You might also like

- Cellular Technologies for Emerging Markets: 2G, 3G and BeyondFrom EverandCellular Technologies for Emerging Markets: 2G, 3G and BeyondNo ratings yet

- The Industry HandbookDocument7 pagesThe Industry HandbookknnoknnoNo ratings yet

- Papers on the field: Telecommunication Economic, Business, Regulation & PolicyFrom EverandPapers on the field: Telecommunication Economic, Business, Regulation & PolicyNo ratings yet

- Telecom Sector Porter's 5 Force AnalysisDocument3 pagesTelecom Sector Porter's 5 Force AnalysisKARTIK ANAND100% (1)

- Porter Five Forces WordDocument11 pagesPorter Five Forces WordvinodvahoraNo ratings yet

- Technical, Commercial and Regulatory Challenges of QoS: An Internet Service Model PerspectiveFrom EverandTechnical, Commercial and Regulatory Challenges of QoS: An Internet Service Model PerspectiveNo ratings yet

- CRM Project Report PDFDocument12 pagesCRM Project Report PDFSobhra SatpathyNo ratings yet

- The Industry HandbookDocument13 pagesThe Industry HandbookRenu NerlekarNo ratings yet

- The Industry Handbook: The Telecommunications Industry: Printer Friendly Version (PDF Format)Document3 pagesThe Industry Handbook: The Telecommunications Industry: Printer Friendly Version (PDF Format)Aman DeepNo ratings yet

- PORTER 5 ForcesDocument4 pagesPORTER 5 ForcesMiley MartinNo ratings yet

- Project Report Final1.1Document74 pagesProject Report Final1.1adsfdgfhgjhkNo ratings yet

- Report Telecoms - EY - 2015 - Global Telecoms Digital PlaybookDocument53 pagesReport Telecoms - EY - 2015 - Global Telecoms Digital Playbookagudo64100% (1)

- Nureye ASSIGNMENTDocument24 pagesNureye ASSIGNMENTZeyinA MohammedNo ratings yet

- Business Strategy Assignment - Final TelecomDocument10 pagesBusiness Strategy Assignment - Final TelecomAishwarya SankhlaNo ratings yet

- Objective of The Study: Literature ReviewDocument15 pagesObjective of The Study: Literature ReviewAanchal PatnahaNo ratings yet

- Customer Satisfaction On Reliance Infocomm: A Summer Training Project Report ONDocument41 pagesCustomer Satisfaction On Reliance Infocomm: A Summer Training Project Report ONTripta SainiNo ratings yet

- Supply Chain Management and Telecom ComponentsDocument5 pagesSupply Chain Management and Telecom Componentsmodern2308No ratings yet

- Group Work - AirtelDocument2 pagesGroup Work - AirtelDEEPAK KUMARNo ratings yet

- The Relevance of Data in The Telecommunication IndustryDocument14 pagesThe Relevance of Data in The Telecommunication IndustryChiylove ChiyloveNo ratings yet

- The Evolution of Voip: A Look Into How Voip Has Proliferated Into The Global Dominant Platform It Is TodayDocument48 pagesThe Evolution of Voip: A Look Into How Voip Has Proliferated Into The Global Dominant Platform It Is TodayBradley SusserNo ratings yet

- Future Business Opportunities and ChallengesDocument15 pagesFuture Business Opportunities and ChallengesChiylove ChiyloveNo ratings yet

- What Is An IndustryDocument8 pagesWhat Is An IndustrypritamNo ratings yet

- IMS Next Gen Comm Networks 080905Document16 pagesIMS Next Gen Comm Networks 080905api-3807600No ratings yet

- Analysis of Vodafone Essar IndiaDocument34 pagesAnalysis of Vodafone Essar Indiachapal07No ratings yet

- Telecom Industry Analysis in IndiaDocument15 pagesTelecom Industry Analysis in IndiaAdhiraj KarmakarNo ratings yet

- SWOT ANALYSIS Chapter SixDocument8 pagesSWOT ANALYSIS Chapter SixSetu MehtaNo ratings yet

- Best Practice Guide West Africa (2013:4)Document8 pagesBest Practice Guide West Africa (2013:4)Kwame AsamoaNo ratings yet

- Industry and Market AnalysesDocument6 pagesIndustry and Market AnalysespunjtanyaNo ratings yet

- 1.1 Telecom Sector: A Global Scenario: Mobile TelephonyDocument23 pages1.1 Telecom Sector: A Global Scenario: Mobile TelephonyNeha KumarNo ratings yet

- Different Frameworks of Strategy in Telecom IndustryDocument12 pagesDifferent Frameworks of Strategy in Telecom IndustrySHIDHARTH RAJ MBA Kolkata 2022-24No ratings yet

