You might also like

- Functions of Treaty BodiesDocument10 pagesFunctions of Treaty BodiesSam Sy-HenaresNo ratings yet

- Insolvency Act 1936Document96 pagesInsolvency Act 1936Man WomanNo ratings yet

- DocStatutory Construction Case DigestDocument14 pagesDocStatutory Construction Case DigestDieanne MaeNo ratings yet

- Generally Accepted Auditing Standards A Complete Guide - 2020 EditionFrom EverandGenerally Accepted Auditing Standards A Complete Guide - 2020 EditionNo ratings yet

- Judicial DepositDocument16 pagesJudicial DepositZydalgLadyz NeadNo ratings yet

- Modes of Payment For ImportsDocument5 pagesModes of Payment For ImportsIsabelle Bañadera LcbNo ratings yet

- CD and Promisory NoteDocument18 pagesCD and Promisory NoteChar LeneNo ratings yet

- Requirements of A Legally Binding ContractDocument10 pagesRequirements of A Legally Binding ContractClitonTayNo ratings yet

- StudyAbroad TravelWaiverDocument1 pageStudyAbroad TravelWaiveridkthisusernameNo ratings yet

- Letter of Credit - Process: Step 1 - Issuance of LCDocument8 pagesLetter of Credit - Process: Step 1 - Issuance of LCRuchitha PrakashNo ratings yet

- Articles of IncorporationDocument11 pagesArticles of IncorporationRache GutierrezNo ratings yet

- Order. - Ex Parte or Upon Motion WithDocument6 pagesOrder. - Ex Parte or Upon Motion WithSakinah MangotaraNo ratings yet

- Death ClaimsDocument60 pagesDeath ClaimsSiddhartha SinhaNo ratings yet

- PR Tax Withholding Exemption Form PDFDocument2 pagesPR Tax Withholding Exemption Form PDFheidi reyesNo ratings yet

- Doctrine of Ultra ViresDocument3 pagesDoctrine of Ultra ViresTony Davis100% (1)

- Notes On Negotiable Instrument Act 1881Document6 pagesNotes On Negotiable Instrument Act 1881Pranjal SrivastavaNo ratings yet

- Non Disc Hold HarmDocument4 pagesNon Disc Hold HarmSylvester MooreNo ratings yet

- Contract SsDocument20 pagesContract SsMir Mahbubur RahmanNo ratings yet

- Negotin Commercial LawDocument27 pagesNegotin Commercial LawChristopher Michael OnaNo ratings yet

- General Durable Power of Attorney Effective Upon ExecutionDocument5 pagesGeneral Durable Power of Attorney Effective Upon Executionsable1234No ratings yet

- Notes On Pretrial Brief and Judicial AffidavitDocument16 pagesNotes On Pretrial Brief and Judicial AffidavitJamellen De Leon BenguetNo ratings yet

- Chapter 4 - Co-Ownership, Estates and TrustsDocument8 pagesChapter 4 - Co-Ownership, Estates and TrustsLiRose SmithNo ratings yet

- Enforcement of Security Interests in Banking TransactionsDocument20 pagesEnforcement of Security Interests in Banking TransactionsAbhjeet Kumar Sinha100% (1)

- Revocable Letter of Credit Can Be Revoked Without The Consent of TheDocument3 pagesRevocable Letter of Credit Can Be Revoked Without The Consent of ThePankaj ThapaNo ratings yet

- Financial Accounting Standards BoardDocument9 pagesFinancial Accounting Standards BoardTarun GuntnurNo ratings yet

- What Is An Affidavit and What Is Its PurposeDocument1 pageWhat Is An Affidavit and What Is Its PurposeHazel-mae LabradaNo ratings yet

- Defamation PDFDocument3 pagesDefamation PDFRanjan BaradurNo ratings yet

- Annex B BOA FORM INDIVIDUAL PARTNERSHIP 1 PDFDocument3 pagesAnnex B BOA FORM INDIVIDUAL PARTNERSHIP 1 PDFJun Guerzon PaneloNo ratings yet

- Appellate March 9 Ruling in Klein V JCOPEDocument4 pagesAppellate March 9 Ruling in Klein V JCOPENew York PostNo ratings yet

- Study Material For This LectureDocument12 pagesStudy Material For This Lectureosaie100% (1)

- Petition To Stop The Racial Profiling of Asian American & Asian Immigrants - Advancing Justice - AAJCDocument1,483 pagesPetition To Stop The Racial Profiling of Asian American & Asian Immigrants - Advancing Justice - AAJCOjieze OsedebamhenNo ratings yet

