You might also like

- Tutorial 4 QuestionsDocument4 pagesTutorial 4 Questionsguan junyan0% (1)

- Q and As-Corporate Financial Management - June 2010 Dec 2010 and June 2011Document71 pagesQ and As-Corporate Financial Management - June 2010 Dec 2010 and June 2011chisomo_phiri72290% (2)

- Spreadsheet Exercise-Drillago CompanyDocument4 pagesSpreadsheet Exercise-Drillago CompanyQueenie MillorNo ratings yet

- T.1042 Maliyy T Hlili Aynur F NdiyevaDocument15 pagesT.1042 Maliyy T Hlili Aynur F NdiyevaelvitaNo ratings yet

- List of Key Financial Ratios: Formulas and Calculation Examples Defined for Different Types of Profitability Ratios and the Other Most Important Financial RatiosFrom EverandList of Key Financial Ratios: Formulas and Calculation Examples Defined for Different Types of Profitability Ratios and the Other Most Important Financial RatiosNo ratings yet

- Fins3635 Final NotesDocument44 pagesFins3635 Final NotesjoannamanngoNo ratings yet

- CPA Review: Excel Professional Services IncDocument7 pagesCPA Review: Excel Professional Services IncMm100% (1)

- Chapter 25Document13 pagesChapter 25Marjorie Ponce100% (1)

- P1 Reviewer ISAPDocument13 pagesP1 Reviewer ISAPVenus B. MacatuggalNo ratings yet

- Projected Cash Flow StatementDocument6 pagesProjected Cash Flow StatementIqtadar AliNo ratings yet

- FCFE Notes by DamodaranDocument34 pagesFCFE Notes by DamodaranNikhil ChitaliaNo ratings yet

- Business Analysis & Valuation Fcfe: Free Cash FlowDocument63 pagesBusiness Analysis & Valuation Fcfe: Free Cash Flowrahul.rishabh9999284No ratings yet

- Value + + + FCF FCF FCF (1 + WACC) (1 + WACC) (1 + WACC) ..Document33 pagesValue + + + FCF FCF FCF (1 + WACC) (1 + WACC) (1 + WACC) ..Manabendra DasNo ratings yet

- Chapter Fifteen Full-Information Forecasting, Valuation, and Business Strategy AnalysisDocument56 pagesChapter Fifteen Full-Information Forecasting, Valuation, and Business Strategy AnalysisRitesh Batra100% (4)

- II. The Two-Stage FCFE ModelDocument7 pagesII. The Two-Stage FCFE ModelzZl3Ul2NNINGZzNo ratings yet

- FIN 213 Review Questions: Question OneDocument16 pagesFIN 213 Review Questions: Question OneJustus MusilaNo ratings yet

- Addl Notes - FCFF Model PDFDocument17 pagesAddl Notes - FCFF Model PDFRoyLadiasanNo ratings yet

- Chapter No.06 Company Analysis and Stock ValuationDocument40 pagesChapter No.06 Company Analysis and Stock ValuationBlue StoneNo ratings yet

- DCF Method of ValuationDocument45 pagesDCF Method of Valuationnotes 1No ratings yet

- Financial Management: Thursday 9 June 2011Document9 pagesFinancial Management: Thursday 9 June 2011catcat1122No ratings yet

- 4.6 Model Assumptions GuidebookDocument6 pages4.6 Model Assumptions GuidebookAlfred DurontNo ratings yet

- FINA 410 - Exercises (NOV)Document7 pagesFINA 410 - Exercises (NOV)said100% (1)

- Evaluation of Financial Performance: Finance 311 1Document33 pagesEvaluation of Financial Performance: Finance 311 1linhtinh8xNo ratings yet

- FCFEDocument22 pagesFCFEFuzuliNo ratings yet

- Free Cash Flow and Its UsesDocument22 pagesFree Cash Flow and Its UsesAnand Deshpande67% (3)

