You might also like

- Responsibility CenterDocument32 pagesResponsibility CenterNeneng WulandariNo ratings yet

- Chapter 1 Lecture - WulanDocument16 pagesChapter 1 Lecture - WulanNeneng WulandariNo ratings yet

- Stocks and Their Valuation: Taufikur@ugm - Ac.idDocument43 pagesStocks and Their Valuation: Taufikur@ugm - Ac.idNeneng Wulandari100% (1)

- AML Sesi 6Document3 pagesAML Sesi 6Neneng WulandariNo ratings yet

- Mergers and Acquisitions: Rights Reserved. Mcgraw-Hill/IrwinDocument23 pagesMergers and Acquisitions: Rights Reserved. Mcgraw-Hill/Irwinkkn35No ratings yet

- The Cost of Capital: Taufikur@ugm - Ac.idDocument31 pagesThe Cost of Capital: Taufikur@ugm - Ac.idNeneng WulandariNo ratings yet

- Options and Corporate Finance: Basic ConceptsDocument68 pagesOptions and Corporate Finance: Basic ConceptsNeneng WulandariNo ratings yet

- Strengthening A Company'S Competitive Position: Strategic Moves, Timing, and Scope of OperationsDocument16 pagesStrengthening A Company'S Competitive Position: Strategic Moves, Timing, and Scope of OperationsNeneng WulandariNo ratings yet

- Determining and Forecasting Exchange Rates: Factors, Systems, and FX Market PlayersDocument4 pagesDetermining and Forecasting Exchange Rates: Factors, Systems, and FX Market PlayersNeneng WulandariNo ratings yet

- Key Features and Valuation of BondsDocument40 pagesKey Features and Valuation of BondsNeneng WulandariNo ratings yet

- Strategies For Competing in International Markets: Student VersionDocument15 pagesStrategies For Competing in International Markets: Student VersionNeneng WulandariNo ratings yet

- Types of Forex Exposure and Transaction Risk ManagementDocument13 pagesTypes of Forex Exposure and Transaction Risk ManagementNeneng WulandariNo ratings yet

- Types of Forex Exposure and Transaction Risk ManagementDocument13 pagesTypes of Forex Exposure and Transaction Risk ManagementNeneng WulandariNo ratings yet

- Book 1 BelajarDocument1 pageBook 1 BelajarNeneng WulandariNo ratings yet

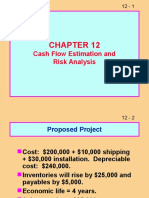

- CH 12 Cash Flow Estimatision and Risk AnalysisDocument39 pagesCH 12 Cash Flow Estimatision and Risk AnalysisNeneng WulandariNo ratings yet

- Audit PrinciplesDocument34 pagesAudit PrinciplesJhayanti Nithyananda KalyaniNo ratings yet

- 1 Effect of Governance On Credit DecitionsDocument21 pages1 Effect of Governance On Credit DecitionsANISANo ratings yet

- Management Accounting: Student EditionDocument24 pagesManagement Accounting: Student EditionNeneng WulandariNo ratings yet

- Management Accounting: Student EditionDocument28 pagesManagement Accounting: Student EditionNeneng WulandariNo ratings yet

- MAHM8e Chapter03.Ab - AzDocument27 pagesMAHM8e Chapter03.Ab - AzDinda OktavianiNo ratings yet

- Management Accounting: Student EditionDocument27 pagesManagement Accounting: Student EditionNeneng WulandariNo ratings yet

- HTTP Tugas EnronDocument1 pageHTTP Tugas EnronNeneng WulandariNo ratings yet

- Responsibility Centers: Types, Performance Measurement and Transfer PricingDocument32 pagesResponsibility Centers: Types, Performance Measurement and Transfer PricingNeneng WulandariNo ratings yet

- Managerial Accounting: Student EditionDocument21 pagesManagerial Accounting: Student EditionNeneng WulandariNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Drafting, Stamping and Registration of DocumentsDocument94 pagesDrafting, Stamping and Registration of DocumentsAmit ThokeNo ratings yet

- Security Bank's History and LeadershipDocument6 pagesSecurity Bank's History and LeadershipKathlyn Cher SarmientoNo ratings yet

- Proffesional Option TraderDocument15 pagesProffesional Option TraderNehang PandyaNo ratings yet

- Cases on SEBI regulations and insider tradingDocument29 pagesCases on SEBI regulations and insider tradingmhatresanjeevNo ratings yet

