by Islamic BanksMiran shah chowdhury100% (3)

- Housing Finance FMG18YDocument80 pagesHousing Finance FMG18YMadhusudan PartaniNo ratings yet

- Commercial Bank ManagementDocument38 pagesCommercial Bank ManagementAikya Gandhi100% (1)

- Retail Banking in India - The Comprehensive Industry ReportDocument4 pagesRetail Banking in India - The Comprehensive Industry Reportankit71420No ratings yet

- Week 5.pptx - WatermarkDocument57 pagesWeek 5.pptx - Watermarkkhushi jaiswalNo ratings yet

- Bank MarketingDocument31 pagesBank MarketingOmar FarukNo ratings yet

- Team - Finacs - Mergers & Acquisition Document in Banking IndustryDocument21 pagesTeam - Finacs - Mergers & Acquisition Document in Banking IndustryankurchorariaNo ratings yet

- Financial Regulation PPT 1Document19 pagesFinancial Regulation PPT 1Tania GhoshNo ratings yet

- 1 - Historical Growth Future OutlookDocument42 pages1 - Historical Growth Future Outlookahsanjaved2021No ratings yet

- Sheam. Bank Management.-1Document121 pagesSheam. Bank Management.-1SM SheamNo ratings yet

- Financial Inclusion PPT 2Document14 pagesFinancial Inclusion PPT 2JanhaviNo ratings yet

- Public V/S Private Sector Banks ComparisonDocument64 pagesPublic V/S Private Sector Banks ComparisonRanjith AlappadanNo ratings yet

- Indian Financial System - CIADocument12 pagesIndian Financial System - CIASamar GhorpadeNo ratings yet

- Service IndustryDocument27 pagesService IndustryheenasapriyaNo ratings yet

- Banking Products & Operations: Session 7Document34 pagesBanking Products & Operations: Session 7Vaidyanathan RavichandranNo ratings yet

- Call Money MarketDocument21 pagesCall Money MarketAakanksha SanctisNo ratings yet

- SBIDocument12 pagesSBIHemlata Kale50% (2)

- HABIB BANK LIMITED HISTORYDocument32 pagesHABIB BANK LIMITED HISTORYĤȜƛrț ĦaȼǩȜřNo ratings yet

- Overview of Islamic FinanceDocument24 pagesOverview of Islamic Financesoorajdivakaran3650100% (1)

- Banking SectorDocument12 pagesBanking SectorasifanisNo ratings yet

- Managing Financial Institutions Course OverviewDocument106 pagesManaging Financial Institutions Course OverviewDevica UditramNo ratings yet

- Banking in PakistanDocument11 pagesBanking in PakistanAdeel RanaNo ratings yet

- Swot Analysis: StrengthsDocument10 pagesSwot Analysis: StrengthsArslan Tariq MalikNo ratings yet

- Sector Overview On Indian Banking Industry: BY BhausahebDocument38 pagesSector Overview On Indian Banking Industry: BY BhausahebPranavNo ratings yet

- Banking System in IndiaDocument47 pagesBanking System in IndiaPallabi PattanayakNo ratings yet

- SWOT Analysis of Indian Banking IndustryDocument14 pagesSWOT Analysis of Indian Banking IndustryAnjnaKandariNo ratings yet

- Microfinance: Vinay Desai Milan Malik Garima Jindal Mayank Golchha Abhinava Chanda Nilesh AnandparaDocument29 pagesMicrofinance: Vinay Desai Milan Malik Garima Jindal Mayank Golchha Abhinava Chanda Nilesh AnandparadaputhechampNo ratings yet

- MAVMADE & CUP CAKES BY ZEHRA KHAN Cake & Cupcake FlavorsDocument2 pagesMAVMADE & CUP CAKES BY ZEHRA KHAN Cake & Cupcake FlavorshinamustafaNo ratings yet

- Baking ConversionsDocument1 pageBaking ConversionshinamustafaNo ratings yet

- Central Region Product Sales Report 2007Document61 pagesCentral Region Product Sales Report 2007hinamustafaNo ratings yet

- Reference LetterDocument2 pagesReference LetterhinamustafaNo ratings yet

- CB - FinalDocument6 pagesCB - FinalhinamustafaNo ratings yet

- NFL RevisedDocument5 pagesNFL RevisedhinamustafaNo ratings yet

- NFL RevisedDocument5 pagesNFL RevisedhinamustafaNo ratings yet

- ACCA FM (F9) Course Notes PDFDocument229 pagesACCA FM (F9) Course Notes PDFBilal AhmedNo ratings yet