- Correct Application and InterpretationDocument106 pagesCorrect Application and Interpretationbiodun o100% (1)

- SB277-What It MeansDocument11 pagesSB277-What It MeansJohn JacksonNo ratings yet

- Week 2: The Hierarchy of The Courts and Common Law and EquityDocument11 pagesWeek 2: The Hierarchy of The Courts and Common Law and EquityGerardNo ratings yet

- US Internal Revenue Service: Irb04-43Document27 pagesUS Internal Revenue Service: Irb04-43IRSNo ratings yet

- Contract To SellDocument3 pagesContract To SellIan GermanNo ratings yet

- Mercantile Law NotesDocument42 pagesMercantile Law NotesMariel DavidNo ratings yet

- ACLU Letter To The Hawaii DMVDocument12 pagesACLU Letter To The Hawaii DMVHonolulu Star-AdvertiserNo ratings yet

- Letter of CreditDocument2 pagesLetter of CreditadifaahNo ratings yet

- Accounting For Estates of A Deceased PersonDocument12 pagesAccounting For Estates of A Deceased PersonNicole TaylorNo ratings yet

- Neglaw EpassfinalDocument68 pagesNeglaw EpassfinalrdNo ratings yet

- Non Taxable IncomeDocument4 pagesNon Taxable IncomeSesshomaruHimuraNo ratings yet

- Preliminary AttachmentDocument193 pagesPreliminary AttachmentDuke SucgangNo ratings yet

- Civil Action by Non-Prisoner PacketDocument59 pagesCivil Action by Non-Prisoner PacketAlan EngleNo ratings yet

- Sec 34. Special Indorsement Indorsement in BlankDocument5 pagesSec 34. Special Indorsement Indorsement in BlankKathleen AcunaNo ratings yet

- Al Nashiri Court DecisionDocument31 pagesAl Nashiri Court DecisionWashington ExaminerNo ratings yet

- ArticlesofconfederationDocument6 pagesArticlesofconfederationLonnie L Grady-ElNo ratings yet

- Promissory Note, Bill of Exchange, CheckDocument2 pagesPromissory Note, Bill of Exchange, CheckJames DecolongonNo ratings yet

- The Depositories Act 1996Document3 pagesThe Depositories Act 1996jineshshah1991No ratings yet

- Debits and CreditsDocument1 pageDebits and Creditsomda4uuNo ratings yet

- Petition & Cost BondDocument24 pagesPetition & Cost BondDan LehrNo ratings yet

- t1 Preventive Relief - InjunctionDocument29 pagest1 Preventive Relief - InjunctionFateh NajwanNo ratings yet

- Waller v. City of New York, Temporary Restraining Order by J. Lucy Billings and Plaintiffs Pleading on Order to Show Cause Before J. Michael Stallman, Case No. 112957-2011 (N.Y. County Supr. Ct. Nov. 15, 2011)Document9 pagesWaller v. City of New York, Temporary Restraining Order by J. Lucy Billings and Plaintiffs Pleading on Order to Show Cause Before J. Michael Stallman, Case No. 112957-2011 (N.Y. County Supr. Ct. Nov. 15, 2011)Michael GinsborgNo ratings yet

- US Internal Revenue Service: I3520 - 1996Document12 pagesUS Internal Revenue Service: I3520 - 1996IRSNo ratings yet

- Bank Secrecy LawDocument8 pagesBank Secrecy LawHermie Dela CruzNo ratings yet

- DTC Agreement Between Jamaica and United StatesDocument40 pagesDTC Agreement Between Jamaica and United StatesOECD: Organisation for Economic Co-operation and DevelopmentNo ratings yet

- 7 UsufructDocument33 pages7 Usufructsovxxx100% (1)

- Of in It It of Jurat of of of of in Or: Extra ADocument4 pagesOf in It It of Jurat of of of of in Or: Extra AAngel CabanNo ratings yet

- Law On Sales AssignmentDocument13 pagesLaw On Sales AssignmentGennia Mae MartinezNo ratings yet

- II. Trade Finance Methods and Instruments: An Overview: A. IntroductionDocument11 pagesII. Trade Finance Methods and Instruments: An Overview: A. IntroductionSandeep SinghNo ratings yet

- Madhuban Bapudham SchemeDocument3 pagesMadhuban Bapudham SchemerahulNo ratings yet

