You might also like

- Introduction To Valuation: The Time Value of MoneyDocument61 pagesIntroduction To Valuation: The Time Value of MoneyNimra RehmanNo ratings yet

- 5.1.2 Ordinary AnnuityDocument19 pages5.1.2 Ordinary AnnuityTin LauguicoNo ratings yet

- Interval ScaleDocument7 pagesInterval ScaleGilian PradoNo ratings yet

- RWJ Chapter 4 DCF ValuationDocument47 pagesRWJ Chapter 4 DCF ValuationAshekin MahadiNo ratings yet

- Compound InterestDocument10 pagesCompound InterestgetphotojobNo ratings yet

- RWJ Chapter 1 Introduction To Corporate FinanceDocument21 pagesRWJ Chapter 1 Introduction To Corporate FinanceAshekin Mahadi100% (1)

- Net Present ValueDocument8 pagesNet Present ValueDagnachew Amare DagnachewNo ratings yet

- Chapter 2 Time Value of MoneyDocument50 pagesChapter 2 Time Value of MoneyAMER KHALIQUENo ratings yet

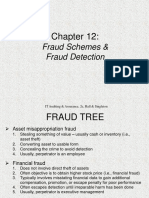

- Ch12 Fraud Scheme DetectionDocument18 pagesCh12 Fraud Scheme DetectionPanda BoarsNo ratings yet

- Derivative Calculator - With Steps!Document4 pagesDerivative Calculator - With Steps!emil wahyudiantoNo ratings yet

- CH 4Document23 pagesCH 4Gizaw BelayNo ratings yet

- Chapter 5Document21 pagesChapter 5MorerpNo ratings yet

- HR Om11 Modb GEDocument46 pagesHR Om11 Modb GESeng SoonNo ratings yet

- Chapter 04 Working Capital 1ce Lecture 050930Document71 pagesChapter 04 Working Capital 1ce Lecture 050930rthillai72No ratings yet

- EBIT-EPS analysis for financing plan decisionsDocument6 pagesEBIT-EPS analysis for financing plan decisionsSthephany GranadosNo ratings yet

- AccountDocument37 pagesAccountGaurang MakwanaNo ratings yet

- Bank Discount CalculationDocument3 pagesBank Discount CalculationPrakash ViswaNo ratings yet

- TVM Practice Problems SolutionsDocument3 pagesTVM Practice Problems SolutionsEmirī PhoonNo ratings yet

- Corporate Finance Chapter 9Document31 pagesCorporate Finance Chapter 9dia0% (2)

- Operators & Mathematical ExpressionDocument27 pagesOperators & Mathematical ExpressionForkensteinNo ratings yet

- 01 Accounting Study NotesDocument8 pages01 Accounting Study NotesJonas ScheckNo ratings yet

- Chapter 4 - Breach of Contract and TerminationDocument20 pagesChapter 4 - Breach of Contract and TerminationMacdonald PhashaNo ratings yet

- Time Value of MoneyDocument40 pagesTime Value of MoneyAhmedmughalNo ratings yet

- New Venture Finance Startup Funding For Entrepreneurs PDFDocument26 pagesNew Venture Finance Startup Funding For Entrepreneurs PDFBhagavan BangaloreNo ratings yet

- Notes On Financial AccountingDocument11 pagesNotes On Financial AccountingAbu ZakiNo ratings yet

- Data Collection MethodsDocument23 pagesData Collection MethodsZakir KhattakNo ratings yet

- Fallacies PDFDocument7 pagesFallacies PDFJazzverNo ratings yet

- Venn Diagrams-Final PDFDocument16 pagesVenn Diagrams-Final PDFsaraswatthiNo ratings yet

- Payout Policy: File, Then Send That File Back To Google Classwork - Assignment by Due Date & Due Time!Document4 pagesPayout Policy: File, Then Send That File Back To Google Classwork - Assignment by Due Date & Due Time!Gian RandangNo ratings yet

- Business Finance-Semi-Final ExamDocument3 pagesBusiness Finance-Semi-Final ExamHLeigh Nietes-Gabutan100% (1)

