You might also like

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- Manajemen Keuangan - 20 Nov 2021 - BDocument24 pagesManajemen Keuangan - 20 Nov 2021 - Bmuhammad nurNo ratings yet

- Capital Structure Extra NotesDocument29 pagesCapital Structure Extra NotesleighannNo ratings yet

- Get Rich with Dividends: A Proven System for Earning Double-Digit ReturnsFrom EverandGet Rich with Dividends: A Proven System for Earning Double-Digit ReturnsNo ratings yet

- Capital Structure: Basic ConceptsDocument34 pagesCapital Structure: Basic ConceptsNitish BudhirajaNo ratings yet

- CF - Chapter 16 - Capital StructureDocument25 pagesCF - Chapter 16 - Capital StructureS A M ANo ratings yet

- Capital Structure - Basic ConceptsDocument10 pagesCapital Structure - Basic ConceptsDUY LE NHAT TRUONGNo ratings yet

- LN Capstru1Document63 pagesLN Capstru1pgdm23samamalNo ratings yet

- 041924353041-Review Chapter 16Document3 pages041924353041-Review Chapter 16Aimé RandrianantenainaNo ratings yet

- C09 +chap+16 +Capital+Structure+-+Basic+ConceptsDocument24 pagesC09 +chap+16 +Capital+Structure+-+Basic+Conceptsstanley tsangNo ratings yet

- Session 12. Capital Structure Decisions Part IDocument21 pagesSession 12. Capital Structure Decisions Part IKAVYA GOYAL PGP 2021-23 BatchNo ratings yet

- Fundamentals of Capital StructureDocument42 pagesFundamentals of Capital StructureSona Singh pgpmx 2017 batch-2No ratings yet

- CF - Chapter 16Document25 pagesCF - Chapter 16Quân LêNo ratings yet

- Capital Structure IDocument23 pagesCapital Structure IhatemNo ratings yet

- Capital Structure: Basic Concepts: Mcgraw-Hill/IrwinDocument25 pagesCapital Structure: Basic Concepts: Mcgraw-Hill/IrwinBennyKurniawanNo ratings yet

- Capital Structure: Basic Concepts: No TaxesDocument27 pagesCapital Structure: Basic Concepts: No TaxesamsaNo ratings yet

- Chap 016Document25 pagesChap 016Utkarsh GoelNo ratings yet

- Capital Structure Basic ConceptsDocument25 pagesCapital Structure Basic ConceptsisratzamananuNo ratings yet

- Optimal Capital Structure Is The Mix of Debt and Equity ThatDocument29 pagesOptimal Capital Structure Is The Mix of Debt and Equity ThatdevashneeNo ratings yet

- Capital Structure: Basic ConceptsDocument25 pagesCapital Structure: Basic ConceptsThuyDuongNo ratings yet

- Corporate Financing Decision (FIN 502) MBA Kathmandu University School of ManagementDocument20 pagesCorporate Financing Decision (FIN 502) MBA Kathmandu University School of ManagementShreeya SigdelNo ratings yet

- Capital StructureDocument21 pagesCapital StructureRameen Jawad MalikNo ratings yet

- 3.0 Capital StructureDocument10 pages3.0 Capital StructureHashashahNo ratings yet

- Optimal Financing MixDocument4 pagesOptimal Financing MixSana SarfarazNo ratings yet

- Capital Structure - 1Document6 pagesCapital Structure - 1nithyasree1994No ratings yet

- Chap 014Document25 pagesChap 014Rizal YusanNo ratings yet

- Finance For Executives Managing For Value Creation 5Th Edition Hawawini Solutions Manual Full Chapter PDFDocument14 pagesFinance For Executives Managing For Value Creation 5Th Edition Hawawini Solutions Manual Full Chapter PDFheulwenvalerie7dr100% (10)

- Mcgraw-Hill/Irwin Corporate Finance, 7/E: © 2005 The Mcgraw-Hill Companies, Inc. All Rights ReservedDocument26 pagesMcgraw-Hill/Irwin Corporate Finance, 7/E: © 2005 The Mcgraw-Hill Companies, Inc. All Rights ReservedMohammad Ilham FawwazNo ratings yet

