You might also like

- Financial Markets: Lectures 3 - 4Document48 pagesFinancial Markets: Lectures 3 - 4Lê Mai Huyền LinhNo ratings yet

- Chapter 13-Equity Financing: Multiple ChoiceDocument43 pagesChapter 13-Equity Financing: Multiple ChoiceLouise100% (2)

- Financial Markets Fundamentals: Why, how and what Products are traded on Financial Markets. Understand the Emotions that drive TradingFrom EverandFinancial Markets Fundamentals: Why, how and what Products are traded on Financial Markets. Understand the Emotions that drive TradingNo ratings yet

- JPMQ: Pairs Trade Model: Pair Trade Close Alert (AGN US / BMY US)Document6 pagesJPMQ: Pairs Trade Model: Pair Trade Close Alert (AGN US / BMY US)smysonaNo ratings yet

- IBM IIW OverviewDocument36 pagesIBM IIW Overviewd_sengNo ratings yet

- The Financial SystemDocument82 pagesThe Financial SystemGaurav007100% (1)

- Smoothed Heikin-Ashi Algorithms Optimized For Automated Trading SystemsDocument12 pagesSmoothed Heikin-Ashi Algorithms Optimized For Automated Trading SystemsCristóbal AcevedoNo ratings yet

- Chapter 1 Role of Financial Markets and InstitutionsDocument42 pagesChapter 1 Role of Financial Markets and Institutionschinuuchu100% (2)

- (CK Locke and Partners) CFD Trading ManualDocument8 pages(CK Locke and Partners) CFD Trading ManualSumit BhartiaNo ratings yet

- Financial Economics Course OverviewDocument66 pagesFinancial Economics Course OverviewKassahunNo ratings yet

- Financial EconomicsDocument159 pagesFinancial EconomicsLakachew GetasewNo ratings yet

- Role of Financial Markets and the Institutions that Facilitate Funds MovementDocument40 pagesRole of Financial Markets and the Institutions that Facilitate Funds MovementTayyab SaleemNo ratings yet

- CH 1Document26 pagesCH 1Chernet TeferaNo ratings yet

- Week 2 - SF: Role of Financial Markets and InstitutionsDocument39 pagesWeek 2 - SF: Role of Financial Markets and Institutionsciara WhiteNo ratings yet

- Chapter 1Document30 pagesChapter 1Hương Ngô Thị ThanhNo ratings yet

- Role of Financial Markets and InstitutionsDocument30 pagesRole of Financial Markets and InstitutionsĒsrar BalócNo ratings yet

- Chapter 1 Role of Financial Markets and InstitutionsDocument46 pagesChapter 1 Role of Financial Markets and InstitutionsJao FloresNo ratings yet

- Why Study Financial Markets? Financial Markets, Such As Bond and Stock Markets, Are Crucial in Our EconomyDocument27 pagesWhy Study Financial Markets? Financial Markets, Such As Bond and Stock Markets, Are Crucial in Our EconomyShaheena SanaNo ratings yet

- Financial Markets and InstrumentDocument30 pagesFinancial Markets and InstrumentAbdul Fattaah Bakhsh 1837065No ratings yet

- Financial Institutions & Financial Markets Module - 1: by Sanjeev TamhaneDocument35 pagesFinancial Institutions & Financial Markets Module - 1: by Sanjeev TamhaneSwagatJagtapNo ratings yet

- الشابتر الاولDocument3 pagesالشابتر الاولV VORTEXNo ratings yet

- Session 1 - 2 - Investment EnvironmentDocument96 pagesSession 1 - 2 - Investment EnvironmentPratyush GoelNo ratings yet

- Topic 2 - Long Term FinDocument25 pagesTopic 2 - Long Term FinAina KhairunnisaNo ratings yet

- Moving Funds Through The Financial SystemDocument27 pagesMoving Funds Through The Financial Systemjuan pranataNo ratings yet

- INVESTMENTDocument41 pagesINVESTMENTbereket nigussieNo ratings yet

- Optimizing Indian Financial SystemDocument41 pagesOptimizing Indian Financial SystemSakshi ChauhanNo ratings yet

- Ch.2 - Financial InstitutionsDocument21 pagesCh.2 - Financial InstitutionsbodyelkasabyNo ratings yet