- Report On Industry, Competitive, SPACE Matrix Analysis For Telecom Industry - TATA Tele Services, Bharti AirtelDocument18 pagesReport On Industry, Competitive, SPACE Matrix Analysis For Telecom Industry - TATA Tele Services, Bharti AirtelankitsuroliaNo ratings yet

- PaperDocument22 pagesPapernishant_singhal_4No ratings yet

- Spectrum Report ColeagoDocument49 pagesSpectrum Report Coleagowalia_anujNo ratings yet

- Presentation On Airtel and Cell Phone Service IndustryDocument37 pagesPresentation On Airtel and Cell Phone Service Industrygagan15095895No ratings yet

- Telecom Industry AnalysisDocument5 pagesTelecom Industry AnalysisSana NusratNo ratings yet

- HRM RelianceDocument78 pagesHRM Reliancemanwanimuki12No ratings yet

- Comsumer Behaviour Project ReportDocument39 pagesComsumer Behaviour Project ReportAbhijeet VatsNo ratings yet

- DOCOMO Assignment Questions-1Document4 pagesDOCOMO Assignment Questions-1nitishhere100% (2)

- World Telecom Industry Is An Uprising Industry, Proceeding Towards A Goal of Achieving TwoDocument52 pagesWorld Telecom Industry Is An Uprising Industry, Proceeding Towards A Goal of Achieving Twomanwanimuki12No ratings yet

- Electronic: Components and Factors Responsible Behind The Growth of Telecommunications IndustryDocument4 pagesElectronic: Components and Factors Responsible Behind The Growth of Telecommunications IndustryMayank AgarwalNo ratings yet

- Telecom Industry in IndiaDocument21 pagesTelecom Industry in IndiaVaibhav PatelNo ratings yet

- The Industry Handbook - The Telecommunications Industry: Back To Industry ListDocument5 pagesThe Industry Handbook - The Telecommunications Industry: Back To Industry ListAnkush ThoratNo ratings yet

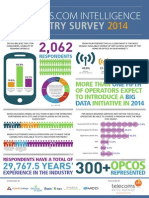

- Industry Survey: More Than of Operators Expect To Introduce A Initiative inDocument40 pagesIndustry Survey: More Than of Operators Expect To Introduce A Initiative intanveerameenNo ratings yet

- Data Analysis Cases With Real Data Case 3.1Document5 pagesData Analysis Cases With Real Data Case 3.1nikhiltiwari12389No ratings yet

- Assignment: Case Studies For Telecom Business FinanceDocument11 pagesAssignment: Case Studies For Telecom Business FinancesinghrachanabaghelNo ratings yet

- Coaxial Cable Market - North America Industry Analysis, Size, Share, Growth, Trends and Forecast, 2012 - 2018Document8 pagesCoaxial Cable Market - North America Industry Analysis, Size, Share, Growth, Trends and Forecast, 2012 - 2018api-247970851No ratings yet

- SM Assignment - e S JayaweeraDocument11 pagesSM Assignment - e S JayaweeraAnujanNo ratings yet

- Telecommunications Final PaperDocument41 pagesTelecommunications Final PaperJessieHaNo ratings yet

- Telecom Industry AnalysisDocument5 pagesTelecom Industry AnalysisSagar ThakurNo ratings yet

- Porter'S Five Forces Analysis of Indian Telecom Industry: I. Buyer PowerDocument6 pagesPorter'S Five Forces Analysis of Indian Telecom Industry: I. Buyer PowerRahul SinghNo ratings yet

- Handset Leasing - Unlock Opportunities To Regain Financial Position in Telecom IndustryDocument7 pagesHandset Leasing - Unlock Opportunities To Regain Financial Position in Telecom IndustryHoàng NguyễnNo ratings yet

- McKinsey Telecoms. RECALL No. 12, 2010 - The Fiber FutureDocument63 pagesMcKinsey Telecoms. RECALL No. 12, 2010 - The Fiber FuturekentselveNo ratings yet

- Topic of A ResearchDocument42 pagesTopic of A ResearchNhung DuckieNo ratings yet

- Current Trends in Indian Telecom: 1. New Players Entering Rural MarketsDocument7 pagesCurrent Trends in Indian Telecom: 1. New Players Entering Rural MarketsRishabh KantNo ratings yet

- Analysis of Vodafone Essar IndiaDocument34 pagesAnalysis of Vodafone Essar IndiaSantosh SamNo ratings yet

- AirtelDocument22 pagesAirtelAbhinav DaharwalNo ratings yet

- OECD Communications Outlook 2011: Summary in EnglishDocument5 pagesOECD Communications Outlook 2011: Summary in Englishuser2127No ratings yet