- FM Case 5 14ADocument43 pagesFM Case 5 14Asquishbug100% (2)

- Recap: Eps and Bvps Diluted: Convertible Instruments Convertible Bond Convertible Preff Stock EsosDocument16 pagesRecap: Eps and Bvps Diluted: Convertible Instruments Convertible Bond Convertible Preff Stock Esosnoratiqah zakariaNo ratings yet

- AFA - Earnings Drivers EtcDocument24 pagesAFA - Earnings Drivers EtcHYUN JUNG KIMNo ratings yet

- Profitability AnalysisDocument9 pagesProfitability AnalysisBurhan Al MessiNo ratings yet

- Corporate FinanceDocument5 pagesCorporate FinancemallikaNo ratings yet

- Seminar 10Document24 pagesSeminar 10Tharindu PereraNo ratings yet

- Capital Investment DecisionsDocument12 pagesCapital Investment Decisionsmoza salimNo ratings yet

- Wa0013Document54 pagesWa0013Maria AbrahamNo ratings yet

- Midterm Review - Key ConceptsDocument10 pagesMidterm Review - Key ConceptsGurpreetNo ratings yet

- SEx 12Document64 pagesSEx 12Deron Lai100% (1)

- HKICPA QP Exam (Module A) Sep2004 AnswerDocument14 pagesHKICPA QP Exam (Module A) Sep2004 Answercynthia tsuiNo ratings yet

- Concept Questions: Chapter Twelve The Analysis of Growth and Sustainable EarningsDocument64 pagesConcept Questions: Chapter Twelve The Analysis of Growth and Sustainable EarningsceojiNo ratings yet

- Financial Statements, Cash Flow, and TaxesDocument44 pagesFinancial Statements, Cash Flow, and TaxesreNo ratings yet

- Dividend PolicyDocument8 pagesDividend PolicySumit PandeyNo ratings yet

- READING 8 Free Cashflow (Equity Valuation)Document25 pagesREADING 8 Free Cashflow (Equity Valuation)DandyNo ratings yet

- Lecture 28Document34 pagesLecture 28Riaz Baloch NotezaiNo ratings yet

- Chapter 6 Valuating StocksDocument46 pagesChapter 6 Valuating StocksCezarene FernandoNo ratings yet

- Chapter-Two: Financial Planning and ProjectionDocument6 pagesChapter-Two: Financial Planning and Projectionমেহেদী হাসানNo ratings yet

- Chapter 19: Financial Statement AnalysisDocument11 pagesChapter 19: Financial Statement AnalysisSilviu TrebuianNo ratings yet

- Chapter 2 Buiness FinanxceDocument38 pagesChapter 2 Buiness FinanxceShajeer HamNo ratings yet

- Final Review Session SPR12RปDocument10 pagesFinal Review Session SPR12RปFight FionaNo ratings yet

- Lecture 3: Emerging Stock MarketsDocument115 pagesLecture 3: Emerging Stock MarketsShweta ShrivastavaNo ratings yet

- Pma FacsDocument27 pagesPma FacsGopi NathanNo ratings yet

- Slides - Session 5Document49 pagesSlides - Session 5Murte BolaNo ratings yet

- Financial Statements & AnalysisDocument36 pagesFinancial Statements & AnalysisMahiNo ratings yet

- Final Statement Assessment 1Document7 pagesFinal Statement Assessment 1AssignemntNo ratings yet

- CH 4Document20 pagesCH 4Waheed Zafar100% (1)

- Financial Management, Lecture 5 & 6Document27 pagesFinancial Management, Lecture 5 & 6Muhammad ImranNo ratings yet

- CV Midterm Exam 1 - Solution GuideDocument11 pagesCV Midterm Exam 1 - Solution GuideKala Paul100% (1)

- Lucky Cement Final Project Report On: Financial Statement AnalysisDocument25 pagesLucky Cement Final Project Report On: Financial Statement AnalysisPrecious BarbieNo ratings yet

