You might also like

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- BWRR3123 AssignmentDocument55 pagesBWRR3123 AssignmentBaby KhorNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Chap10 Capital Budgeting TechniquesDocument54 pagesChap10 Capital Budgeting TechniquesBaby KhorNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- Chapter 4Document42 pagesChapter 4Baby KhorNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- International Codes of Corporate GovernanceDocument38 pagesInternational Codes of Corporate GovernanceBaby KhorNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Chap13 Leverage and Capital StructureDocument101 pagesChap13 Leverage and Capital StructureBaby KhorNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Estate Planning 3 PDFDocument2 pagesEstate Planning 3 PDFBaby KhorNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Chapter 1Document26 pagesChapter 1Baby KhorNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Chapter 5Document7 pagesChapter 5Baby KhorNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Case StudyDocument32 pagesCase StudyBaby Khor100% (1)

- Bwrr3103 - Estate PlanningDocument7 pagesBwrr3103 - Estate PlanningBaby KhorNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Chapter 1Document33 pagesChapter 1Baby Khor100% (1)

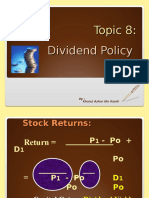

- Topic 8-Dividend PolicyDocument46 pagesTopic 8-Dividend PolicyBaby KhorNo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Chapter 2 LatestDocument24 pagesChapter 2 LatestBaby KhorNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Trust 2Document1 pageTrust 2Baby KhorNo ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- BWRR3103 EP SyllabusDocument7 pagesBWRR3103 EP SyllabusBaby KhorNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- BWRR3103 Case GuideDocument1 pageBWRR3103 Case GuideBaby KhorNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Topic 7 - Financial Leverage - Part 2Document35 pagesTopic 7 - Financial Leverage - Part 2Baby Khor100% (2)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- Topic 9 Tax AdministrationDocument31 pagesTopic 9 Tax AdministrationBaby KhorNo ratings yet

- Topic 7 - Financial Leverage - ExtraDocument57 pagesTopic 7 - Financial Leverage - ExtraBaby KhorNo ratings yet

- Topic 6-Cash Flow in Capital BudgetingDocument61 pagesTopic 6-Cash Flow in Capital BudgetingBaby KhorNo ratings yet

- Topic 3 - Stock ValuationDocument50 pagesTopic 3 - Stock ValuationBaby KhorNo ratings yet

- Topic 1 - TVMDocument61 pagesTopic 1 - TVMBaby KhorNo ratings yet

- Topic 7 - Financial Leverage - Part 1Document82 pagesTopic 7 - Financial Leverage - Part 1Baby KhorNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Topic 5 Capital Budgeting TechniqueDocument47 pagesTopic 5 Capital Budgeting TechniqueBaby KhorNo ratings yet

- Topic 4 Costofcapital NEW SLIDEDocument60 pagesTopic 4 Costofcapital NEW SLIDEBaby KhorNo ratings yet

- Chap8 Cost of CapitalDocument75 pagesChap8 Cost of CapitalBaby Khor50% (2)

- Topic 4 AdditionalDocument15 pagesTopic 4 AdditionalBaby KhorNo ratings yet

- Topic 2 - Bond Valuation-A132Document58 pagesTopic 2 - Bond Valuation-A132Baby KhorNo ratings yet

- Chap14 Dividend Payout PolicyDocument62 pagesChap14 Dividend Payout PolicyBaby KhorNo ratings yet

- CHAPTER 1-Bank ManagementDocument43 pagesCHAPTER 1-Bank ManagementBaby Khor90% (10)

- Jungreg CDocument7 pagesJungreg CStephen Lloyd GeronaNo ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- CIN - TAXINN Procedure - An Overview: Transaction Code: OBYZDocument8 pagesCIN - TAXINN Procedure - An Overview: Transaction Code: OBYZNeelesh KumarNo ratings yet

- Project ShaktiDocument2 pagesProject ShaktiMaitraya0% (1)

- Apple - Logo EvolutionDocument3 pagesApple - Logo EvolutionyuvashreeNo ratings yet

- Chapter - 06 Making Investment Decisions With The Net Present Value RuleDocument15 pagesChapter - 06 Making Investment Decisions With The Net Present Value RuleShaani KtkNo ratings yet

- Country Notebook Economic Analysis Resource GridDocument4 pagesCountry Notebook Economic Analysis Resource GridAmit GandhiNo ratings yet

- Hems For GarmentsDocument9 pagesHems For Garmentsvivek jangra100% (1)

- Executive SummaryDocument13 pagesExecutive SummaryKamlesh SoniwalNo ratings yet

- Income Declaration Scheme 2016 Critical AnalysisDocument6 pagesIncome Declaration Scheme 2016 Critical AnalysisTaxmann PublicationNo ratings yet

- Solutions For Economics Review QuestionsDocument28 pagesSolutions For Economics Review QuestionsDoris Acheng67% (3)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- PPC Tutorial 2 PDFDocument21 pagesPPC Tutorial 2 PDFkoriom@live.com.auNo ratings yet

- Classification of Economic EnvironmentDocument5 pagesClassification of Economic Environmentashish18518No ratings yet

- Buk 553100 BDocument7 pagesBuk 553100 BMario FloresNo ratings yet

- Capital Budgeting Study at Panasonic CarbonDocument8 pagesCapital Budgeting Study at Panasonic Carbone WAYNo ratings yet

- Karachi Head Office Membership ListDocument10 pagesKarachi Head Office Membership ListUsama KHan100% (1)

- OPOSing Telugu Curries PDFDocument2 pagesOPOSing Telugu Curries PDFpaadam68100% (2)

- IRCTC E-ticket from Kota Jn to BhagalpurDocument2 pagesIRCTC E-ticket from Kota Jn to BhagalpurAditya JhaNo ratings yet

- Engineering Steel - SBQ - Supply and Demand in EuropeDocument1 pageEngineering Steel - SBQ - Supply and Demand in EuropeAndrzej M KotasNo ratings yet

- Hotel ReportDocument6 pagesHotel ReportRamji SimhadriNo ratings yet

- Shampoo Project Implications Dec Can IntellectsDocument13 pagesShampoo Project Implications Dec Can IntellectsRakesh SainikNo ratings yet

- EconomicDocument6 pagesEconomicDaniloCardenasNo ratings yet

- Bhutans Gross National HappinessDocument4 pagesBhutans Gross National HappinessscrNo ratings yet

- Problem 3-2b SolutionDocument7 pagesProblem 3-2b SolutionAbdul Rasyid RomadhoniNo ratings yet

- Irf4104Gpbf: FeaturesDocument9 pagesIrf4104Gpbf: FeaturesAdam StevensonNo ratings yet

- Cse-Vi-management and Entrepreneurship (10al61) - Question PaperDocument3 pagesCse-Vi-management and Entrepreneurship (10al61) - Question PaperBMPNo ratings yet

- Swot Analysis of Indian Road NetworkDocument2 pagesSwot Analysis of Indian Road NetworkArpit Vaidya100% (1)

- PC3200 DDR II RAM (DDR-400) model size compatibility guideDocument7 pagesPC3200 DDR II RAM (DDR-400) model size compatibility guideEduard RubiaNo ratings yet

- Eu4 Loan-To-Build Profits CalculatorDocument8 pagesEu4 Loan-To-Build Profits CalculatorAnonymous pw0ajGNo ratings yet

- Drawstrings On Children's Upper Outerwear: Standard Safety Specification ForDocument2 pagesDrawstrings On Children's Upper Outerwear: Standard Safety Specification ForDoulat Ram100% (1)