- Bond ValuationDocument50 pagesBond Valuationrenu3rdjanNo ratings yet

- Raising Capital MethodsDocument22 pagesRaising Capital MethodsSpidy BondNo ratings yet

- Corn Products Refining Company v. Commissioner of Internal Revenue, 215 F.2d 513, 2d Cir. (1954)Document7 pagesCorn Products Refining Company v. Commissioner of Internal Revenue, 215 F.2d 513, 2d Cir. (1954)Scribd Government DocsNo ratings yet

- Valuation and Rate of ReturnsDocument42 pagesValuation and Rate of ReturnsMadCube gamingNo ratings yet

- Accrual Accounting ProcessDocument52 pagesAccrual Accounting Processaamritaa100% (1)

- Time Value of Money-PowerpointDocument83 pagesTime Value of Money-Powerpointhaljordan313No ratings yet

- CHP 5Document72 pagesCHP 5Khaled A. M. El-sherifNo ratings yet

- Accounting Reports Tutorial NotesDocument21 pagesAccounting Reports Tutorial NotesSamiha RashidNo ratings yet

- The False DilemmaDocument7 pagesThe False DilemmaJessicaNo ratings yet

- Assignment I-Summers-Decision TheoryDocument2 pagesAssignment I-Summers-Decision TheorysaadNo ratings yet

- Unit 5 AP Macroeconomics Stabilization PoliciesDocument7 pagesUnit 5 AP Macroeconomics Stabilization PoliciesPinkyNo ratings yet

- Mathematics of InvestmentsDocument8 pagesMathematics of InvestmentsMathew EsparragoNo ratings yet

- Chapter 1Document213 pagesChapter 1Annur SofeaNo ratings yet

- C H A P T E R: Gross Income: ExclusionsDocument32 pagesC H A P T E R: Gross Income: Exclusionsdragon67No ratings yet

- Chap 10 IM Common Stock ValuationDocument97 pagesChap 10 IM Common Stock ValuationHaziq Shoaib MirNo ratings yet

- BEPP250 Final TestbankDocument189 pagesBEPP250 Final TestbankMichael Wen100% (2)

- CH12 Mish11 EMBFMDocument40 pagesCH12 Mish11 EMBFMBradley Ray100% (1)

- CH - 02 - Time Value of MoneyDocument38 pagesCH - 02 - Time Value of MoneyAlwin SebastianNo ratings yet

- Quantitative Problems Chapter 3Document5 pagesQuantitative Problems Chapter 3Shahzain RafiqNo ratings yet

- Chapter 0: Economics: The Core Issues: Multiple Choice QuestionsDocument107 pagesChapter 0: Economics: The Core Issues: Multiple Choice Questionsayoob naderNo ratings yet

- Compound Interest ProblemsDocument1 pageCompound Interest ProblemsLaSpina67% (3)

- Epler Consulting ServicesDocument3 pagesEpler Consulting ServicesAmmad Ud Din SabirNo ratings yet

- 03 LasherIM Ch03Document47 pages03 LasherIM Ch03Sana Khan100% (1)

- Chapter Three: Valuation of Financial Instruments & Cost of CapitalDocument68 pagesChapter Three: Valuation of Financial Instruments & Cost of CapitalAbrahamNo ratings yet

- Human Capital: Education and Health in Economic DevelopmentDocument33 pagesHuman Capital: Education and Health in Economic DevelopmentIvan PachecoNo ratings yet

- Chapter 6 Discounted Cash Flow ValuationDocument27 pagesChapter 6 Discounted Cash Flow ValuationAhmed Fathelbab100% (1)

- QUIZ-1 Monetary Theory and PolicyDocument1 pageQUIZ-1 Monetary Theory and PolicyAltaf HussainNo ratings yet

- Chap 12Document23 pagesChap 12MichelleLeeNo ratings yet

- Chapter 3_FIN3004_2024Document99 pagesChapter 3_FIN3004_2024luuthuydiem63No ratings yet

- Introduction To Valuation: The Time Value of MoneyDocument34 pagesIntroduction To Valuation: The Time Value of MoneyAlfina AfiiNo ratings yet