- Chapter Two PDFDocument6 pagesChapter Two PDFKate PereiraNo ratings yet

- Constituents of The Financial System DD Intro NewDocument17 pagesConstituents of The Financial System DD Intro NewAnonymous bf1cFDuepPNo ratings yet

- Chap. 2. Financial MarketsDocument40 pagesChap. 2. Financial MarketsMichaelAngeloBattungNo ratings yet

- Role of financial markets and institutionsDocument3 pagesRole of financial markets and institutionsMeilin Denise MEDRANANo ratings yet

- Money, Banking & Finance: The Nature of Financial Intermediation K MatthewsDocument25 pagesMoney, Banking & Finance: The Nature of Financial Intermediation K MatthewsMuhammad SarmadNo ratings yet

- Financial SystemDocument13 pagesFinancial SystemAsad AkhlaqNo ratings yet

- Module 1 Money & Banking FinalDocument28 pagesModule 1 Money & Banking Finalblue252436No ratings yet

- Chapter 2 Overview of The Financial SystemDocument72 pagesChapter 2 Overview of The Financial SystemKokab Manzoor100% (1)

- Overview of Key Financial System Concepts - Markets, Instruments, Participants & RegulatorsDocument50 pagesOverview of Key Financial System Concepts - Markets, Instruments, Participants & RegulatorsshahyashrNo ratings yet

- Week 4Document42 pagesWeek 4Maqsood AhmadNo ratings yet

- The Financial SystemDocument47 pagesThe Financial SystemAlexa Daphne M. EquisabalNo ratings yet

- FMBODocument10 pagesFMBOHimani ChavanNo ratings yet

- Module 3 Merchant Banking: Nature of Services, structure of merchant banking firms. Financial Markets: Capital Market, Money Market, Forex Market, Linkage between the marketsDocument6 pagesModule 3 Merchant Banking: Nature of Services, structure of merchant banking firms. Financial Markets: Capital Market, Money Market, Forex Market, Linkage between the marketsSandeep YogeshwaranNo ratings yet

- Chapter 1 NotesDocument6 pagesChapter 1 NotesMax PossekNo ratings yet

- FINMARDocument28 pagesFINMARrou ziaNo ratings yet

- FM 13- FINCIAL MARKETSDocument80 pagesFM 13- FINCIAL MARKETSBrithney ButalidNo ratings yet

- Lecture 1 PDFDocument18 pagesLecture 1 PDFJulio GaziNo ratings yet

- 02 AE13 Overview of The Financial SystemDocument26 pages02 AE13 Overview of The Financial SystemLeojelaineIgcoyNo ratings yet

- Capital MarketDocument20 pagesCapital MarketMedhansh ShindeNo ratings yet

- Capital Market Risks and InvestmentsDocument27 pagesCapital Market Risks and InvestmentsNITISH BHARDWAJNo ratings yet

- Capital MarketsDocument19 pagesCapital MarketsCarla Jane Maitom TagoyNo ratings yet

- Ch 1Document36 pagesCh 1youssef ibrahimNo ratings yet

- Fmi 2Document41 pagesFmi 2Lebbe PuthaNo ratings yet

- Function and Structure of Financial MarketsDocument24 pagesFunction and Structure of Financial MarketsAniket GuptaNo ratings yet

- Capital Market Primary and Secondary MarketDocument27 pagesCapital Market Primary and Secondary Marketswastik guptaNo ratings yet

- financial marketsDocument34 pagesfinancial marketsmouli poliparthiNo ratings yet

- Lec 2 FM NumlDocument22 pagesLec 2 FM Numlpal 8311No ratings yet

- FE Chapter 4Document43 pagesFE Chapter 4dehinnetagimasNo ratings yet

- Understanding Finance Through Financial Markets and InstitutionsDocument38 pagesUnderstanding Finance Through Financial Markets and Institutionskc103038No ratings yet

- Understanding the Financial System and its Key ComponentsDocument5 pagesUnderstanding the Financial System and its Key ComponentsKen TuazonNo ratings yet

- CH - 12 (Global Capital Market)Document24 pagesCH - 12 (Global Capital Market)AhanafNo ratings yet