- What Is Leveraged Buyout Model Aka LBO Model?Document5 pagesWhat Is Leveraged Buyout Model Aka LBO Model?bhumiklalka999No ratings yet

- CF 11th Edition Chapter 16 Excel Master StudentDocument15 pagesCF 11th Edition Chapter 16 Excel Master StudentEstefanīa GalarzaNo ratings yet

- MBS Corporate Finance 2023 Slide Set 4Document112 pagesMBS Corporate Finance 2023 Slide Set 4PGNo ratings yet

- Debt and Policy Value CaseDocument6 pagesDebt and Policy Value CaseUche Mba100% (2)

- Lecture 16 - Capital Structure - Basic ConceptsDocument15 pagesLecture 16 - Capital Structure - Basic ConceptsNhân TrịnhNo ratings yet

- Capital Structure: Rakesh ArrawatiaDocument38 pagesCapital Structure: Rakesh ArrawatiashravaniNo ratings yet

- Campus Deli Case 4Document15 pagesCampus Deli Case 4Ash RamirezNo ratings yet

- Case Study 2Document5 pagesCase Study 2Tabish Iftikhar SyedNo ratings yet

- Capital Structure: Basic ConceptsDocument27 pagesCapital Structure: Basic ConceptsRemonNo ratings yet

- Capital Structure: Basic ConceptsDocument27 pagesCapital Structure: Basic ConceptsArjun SharmaNo ratings yet

- Chapter 16 Tcdn GốcDocument37 pagesChapter 16 Tcdn GốcN KhNo ratings yet

- Managerial Finance AssignmentDocument5 pagesManagerial Finance AssignmentvinneNo ratings yet

- FIN 500 Extra Problems Fall 20-21Document4 pagesFIN 500 Extra Problems Fall 20-21saraNo ratings yet

- Introduction To Debt PolicyDocument8 pagesIntroduction To Debt PolicyRatnesh DubeyNo ratings yet

- 02 CapStr Basic NiuDocument28 pages02 CapStr Basic NiuLombeNo ratings yet

- Financing Decisions 10-12Document48 pagesFinancing Decisions 10-12Rajat ShrinetNo ratings yet

- Capital Structure - Sep 2021Document52 pagesCapital Structure - Sep 2021BHAVYA KANDPAL 13BCE0206No ratings yet

- Cffinals PDFDocument82 pagesCffinals PDFsultaniiuNo ratings yet

- Problem Set 5: Capital StructureDocument3 pagesProblem Set 5: Capital StructureGautam PatilNo ratings yet

- Capital Structure DecisionDocument26 pagesCapital Structure DecisionNet BeeNo ratings yet

- Quiz 6 NotesDocument14 pagesQuiz 6 NotesEmily SNo ratings yet

- Chapter 4: Analysis of Financial StatementsDocument8 pagesChapter 4: Analysis of Financial StatementsSafuan HalimNo ratings yet

- Leverage: Definition 1Document11 pagesLeverage: Definition 1diptishahNo ratings yet

- Topic 8Document7 pagesTopic 8黄芷琦No ratings yet

- Case 26 An Introduction To Debt Policy ADocument5 pagesCase 26 An Introduction To Debt Policy Amy VinayNo ratings yet

- IB - Lecture 9Document55 pagesIB - Lecture 9Phan ChiNo ratings yet

- Ross Corporate 13e PPT CH16 AccessibleDocument26 pagesRoss Corporate 13e PPT CH16 Accessiblemaigiangngoc2004No ratings yet

- LeveragesDocument50 pagesLeveragesPrem KishanNo ratings yet

- Capital StructureDocument27 pagesCapital Structuresiddharth agrawalNo ratings yet

- Cap StrucDocument58 pagesCap StrucTanyaNo ratings yet

- 3rd Presentation 2020Document51 pages3rd Presentation 2020Camila Arango PérezNo ratings yet

- The McDozer Blogs - Public Journal of A DropoutDocument254 pagesThe McDozer Blogs - Public Journal of A DropoutmcdozerNo ratings yet