- E-Business Solutions For The Telecommunications Industry: January 2001Document16 pagesE-Business Solutions For The Telecommunications Industry: January 2001Fariha AzamNo ratings yet

- Exact Ventures NA Repair Market ReportDocument12 pagesExact Ventures NA Repair Market ReportCleyton Archbold BarkerNo ratings yet

- Euler's Method and Logistic Growth Solutions (BC Only) SolutionsDocument4 pagesEuler's Method and Logistic Growth Solutions (BC Only) SolutionsdeltabluerazeNo ratings yet

- Mobile Assisted Language Learning (MALL) Describes An Approach To Language LearningDocument7 pagesMobile Assisted Language Learning (MALL) Describes An Approach To Language Learninggusria ningsihNo ratings yet

- Dcof Full Notes (Module 2)Document9 pagesDcof Full Notes (Module 2)Minhaj KmNo ratings yet

- Total Result 194Document50 pagesTotal Result 194S TompulNo ratings yet

- MIS AssignmentDocument3 pagesMIS Assignmentsparepaper7455No ratings yet

- Full Download Ebook PDF Fundamentals of Modern Manufacturing Materials Processes and Systems 6th Edition PDFDocument42 pagesFull Download Ebook PDF Fundamentals of Modern Manufacturing Materials Processes and Systems 6th Edition PDFruth.white442100% (37)

- VSPlayer V7.2.0 - ENDocument27 pagesVSPlayer V7.2.0 - ENGiNo ratings yet

- 7 Maths NCERT Solutions Chapter 1 2 PDFDocument2 pages7 Maths NCERT Solutions Chapter 1 2 PDFAshwani K Sharma100% (1)

- 9.2.2.9 Lab - Configuring Multi-Area OSPFv3Document8 pages9.2.2.9 Lab - Configuring Multi-Area OSPFv3Jessica GregoryNo ratings yet

- MP Unit-3Document24 pagesMP Unit-3SARTHAK PANWARNo ratings yet

- Cost Benefit AnalysisDocument3 pagesCost Benefit AnalysisSaimo MghaseNo ratings yet

- HCD RG221Document64 pagesHCD RG221Berenice LopezNo ratings yet

- 6.6 MAC Address Table AttackDocument4 pages6.6 MAC Address Table AttackThoriq ThoriqNo ratings yet

- Clayoo User's GuideDocument200 pagesClayoo User's Guideronald patiño100% (1)

- Girbau, S.A.: STI-54 / STI-77 Parts ManualDocument72 pagesGirbau, S.A.: STI-54 / STI-77 Parts ManualoozbejNo ratings yet

- Pharma 4.0Document17 pagesPharma 4.0akhil pillai100% (1)

- 10 Challenges Facing Today's Applied Sport ScientistDocument7 pages10 Challenges Facing Today's Applied Sport ScientistDorian FigueroaNo ratings yet

- Block Diagram and Signal Flow GraphDocument15 pagesBlock Diagram and Signal Flow GraphAngelus Vincent GuilalasNo ratings yet

- FAA Safety Briefing Nov-Dec 2017 PDFDocument36 pagesFAA Safety Briefing Nov-Dec 2017 PDFAllison JacobsonNo ratings yet

- Enterprise Resourse Planning - Assessment-3Document8 pagesEnterprise Resourse Planning - Assessment-3Sha iyyaahNo ratings yet

- TFT Proview AY565 LCD Service MaunalDocument30 pagesTFT Proview AY565 LCD Service MaunalMarienka JankovaNo ratings yet

- Ransomware Ctep Situation Manual Ncep 072022 508 - 0Document30 pagesRansomware Ctep Situation Manual Ncep 072022 508 - 0piash007_571387617No ratings yet

- DSC-33C DSTC-40GDocument1 pageDSC-33C DSTC-40GsathishNo ratings yet

- 174872-Report On Voice Enabled Enterprise ChatbotDocument61 pages174872-Report On Voice Enabled Enterprise ChatbotBalaji GrandhiNo ratings yet

- Lab Manual 5Document6 pagesLab Manual 5Nasr UllahNo ratings yet

- Virtual Reality and Innovation PotentialDocument10 pagesVirtual Reality and Innovation PotentialUmerFarooqNo ratings yet

- ADPRO XO5.3.12 Security GuideDocument19 pagesADPRO XO5.3.12 Security Guidemichael.f.lamieNo ratings yet

- Guidely Age Set 1 PDFDocument5 pagesGuidely Age Set 1 PDFPriya KumariNo ratings yet

- Chapter 2 MeasurementsDocument50 pagesChapter 2 MeasurementsMehak SharmaNo ratings yet

- Linear Amps For Mobile OperationDocument10 pagesLinear Amps For Mobile OperationIan McNairNo ratings yet