- Unilever Case StudyDocument5 pagesUnilever Case StudyHarshit MasterNo ratings yet

- Depb Scheme:: Imports Writing InstrumentsDocument6 pagesDepb Scheme:: Imports Writing InstrumentsHarshit MasterNo ratings yet

- MGMT 704 FALL 2015 Lecture Notes SEMINAR 4 - Level 5 Leadership - Article 3Document2 pagesMGMT 704 FALL 2015 Lecture Notes SEMINAR 4 - Level 5 Leadership - Article 3Harshit MasterNo ratings yet

- The HR Forecasting ProcessDocument15 pagesThe HR Forecasting ProcessHarshit MasterNo ratings yet

- IbmDocument35 pagesIbmCyril ChettiarNo ratings yet

- SM FinalDocument32 pagesSM FinalHarshit MasterNo ratings yet

- Vol 1 MGMT704 - Management and LeadershipDocument319 pagesVol 1 MGMT704 - Management and LeadershipHarshit Master100% (1)

- Manning ST13e Inppt03Document28 pagesManning ST13e Inppt03Harshit MasterNo ratings yet

- Manning ST13e Inppt01Document23 pagesManning ST13e Inppt01Muhammad Ahsan AkramNo ratings yet

- Implementation and Application of Logistics Information Systems in International Supply Chains - Challenges and Effectiveness GainsDocument19 pagesImplementation and Application of Logistics Information Systems in International Supply Chains - Challenges and Effectiveness GainsHarshit MasterNo ratings yet

- The Stock Market, The Theory of Rational Expectations, and The Efficient Market HypothesisDocument34 pagesThe Stock Market, The Theory of Rational Expectations, and The Efficient Market HypothesisHarshit MasterNo ratings yet

- Study on foreign entry alternativesDocument7 pagesStudy on foreign entry alternativesHarshit MasterNo ratings yet

- Bejing Chcago: AntwerpDocument3 pagesBejing Chcago: AntwerpHarshit MasterNo ratings yet

- How Management Accounting Information Supports Decision MakingDocument14 pagesHow Management Accounting Information Supports Decision MakingKad SaadNo ratings yet

- History: Jacob Davis Latvian JewishDocument2 pagesHistory: Jacob Davis Latvian JewishHarshit MasterNo ratings yet

- Export Assistances and IncentivesDocument15 pagesExport Assistances and IncentivesHarshit MasterNo ratings yet

- Attributes of Information: ExamplesDocument12 pagesAttributes of Information: ExamplesHarshit MasterNo ratings yet

- Salman MakdaDocument57 pagesSalman MakdaHarshit MasterNo ratings yet

- NaftaDocument8 pagesNaftaChitwan AchantaniNo ratings yet

- Export Assistances and IncentivesDocument15 pagesExport Assistances and IncentivesHarshit MasterNo ratings yet

- Export Assistance and IncentivesDocument8 pagesExport Assistance and IncentivesHarshit MasterNo ratings yet

- Economics 54tarting PagesDocument8 pagesEconomics 54tarting PagesHarshit MasterNo ratings yet

- Indian Management Thoughts and PracticesDocument14 pagesIndian Management Thoughts and PracticesHarshit MasterNo ratings yet

- Raghuram Rajan's Strong Starting Speech as RBI GovernorDocument3 pagesRaghuram Rajan's Strong Starting Speech as RBI GovernorHarshit MasterNo ratings yet

- July12 4 PDFDocument8 pagesJuly12 4 PDFInma Vidal GrimaltosNo ratings yet

- IEPR493SRR0913Document7 pagesIEPR493SRR0913Harshit MasterNo ratings yet

- Chap007 NewDocument46 pagesChap007 NewHarshit MasterNo ratings yet

- (U - Y Ux1 Esi) JADocument7 pages(U - Y Ux1 Esi) JAMustafa HusseinNo ratings yet

- New HRMDocument45 pagesNew HRMHarshit MasterNo ratings yet

- Compilation of CasesDocument121 pagesCompilation of CasesMabelle ArellanoNo ratings yet