- M09 Berk0821 04 Ism C091Document15 pagesM09 Berk0821 04 Ism C091Linda VoNo ratings yet

- Annuity Tables p6Document17 pagesAnnuity Tables p6williammasvinuNo ratings yet

- Financial Management Tutorial QuestionsDocument8 pagesFinancial Management Tutorial QuestionsStephen Olieka100% (2)

- Financial Statements, Cash Flow and TaxesDocument44 pagesFinancial Statements, Cash Flow and TaxesAli JumaniNo ratings yet

- Reading 13 Integration of Financial Statement Analysis Techniques - AnswersDocument21 pagesReading 13 Integration of Financial Statement Analysis Techniques - Answerstristan.riolsNo ratings yet

- Management Control Systems: University Question - AnswersDocument19 pagesManagement Control Systems: University Question - AnswersvaishalikatkadeNo ratings yet

- Financial Statements, Cash Flow, and TaxesDocument30 pagesFinancial Statements, Cash Flow, and TaxesDivina Grace Rodriguez - LibreaNo ratings yet

- Applied Corporate Finance. What is a Company worth?From EverandApplied Corporate Finance. What is a Company worth?Rating: 3 out of 5 stars3/5 (2)

- Offices of Bank Holding Company Revenues World Summary: Market Values & Financials by CountryFrom EverandOffices of Bank Holding Company Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Economic and Business Forecasting: Analyzing and Interpreting Econometric ResultsFrom EverandEconomic and Business Forecasting: Analyzing and Interpreting Econometric ResultsNo ratings yet

- List of the Most Important Financial Ratios: Formulas and Calculation Examples Defined for Different Types of Key Financial RatiosFrom EverandList of the Most Important Financial Ratios: Formulas and Calculation Examples Defined for Different Types of Key Financial RatiosNo ratings yet

- M11 Estate Planning and Family BreakdownDocument60 pagesM11 Estate Planning and Family BreakdownjoannamanngoNo ratings yet

- Week 3: Lecture Slides: DCF - Earnings and Terminal Value Chapter 10 and 12Document21 pagesWeek 3: Lecture Slides: DCF - Earnings and Terminal Value Chapter 10 and 12joannamanngoNo ratings yet

- Fins3635 Final NotesDocument44 pagesFins3635 Final NotesjoannamanngoNo ratings yet

- Sample TestDocument9 pagesSample Teststudunt100% (2)

- Fins3635 Final NotesDocument44 pagesFins3635 Final NotesjoannamanngoNo ratings yet

- FINS 3635 Short Computer Assignment-2017-2Document1 pageFINS 3635 Short Computer Assignment-2017-2joannamanngoNo ratings yet

- Global Leadership Program 2017Document14 pagesGlobal Leadership Program 2017joannamanngoNo ratings yet

- Problem Set 8Document4 pagesProblem Set 8joannamanngoNo ratings yet

- Social Psych Practice MCQDocument3 pagesSocial Psych Practice MCQjoannamanngoNo ratings yet

- Social Psych Practice MCQDocument3 pagesSocial Psych Practice MCQjoannamanngoNo ratings yet

- Developmental PsychDocument62 pagesDevelopmental PsychjoannamanngoNo ratings yet

- FINS 3616 Lecture Notes-Week 1Document38 pagesFINS 3616 Lecture Notes-Week 1joannamanngoNo ratings yet

- Chapter 15: Foreign Exchange (FX) MarketsDocument32 pagesChapter 15: Foreign Exchange (FX) MarketsjoannamanngoNo ratings yet

- UNSW FINS2624 Problem Set 5Document2 pagesUNSW FINS2624 Problem Set 5joannamanngo100% (1)

- Portfolio Performance EvaluationDocument11 pagesPortfolio Performance EvaluationjoannamanngoNo ratings yet

- This Study Resource Was: ExercisesDocument9 pagesThis Study Resource Was: ExercisesNah HamzaNo ratings yet