- Gail B. Warden, in Her Capacity as Trustee of the Trust Established Under Deed of Charles Graham Berwind, Dated February 28, 1963, for the Benefit of David McMichael Berwind, and Derivatively on Behalf of Berwind Pharmaceutical Services, Inc. Linda B. Shappy, in Her Capacity as Trustee of the Trust Established Under Deed of Charles Graham Berwind, Dated February 28, 1963, for the Benefit of David McMichael Berwind, and Derivatively on Behalf of Berwind Pharmaceutical Services, Inc. David McMichael Berwind, Jr., in His Capacity as Trustee of the Trust Established Under Deed of Charles Graham Berwind, Dated February 28, 1963, for the Benefit of David McMichael Berwind, and Derivatively on Behalf of Berwind Pharmaceutical Services, Inc. David McMichael Berwind, in His Capacity as Trustee of the Trust Established Under Deed of Charles Graham Berwind, Dated February 28, 1963, for the Benefit of David McMichael Berwind, and Derivatively on Behalf of Berwind Pharmaceutical Services, Inc. v. MDocument14 pagesGail B. Warden, in Her Capacity as Trustee of the Trust Established Under Deed of Charles Graham Berwind, Dated February 28, 1963, for the Benefit of David McMichael Berwind, and Derivatively on Behalf of Berwind Pharmaceutical Services, Inc. Linda B. Shappy, in Her Capacity as Trustee of the Trust Established Under Deed of Charles Graham Berwind, Dated February 28, 1963, for the Benefit of David McMichael Berwind, and Derivatively on Behalf of Berwind Pharmaceutical Services, Inc. David McMichael Berwind, Jr., in His Capacity as Trustee of the Trust Established Under Deed of Charles Graham Berwind, Dated February 28, 1963, for the Benefit of David McMichael Berwind, and Derivatively on Behalf of Berwind Pharmaceutical Services, Inc. David McMichael Berwind, in His Capacity as Trustee of the Trust Established Under Deed of Charles Graham Berwind, Dated February 28, 1963, for the Benefit of David McMichael Berwind, and Derivatively on Behalf of Berwind Pharmaceutical Services, Inc. v. MScribd Government DocsNo ratings yet

- Semi Detailed Lesson Plan in Epp VLDocument5 pagesSemi Detailed Lesson Plan in Epp VLMei Bhern Garo67% (3)

- Cgr660 10 LiquidationDocument39 pagesCgr660 10 Liquidationr4vemasterNo ratings yet

- ATC List 2020 Updated 25620 PDFDocument54 pagesATC List 2020 Updated 25620 PDFPeper12345No ratings yet

- Key Feature Document: You Have Chosen Second Income Option Maturity Benefit: Death Benefit: Income BenefitDocument3 pagesKey Feature Document: You Have Chosen Second Income Option Maturity Benefit: Death Benefit: Income BenefitSantosh Kumar RoyNo ratings yet

- Legal FrameworkDocument48 pagesLegal FrameworkRK DeshmukhNo ratings yet

- Sec 35-37 Powers of CorporationDocument10 pagesSec 35-37 Powers of CorporationJoana Trinidad100% (1)

- Schedule For Analyst Inst MeetDocument20 pagesSchedule For Analyst Inst MeetNeerav Indrajit GadhviNo ratings yet

- Local Business Partner in UAEDocument1 pageLocal Business Partner in UAEDevar AENo ratings yet

- Limited Liability With One-Man Companies and Subsidiary Corporati PDFDocument32 pagesLimited Liability With One-Man Companies and Subsidiary Corporati PDFansanjunelynNo ratings yet

- Co Operative BankingDocument11 pagesCo Operative BankingMahesh VermaNo ratings yet

- Background of Company LawDocument30 pagesBackground of Company LawsidaneyNo ratings yet

- Financial Accounting (Assignment)Document7 pagesFinancial Accounting (Assignment)Bella SeahNo ratings yet

- Business Law Agency NotesDocument16 pagesBusiness Law Agency NotesKingpinsNo ratings yet

- Financial Derivatives ExplainedDocument8 pagesFinancial Derivatives ExplainedAmit babarNo ratings yet

- 2012 Corporate InsolvencyDocument96 pages2012 Corporate Insolvencygreenemerald36No ratings yet

- Resume Swap Markets 15-1 Background: 15-1a Use of Swaps For HedgingDocument9 pagesResume Swap Markets 15-1 Background: 15-1a Use of Swaps For HedgingAbdul Aziz FaqihNo ratings yet

- 1113 Form1LLPDocument4 pages1113 Form1LLPJothiChidanandNo ratings yet

- LWR Wordings Issued 2021 - at 28 February 2021Document3 pagesLWR Wordings Issued 2021 - at 28 February 2021Farrukh KhanNo ratings yet

- Sekuritas Hibrida: Utang Konvertibel: Convertible DebtDocument10 pagesSekuritas Hibrida: Utang Konvertibel: Convertible DebtErna hkNo ratings yet

- ch16 Dilutive Securities - Amp - EPS OLDDocument120 pagesch16 Dilutive Securities - Amp - EPS OLDnandidhiya100% (1)

- Book Value Per Share Basic Earnings PerDocument61 pagesBook Value Per Share Basic Earnings Perayagomez100% (1)

- Top 40 Wealth Management Firms 2017Document3 pagesTop 40 Wealth Management Firms 2017JonNo ratings yet

- Health Insurance Receipt 2022Document1 pageHealth Insurance Receipt 2022Vijay SekarNo ratings yet

- A Guide To Deposit InsuranceDocument7 pagesA Guide To Deposit InsuranceSubrahmanyam PvNo ratings yet

- Company LawDocument19 pagesCompany LawAakankshaNo ratings yet