- IPO Note SBFC Finance LTDDocument14 pagesIPO Note SBFC Finance LTDKrishna GoyalNo ratings yet

- Credit Acceptance Corp The Black Swan EventDocument13 pagesCredit Acceptance Corp The Black Swan EventhpatnerNo ratings yet

- Descriptions For NAHB COA AccountsDocument67 pagesDescriptions For NAHB COA AccountsdumpNo ratings yet

- Mifos - Data - SheetJuly 2015 PDFDocument4 pagesMifos - Data - SheetJuly 2015 PDFmariaduque9No ratings yet

- Your Account Statement: Payment Information Summary of Account ActivityDocument4 pagesYour Account Statement: Payment Information Summary of Account ActivityAndreina VillalobosNo ratings yet

- Prudential Bank vs Alviar: Dragnet Clause and Reliance on Security TestDocument2 pagesPrudential Bank vs Alviar: Dragnet Clause and Reliance on Security TestRufino Gerard Moreno67% (3)

- 16 Week PlanDocument5 pages16 Week PlanAliza IshraNo ratings yet

- Math 1090Document8 pagesMath 1090api-287030709No ratings yet

- MSC Thesis ProposalDocument47 pagesMSC Thesis ProposalEric Osei Owusu-kumihNo ratings yet

- Financial Analysis of a Selected CompanyDocument20 pagesFinancial Analysis of a Selected CompanyDavid SamuelNo ratings yet

- Msi Owner Occupancy AffidavitDocument1 pageMsi Owner Occupancy AffidavitbatinatorNo ratings yet

- Office of The Team Leader: Commission On AuditDocument4 pagesOffice of The Team Leader: Commission On Auditrussel1435100% (1)

- Cash Flow Basics: Track Inflows & OutflowsDocument12 pagesCash Flow Basics: Track Inflows & OutflowsMARY IRISH FAITH PATAJONo ratings yet

- Unit 4 Written Assignment BUS 2203: Principles of Finance 1 University of The People Galin TodorovDocument5 pagesUnit 4 Written Assignment BUS 2203: Principles of Finance 1 University of The People Galin TodorovMarcusNo ratings yet

- Topic 5: International Lending and Portfolio ManagementDocument29 pagesTopic 5: International Lending and Portfolio ManagementSanthiya MogenNo ratings yet

- Banker's guide to credit management from IIBFDocument3 pagesBanker's guide to credit management from IIBFRahul Pandey27% (11)

- He 9780199276080 Chapter 17Document55 pagesHe 9780199276080 Chapter 17RobinNo ratings yet

- Cibil ReportDocument3 pagesCibil Reportbajaj enterprisesNo ratings yet

- How the Big Short exposed flaws in the US mortgage marketDocument2 pagesHow the Big Short exposed flaws in the US mortgage marketPedro HacheNo ratings yet

- The Impact of Credit Policy On Improving Vietnamese Household Living Standards in The Time of Covid 19 Pandemic - 20230228 - 020555Document49 pagesThe Impact of Credit Policy On Improving Vietnamese Household Living Standards in The Time of Covid 19 Pandemic - 20230228 - 020555Phương ThảoNo ratings yet

- DPCDocument16 pagesDPCShikhar SrivastavNo ratings yet

- Intermediate Accounting 1 - Loans Receivable ProblemsDocument1 pageIntermediate Accounting 1 - Loans Receivable ProblemsJanidelle Swiftie67% (3)

- Radian Default Claims Servicing GuideDocument42 pagesRadian Default Claims Servicing GuidelostvikingNo ratings yet

- Unit # 5 Problems Related TVMDocument5 pagesUnit # 5 Problems Related TVMZaheer Ahmed SwatiNo ratings yet

- Maybank Report MFRS 139 Project Loan AnalysisDocument3 pagesMaybank Report MFRS 139 Project Loan AnalysispalmkodokNo ratings yet

- Personal Finance - Introduction Ver 0.4Document59 pagesPersonal Finance - Introduction Ver 0.4Aravind MenonNo ratings yet

- Assessment of Working Capital LimitDocument4 pagesAssessment of Working Capital LimitKeshav Malpani100% (8)

- General FAQs For The New SABBMobileDocument3 pagesGeneral FAQs For The New SABBMobileSajad PkNo ratings yet

- Working Capital Management of Hero Motocorp Limited: November 2019Document17 pagesWorking Capital Management of Hero Motocorp Limited: November 2019Venu Gopal J S100% (1)