- Digest - PFRS 3 and PFRS 10Document4 pagesDigest - PFRS 3 and PFRS 10Elizabeth DumawalNo ratings yet

- MAC3701 Question Bank 2016Document65 pagesMAC3701 Question Bank 2016Blessings MunkuliNo ratings yet

- Auditing Problems With AnswersDocument12 pagesAuditing Problems With AnswersFlorie May HizoNo ratings yet

- Accounting WorksheetDocument6 pagesAccounting WorksheetAlexa BellNo ratings yet

- Accounting Standard2Document24 pagesAccounting Standard2shajiNo ratings yet

- M3 - Nila Savitri - 21221488 - 2EB09 (AKM 1)Document6 pagesM3 - Nila Savitri - 21221488 - 2EB09 (AKM 1)rully movizarNo ratings yet

- Summative QuizDocument2 pagesSummative QuizVIRGIL KIT AUGUSTIN ABANILLANo ratings yet

- Consoliated Group Financial Report - Jane Lazar CHP 12.1Document1 pageConsoliated Group Financial Report - Jane Lazar CHP 12.1Ng GraceNo ratings yet

- PDF Solution Manual Partnership Amp Corporation 2014 2015pdfDocument85 pagesPDF Solution Manual Partnership Amp Corporation 2014 2015pdfGenevieve Anne AlagonNo ratings yet

- Ratio Analysis FormulaeDocument3 pagesRatio Analysis FormulaeErica DsouzaNo ratings yet

- FSA Midterm Exam FormattedDocument8 pagesFSA Midterm Exam Formattedkarthikmaddula007_66No ratings yet

- Automobile Sector of PakistanDocument28 pagesAutomobile Sector of PakistanImama KhanNo ratings yet

- Toaz - Info Acca f3 LRP Questions PRDocument64 pagesToaz - Info Acca f3 LRP Questions PRArt and Fashion galleryNo ratings yet

- Braun Ma4 SM 10Document72 pagesBraun Ma4 SM 10noblevermaNo ratings yet

- Tutorial 7 Chapter 15: Cash Conversion CycleDocument8 pagesTutorial 7 Chapter 15: Cash Conversion CycleAlvaroNo ratings yet

- Sol. Man. - Chapter 15 - Accounting For CorporationsDocument15 pagesSol. Man. - Chapter 15 - Accounting For Corporationspehik100% (1)

- QUIZ 6 Joint ArrangementDocument2 pagesQUIZ 6 Joint ArrangementEki SunriseNo ratings yet

- SV Exercises FA1Document13 pagesSV Exercises FA1Nguyễn Văn AnNo ratings yet

- BNI Sekuritas ANTM - Site Visit Key TakeawaysDocument7 pagesBNI Sekuritas ANTM - Site Visit Key Takeawaysbudi handokoNo ratings yet

- What Is Accounts Receivable (AR) ?Document2 pagesWhat Is Accounts Receivable (AR) ?Art B. EnriquezNo ratings yet

- 3 - Discussion - Joint Products and ByproductsDocument2 pages3 - Discussion - Joint Products and ByproductsCharles TuazonNo ratings yet

- True-False: 16 - Intercoprporate InvestmentsDocument9 pagesTrue-False: 16 - Intercoprporate InvestmentsEych MendozaNo ratings yet

- AC 212 Test 1 SolutionDocument4 pagesAC 212 Test 1 SolutionJoyce PamendaNo ratings yet

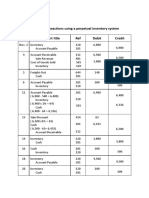

- Group 1: A) Journalize The Transactions Using A Perpetual Inventory System Date Account Title Ref Debit CreditDocument6 pagesGroup 1: A) Journalize The Transactions Using A Perpetual Inventory System Date Account Title Ref Debit CreditQuỳnh'ss Đắc'ssNo ratings yet