You might also like

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- MoM Internship Briefing 2016Document2 pagesMoM Internship Briefing 2016Dicky Leonardo LoisNo ratings yet

- Audit Project 3Document3 pagesAudit Project 3Dicky Leonardo LoisNo ratings yet

- Audit Project 3Document3 pagesAudit Project 3Dicky Leonardo LoisNo ratings yet

- Major Association of Accounting President UniversityDocument1 pageMajor Association of Accounting President UniversityDicky Leonardo LoisNo ratings yet

- Pak Frans Most Updated Resume - FinalDocument7 pagesPak Frans Most Updated Resume - FinalDicky Leonardo LoisNo ratings yet

- Financial RatioDocument25 pagesFinancial RatioDicky Leonardo LoisNo ratings yet

- AJAX Corp SolutionDocument2 pagesAJAX Corp SolutionDicky Leonardo LoisNo ratings yet

- Active 2016 Invitation Letter LecturerDocument2 pagesActive 2016 Invitation Letter LecturerDicky Leonardo LoisNo ratings yet

- Asis Untuk BADocument3 pagesAsis Untuk BADicky Leonardo LoisNo ratings yet

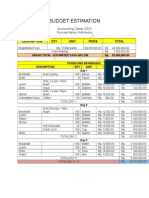

- Budget Estimation: Description QTY Unit Price TotalDocument4 pagesBudget Estimation: Description QTY Unit Price TotalDicky Leonardo LoisNo ratings yet

- LPJ KPMG 4seas ScholarshipDocument13 pagesLPJ KPMG 4seas ScholarshipDicky Leonardo LoisNo ratings yet

- CV BrohDocument2 pagesCV BrohDicky Leonardo LoisNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- 4b Notes PDFDocument9 pages4b Notes PDFIrriz MadriagaNo ratings yet

- REVISED FINAMA Reviewer With AnswersDocument25 pagesREVISED FINAMA Reviewer With AnswersYander Marl Bautista100% (1)

- Eli Lilly in IndiaDocument9 pagesEli Lilly in IndiaAnonymous 3XQl6TL100% (1)

- Eco Com 1 AnantDocument5 pagesEco Com 1 AnantAnant JainNo ratings yet

- Airbus Student-08Document20 pagesAirbus Student-08NicolasKollerNo ratings yet

- Managerial Accounting - Assignment (1) - Model AnswerDocument3 pagesManagerial Accounting - Assignment (1) - Model AnswerHaytham NasefNo ratings yet

- Understanding Financial Highlights in The Financial Statements of Hedge FundsDocument3 pagesUnderstanding Financial Highlights in The Financial Statements of Hedge Fundssoumyac100% (1)

- Macroeconomics - Staicu&PopescuDocument155 pagesMacroeconomics - Staicu&PopescuŞtefania Alice100% (1)

- Farm Laws Detailed Analysis-StudyDocument5 pagesFarm Laws Detailed Analysis-StudyRakeshKulkarniNo ratings yet

- Fertilizer Market ReportDocument72 pagesFertilizer Market ReportLe Anh DangNo ratings yet

- Fixed Income Portfolio Performance AttributionDocument38 pagesFixed Income Portfolio Performance Attributionvipinkumar96No ratings yet

- Research Report On Strategies of Amul and SarasDocument84 pagesResearch Report On Strategies of Amul and Sarasswatigupta8880% (5)

- Econ Exam Vault (UCSD)Document85 pagesEcon Exam Vault (UCSD)CameronNo ratings yet

- Business Plan TemplateDocument12 pagesBusiness Plan TemplateJomel BriosoNo ratings yet

- Mac TilesDocument24 pagesMac TilesNuwani Manasinghe100% (1)

- Formation of ContractDocument15 pagesFormation of ContractVi Pin SinghNo ratings yet

- Microeconomics 4th Edition Hubbard Test BankDocument65 pagesMicroeconomics 4th Edition Hubbard Test Bankpearlgregoryspx100% (30)

- Nonprofit Management: Chapter 10: Marketing and CommunicationsDocument12 pagesNonprofit Management: Chapter 10: Marketing and Communicationssam lissenNo ratings yet

- Cost CurvesDocument35 pagesCost Curvessinghanshu21100% (2)

- Chapter 14Document38 pagesChapter 14Mahedi Hasan RabbiNo ratings yet

- Direct and Indirect TaxDocument3 pagesDirect and Indirect TaxKb AliNo ratings yet

- EIL EnquiryDocument321 pagesEIL EnquiryyogitatanavadeNo ratings yet

- Valuation of Aggregate Operations For Banking PurposesDocument18 pagesValuation of Aggregate Operations For Banking PurposesRodrigo DavidNo ratings yet

- Trading The Forex Market: by Vince StanzioneDocument51 pagesTrading The Forex Market: by Vince StanzioneTiavina Rakotomalala43% (7)

- Gnosis WhitepaperDocument30 pagesGnosis WhitepaperСергей БуркатовскийNo ratings yet

- Quiz Internal AccountingDocument3 pagesQuiz Internal AccountingMili Dit100% (1)

- Not ADocument4 pagesNot AKasia PilecwzNo ratings yet

- PAS 2 Inventories MeasurementDocument6 pagesPAS 2 Inventories Measurementcamille joi florendoNo ratings yet

- Effectiveness of Customer Relationship Management at Airtel: A Project ReportDocument79 pagesEffectiveness of Customer Relationship Management at Airtel: A Project ReportvipultandonddnNo ratings yet

- 3 PLDocument6 pages3 PLAbhishek7705No ratings yet