- Dinh Che Tai ChinhDocument38 pagesDinh Che Tai ChinhEli LiNo ratings yet

- Financial Imst &mark Unit - 2Document57 pagesFinancial Imst &mark Unit - 2KalkayeNo ratings yet

- Financial Institutions NotesDocument12 pagesFinancial Institutions NotesSherif ElSheemyNo ratings yet

- Unit 5Document97 pagesUnit 5Pankaj PrasadNo ratings yet

- Financial System GuideDocument24 pagesFinancial System GuideShochrulNo ratings yet

- Chapter Two: An Overview of The Financial SystemDocument43 pagesChapter Two: An Overview of The Financial SystemRaihan chowdhuryNo ratings yet

- Chapter 1-2Document40 pagesChapter 1-2jakeNo ratings yet

- Introduction To Financial SystemDocument22 pagesIntroduction To Financial SystemDivya JainNo ratings yet

- Research Variables DefinitionsDocument75 pagesResearch Variables DefinitionsShaheena SanaNo ratings yet

- Compensation Management SystemDocument10 pagesCompensation Management SystemShaheena SanaNo ratings yet

- Basic Concepts Organizational Composition & Role of HRM Management, Managers and OrganizationDocument12 pagesBasic Concepts Organizational Composition & Role of HRM Management, Managers and OrganizationShaheena SanaNo ratings yet

- Perception & DMDocument15 pagesPerception & DMShaheena SanaNo ratings yet

- Employee Relation ManagementDocument11 pagesEmployee Relation ManagementShaheena SanaNo ratings yet

- Performance Management SystemDocument17 pagesPerformance Management SystemShaheena SanaNo ratings yet

- Perception & DMDocument15 pagesPerception & DMShaheena SanaNo ratings yet

- Assignment No 4 of RMDocument12 pagesAssignment No 4 of RMShaheena SanaNo ratings yet

- South West AssignDocument2 pagesSouth West AssignShaheena SanaNo ratings yet

- Exercises of Paraphrasing - 1Document3 pagesExercises of Paraphrasing - 1Shaheena SanaNo ratings yet

- Ridha Rahim Research Methodology MSMS-2019: Basic and Applied Research, N.D)Document14 pagesRidha Rahim Research Methodology MSMS-2019: Basic and Applied Research, N.D)Shaheena SanaNo ratings yet

- AWS Seeks Engineer to Build Customer Billing SystemDocument3 pagesAWS Seeks Engineer to Build Customer Billing SystemShaheena SanaNo ratings yet

- RMM Lecture 30 Data Transformation ADocument26 pagesRMM Lecture 30 Data Transformation AShaheena SanaNo ratings yet

- Baron & Kenny PDFDocument10 pagesBaron & Kenny PDFBitter MoonNo ratings yet

- RMM Lecture 31-32 Data PresentationDocument40 pagesRMM Lecture 31-32 Data PresentationShaheena SanaNo ratings yet

- Assignment 2Document6 pagesAssignment 2Shaheena SanaNo ratings yet

- Research Methods: FieldworkDocument21 pagesResearch Methods: FieldworkShaheena SanaNo ratings yet

- Job Opportunity: Sui Northern GasDocument3 pagesJob Opportunity: Sui Northern GasShaheena SanaNo ratings yet

- Last AssignDocument2 pagesLast AssignShaheena SanaNo ratings yet

- Why Job Satisfaction and Employee Engagement MatterDocument4 pagesWhy Job Satisfaction and Employee Engagement MatterShaheena Sana100% (1)

- Shifa Hospital Problem ID and SolutionsDocument12 pagesShifa Hospital Problem ID and SolutionsShaheena SanaNo ratings yet

- Impact of Job Stress On Employee Performance: Research PaperDocument21 pagesImpact of Job Stress On Employee Performance: Research PaperShaheena SanaNo ratings yet

- Int PMS Final PaperDocument12 pagesInt PMS Final PaperShaheena SanaNo ratings yet

- Shaheena Hafeez S19MSMS011 HR Communication Strategy of Zong Internal CommunicationDocument5 pagesShaheena Hafeez S19MSMS011 HR Communication Strategy of Zong Internal CommunicationShaheena SanaNo ratings yet