- Eritrea and Ethiopia Beyond The Impasse PDFDocument12 pagesEritrea and Ethiopia Beyond The Impasse PDFThe Ethiopian AffairNo ratings yet

- Flare Finance Ecosystem MapDocument1 pageFlare Finance Ecosystem MapEssence of ChaNo ratings yet

- MiniQAR MK IIDocument4 pagesMiniQAR MK IIChristina Gray0% (1)

- Emperger's pioneering composite columnsDocument11 pagesEmperger's pioneering composite columnsDishant PrajapatiNo ratings yet

- Understanding CTS Log MessagesDocument63 pagesUnderstanding CTS Log MessagesStudentNo ratings yet

- Introduction To Succession-1Document8 pagesIntroduction To Succession-1amun dinNo ratings yet

- MSBI Installation GuideDocument25 pagesMSBI Installation GuideAmit SharmaNo ratings yet

- SAP ORC Opportunities PDFDocument1 pageSAP ORC Opportunities PDFdevil_3565No ratings yet

- Tech Letter-NFPA 54 To Include Bonding 8-08Document2 pagesTech Letter-NFPA 54 To Include Bonding 8-08gl lugaNo ratings yet

- BA 9000 - NIJ CTP Body Armor Quality Management System RequirementsDocument6 pagesBA 9000 - NIJ CTP Body Armor Quality Management System RequirementsAlberto GarciaNo ratings yet

- Ralf Behrens: About The ArtistDocument3 pagesRalf Behrens: About The ArtistStavros DemosthenousNo ratings yet

- Alfa Laval Complete Fittings CatalogDocument224 pagesAlfa Laval Complete Fittings CatalogGraciele SoaresNo ratings yet

- Ieee Research Papers On Software Testing PDFDocument5 pagesIeee Research Papers On Software Testing PDFfvgjcq6a100% (1)

- Aci 207.1Document38 pagesAci 207.1safak kahraman100% (7)

- John GokongweiDocument14 pagesJohn GokongweiBela CraigNo ratings yet

- Chapter 2a Non Structured DataRozianiwatiDocument43 pagesChapter 2a Non Structured DataRozianiwatiNur AnisaNo ratings yet

- Deed of Sale - Motor VehicleDocument4 pagesDeed of Sale - Motor Vehiclekyle domingoNo ratings yet

- UW Computational-Finance & Risk Management Brochure Final 080613Document2 pagesUW Computational-Finance & Risk Management Brochure Final 080613Rajel MokNo ratings yet

- Theme Meal ReportDocument10 pagesTheme Meal Reportapi-434982019No ratings yet

- EFM2e, CH 03, SlidesDocument36 pagesEFM2e, CH 03, SlidesEricLiangtoNo ratings yet

- Engine Controls (Powertrain Management) - ALLDATA RepairDocument4 pagesEngine Controls (Powertrain Management) - ALLDATA Repairmemo velascoNo ratings yet

- Account STMT XX0226 19122023Document13 pagesAccount STMT XX0226 19122023rdineshyNo ratings yet

- Developing a Positive HR ClimateDocument15 pagesDeveloping a Positive HR ClimateDrPurnima SharmaNo ratings yet

- CSEC IT Fundamentals of Hardware and SoftwareDocument2 pagesCSEC IT Fundamentals of Hardware and SoftwareR.D. Khan100% (1)

- Bentone 30 Msds (Eu-Be)Document6 pagesBentone 30 Msds (Eu-Be)Amir Ososs0% (1)

- Applicants at Huye Campus SiteDocument4 pagesApplicants at Huye Campus SiteHIRWA Cyuzuzo CedricNo ratings yet

- ABS Rules for Steel Vessels Under 90mDocument91 pagesABS Rules for Steel Vessels Under 90mGean Antonny Gamarra DamianNo ratings yet

- SD Electrolux LT 4 Partisi 21082023Document3 pagesSD Electrolux LT 4 Partisi 21082023hanifahNo ratings yet

- Material Properties L2 Slides and NotesDocument41 pagesMaterial Properties L2 Slides and NotesjohnNo ratings yet