- Home Loans V1Document38 pagesHome Loans V1katari vajrakuntNo ratings yet

- Finance - Function Matters, Not SizeDocument25 pagesFinance - Function Matters, Not SizeVicente MirandaNo ratings yet

- The Structure of Financial System of BangladeshDocument8 pagesThe Structure of Financial System of Bangladeshmoaz_tareq1622No ratings yet

- S F S P: The Pecial Actor Taking LanDocument7 pagesS F S P: The Pecial Actor Taking LanMG7FILMESNo ratings yet

- NEGO 103 Case DigestsDocument34 pagesNEGO 103 Case DigestskbongcoNo ratings yet

- Project Report On Birla Sunlife Mutual FundDocument46 pagesProject Report On Birla Sunlife Mutual FundSandeepSingh83% (6)

- Fairstone Terms and Conditions PDFDocument10 pagesFairstone Terms and Conditions PDFGarrett GilesNo ratings yet

- Lesson #1 FabmDocument32 pagesLesson #1 FabmCZARINA ROSEANNE M. GIMENEZNo ratings yet

- The Internet of Money Volume Three A Collection of Talks by AndreasDocument198 pagesThe Internet of Money Volume Three A Collection of Talks by AndreasawenNo ratings yet

- ECON 302 Lecture 1Document29 pagesECON 302 Lecture 1Jasmine Yang100% (1)

- Debt Collection Article PDFDocument38 pagesDebt Collection Article PDFAlexandria BurrisNo ratings yet

- Admission of A Partner PDFDocument8 pagesAdmission of A Partner PDFSpandan DasNo ratings yet

- PubFin Module 1 Chpater 1 Overview of Public Fiscal Administration (Old Module)Document63 pagesPubFin Module 1 Chpater 1 Overview of Public Fiscal Administration (Old Module)Christoper TaranNo ratings yet

- The Fed's Dual Mandate Responsibilities and Challenges Facing U.S. Monetary Policy - Federal Reserve Bank of ChicagoDocument5 pagesThe Fed's Dual Mandate Responsibilities and Challenges Facing U.S. Monetary Policy - Federal Reserve Bank of ChicagoAlvaroNo ratings yet

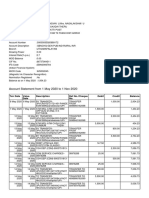

- Account Statement From 1 May 2020 To 1 Nov 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument9 pagesAccount Statement From 1 May 2020 To 1 Nov 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceChellapandiNo ratings yet

- Tax PaidDocument1 pageTax PaidRiya Mazumder Roll 286No ratings yet

- Group AssignmentDocument5 pagesGroup AssignmentDuc Thien LuongNo ratings yet

- You Are Never Too Young or Old To Start InvestingDocument40 pagesYou Are Never Too Young or Old To Start InvestingMaxNo ratings yet

- Errata Sheet Financial DerivativesDocument2 pagesErrata Sheet Financial DerivativesmasniahmakmurNo ratings yet

- Investment Operation of Islami BankDocument34 pagesInvestment Operation of Islami Bankmd.jewel ranaNo ratings yet

- SIP 2023 Project Akshay Dakhale 20233Document48 pagesSIP 2023 Project Akshay Dakhale 20233Aniket KambleNo ratings yet

- Ac101 ch7Document15 pagesAc101 ch7infinite_dreamsNo ratings yet

- Tan Yee Ling 2RFI12Document33 pagesTan Yee Ling 2RFI12MIN ZHE ONGNo ratings yet

- Inflation DissertationDocument59 pagesInflation Dissertationbaguma100% (1)

- Contoh Soal SAP 010 - Financial Accounting (Batch 1&2)Document19 pagesContoh Soal SAP 010 - Financial Accounting (Batch 1&2)Jhoni100% (3)

- Proyeksi Target 2019Document10 pagesProyeksi Target 2019Duky FirmansyahNo ratings yet

- MK84F763C3ID49548209 BorrowerDocument17 pagesMK84F763C3ID49548209 BorrowerMita BanerjeeNo ratings yet

- Valuation of Securities-3Document54 pagesValuation of Securities-3anupan92No ratings yet

- Honor Mobile Flyer 3419Document2 pagesHonor Mobile Flyer 3419bilal asifNo ratings yet