- International Human Resource ManagementDocument4 pagesInternational Human Resource ManagementShaheena SanaNo ratings yet

- OBDocument2 pagesOBShaheena SanaNo ratings yet

- Job Opportunity: Sui Northern GasDocument3 pagesJob Opportunity: Sui Northern GasShaheena SanaNo ratings yet

- Ostracism 1Document13 pagesOstracism 1Shaheena SanaNo ratings yet

- Self EfficacyDocument80 pagesSelf EfficacyShaheena SanaNo ratings yet

- Psychological Wellbeing Meta AnalysisDocument16 pagesPsychological Wellbeing Meta AnalysisShaheena SanaNo ratings yet

- ST-GBOE Complaint AMENDEDDocument36 pagesST-GBOE Complaint AMENDEDPaulaGem607No ratings yet

- Stock ValuationDocument5 pagesStock ValuationDiana SaidNo ratings yet

- Oil & Gas: Equity ResearchDocument19 pagesOil & Gas: Equity ResearchForexliveNo ratings yet

- Project 2 Mbaf 502Document8 pagesProject 2 Mbaf 502Chukka VinayNo ratings yet

- Investments in Debt and Equity Securities Chapter 14 MCQsDocument38 pagesInvestments in Debt and Equity Securities Chapter 14 MCQsallysaallysaNo ratings yet

- Depository System and The Depositories Act, 1996Document22 pagesDepository System and The Depositories Act, 1996DALIP RADHENo ratings yet

- HC Egypt Macro 14 December 2009Document82 pagesHC Egypt Macro 14 December 2009Hesham TabarNo ratings yet

- Highlights: Hong Kong-Listed Mainland-Listed Cross-MarketDocument14 pagesHighlights: Hong Kong-Listed Mainland-Listed Cross-Marketadriaanbernard22No ratings yet

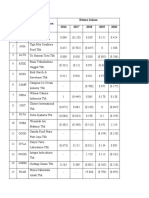

- No Kode Saham Nama Perusahan Return Saham 2016 2017 2018 2019 2020Document13 pagesNo Kode Saham Nama Perusahan Return Saham 2016 2017 2018 2019 2020Yusuf DahanaNo ratings yet

- 2008 Report Financial StatementsDocument76 pages2008 Report Financial StatementsbookfishNo ratings yet

- Factors Affecting Investment Behaviour Among Young ProfessionalsDocument6 pagesFactors Affecting Investment Behaviour Among Young ProfessionalsInternational Jpurnal Of Technical Research And ApplicationsNo ratings yet

- Order in The Matter of Shivalik Cotex Limited and 10 PersonsDocument14 pagesOrder in The Matter of Shivalik Cotex Limited and 10 PersonsShyam SunderNo ratings yet

- CH-4 - Organization and Functioning of Securities MarketDocument13 pagesCH-4 - Organization and Functioning of Securities MarketMoin khanNo ratings yet

- Annual RPT 2009Document122 pagesAnnual RPT 2009Nishant GargNo ratings yet

- Mutual Find SBIDocument25 pagesMutual Find SBIMäñåň FãłķëNo ratings yet

- Investagrams OutlineDocument3 pagesInvestagrams OutlineRoseballToledoNo ratings yet

- Genmath Q2 Week4Document36 pagesGenmath Q2 Week4ShennieNo ratings yet

- Project On SharekhanDocument55 pagesProject On SharekhanjatinNo ratings yet

- MGMT2023 Lecture 7 STOCK VALUATION - Parts I, II IIIDocument86 pagesMGMT2023 Lecture 7 STOCK VALUATION - Parts I, II IIIIsmadth2918388No ratings yet

- How To Convert Your IRA 401k EbookDocument13 pagesHow To Convert Your IRA 401k EbookTạ Minh TrãiNo ratings yet

- Chag PDFDocument5 pagesChag PDFShehry VibesNo ratings yet

- VipulDocument83 pagesVipulheena572003No ratings yet

- Exercise-Stock ValuationDocument2 pagesExercise-Stock Valuationchasnaa lidzamalihaNo ratings yet

- UGBA103 Final Fall 2016Document5 pagesUGBA103 Final Fall 2016Billy bobNo ratings yet