- Course OutlineDocument13 pagesCourse OutlineKabile MwitaNo ratings yet

- Account - 11208100007124 Saiyad Akil Zilani: AddressDocument4 pagesAccount - 11208100007124 Saiyad Akil Zilani: AddressAamena BanuNo ratings yet

- MBA Syllabus 21-08-2020 FinalDocument160 pagesMBA Syllabus 21-08-2020 Finalgundarapu deepika0% (1)

- SSPUSADVDocument1 pageSSPUSADVLuz AmparoNo ratings yet

- Mahindra Sona R 22102013Document3 pagesMahindra Sona R 22102013ukalNo ratings yet

- PreviewDocument4 pagesPreviewJoshua PerumalaNo ratings yet

- Golden Rules of AccountingDocument5 pagesGolden Rules of AccountingVinay ChintamaneniNo ratings yet

- Financial Statement AnalysisDocument26 pagesFinancial Statement Analysissagar7No ratings yet

- XEROXDocument25 pagesXEROXSALONY METHINo ratings yet

- Personal Budget SpreadsheetDocument8 pagesPersonal Budget Spreadsheetnutescu.alexNo ratings yet

- USDA USFS Nursery Manual For Native Plants - A Guide For Tribal Nurseries - Nursery Management Nursery Manual For Native Plants by United States Department of Agriculture - U.S. Forest Service PDFDocument309 pagesUSDA USFS Nursery Manual For Native Plants - A Guide For Tribal Nurseries - Nursery Management Nursery Manual For Native Plants by United States Department of Agriculture - U.S. Forest Service PDFGreg John Peterson100% (2)

- Public Trust Registration Office: Trust Accounts Submission Verification FormDocument1 pagePublic Trust Registration Office: Trust Accounts Submission Verification FormHashtag ComputersNo ratings yet

- Reading Practice TestDocument23 pagesReading Practice Teststephen vaiNo ratings yet

- ZTBL Annual ReportDocument64 pagesZTBL Annual ReportHaris NaseemNo ratings yet

- CFA Research Report - Team APUDocument30 pagesCFA Research Report - Team APUAnonymous 6A1OAiGidZNo ratings yet

- Director of Finance and Administration TFF JOB DESCRIPTIONDocument2 pagesDirector of Finance and Administration TFF JOB DESCRIPTIONJackson M AudifaceNo ratings yet

- H HJ KJHKJDocument15 pagesH HJ KJHKJEmmanuel BatinganNo ratings yet

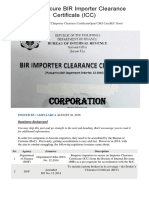

- How To Secure BIR Importer Clearance CertificateDocument6 pagesHow To Secure BIR Importer Clearance CertificateEmely SolonNo ratings yet

- New Zealand 2009 Financial Knowledge SurveyDocument11 pagesNew Zealand 2009 Financial Knowledge SurveywmhuthnanceNo ratings yet

- Fintelum Opens Investment Into New Tokenisation Project KEEPPDocument3 pagesFintelum Opens Investment Into New Tokenisation Project KEEPPPR.comNo ratings yet

- 3 - 01 - 10 - Appendix L - Letter of RepresentationDocument4 pages3 - 01 - 10 - Appendix L - Letter of RepresentationHariprasad B RNo ratings yet

- 3 Sept 2018Document50 pages3 Sept 2018siva kNo ratings yet

- Sample Loan ProposalDocument20 pagesSample Loan Proposalhardmoneyteam94% (16)

- Sample Resume, Mem/Mba: Current Address Permanent Address (Optional) Current Home /cell Phone Jane - Smith@yale - EduDocument1 pageSample Resume, Mem/Mba: Current Address Permanent Address (Optional) Current Home /cell Phone Jane - Smith@yale - EduGurpreetNo ratings yet

- Am113 Module 1-PrelimDocument22 pagesAm113 Module 1-PrelimMaryjel SumambotNo ratings yet

- Soft OfferDocument3 pagesSoft OfferRicardo CagnoniNo ratings yet

- Student Name: Luu Gia Bao Student ID: 1567033: HW Assignment For Week 3Document5 pagesStudent Name: Luu Gia Bao Student ID: 1567033: HW Assignment For Week 3Lưu Gia BảoNo ratings yet

- Annual Report 2019 PDFDocument188 pagesAnnual Report 2019 PDFowen.rijantoNo ratings yet