You might also like

- Final Accounts of Sole ProprietorDocument33 pagesFinal Accounts of Sole Proprietorrasmi78009No ratings yet

- Sole Proprietorship Final AccountsDocument23 pagesSole Proprietorship Final Accountsjaiccha420No ratings yet

- Chapter 9: Financial StatementDocument10 pagesChapter 9: Financial Statementhussain shablilNo ratings yet

- Income Statement and Balance SheetDocument20 pagesIncome Statement and Balance Sheetpankaj tiwariNo ratings yet

- 1.final Accounts by NavkarDocument24 pages1.final Accounts by NavkarKID ZONENo ratings yet

- Practice Material On Cost of Goods Manufectured and Sold Statement. MGT402Document34 pagesPractice Material On Cost of Goods Manufectured and Sold Statement. MGT402Syed Ali HaiderNo ratings yet

- DAIBB Management of AccountingDocument3 pagesDAIBB Management of Accountingdon_mahinNo ratings yet

- Financial Statements Formate 3.1Document15 pagesFinancial Statements Formate 3.1vkvivekkm163No ratings yet

- Final Account: With AdjustmentDocument49 pagesFinal Account: With AdjustmentPandit Niraj Dilip Sharma100% (1)

- Financial StatementsDocument24 pagesFinancial Statementstranlamtuyen1911No ratings yet

- CA ClubIndia 35 Cost AccountingDocument17 pagesCA ClubIndia 35 Cost AccountingAshwin S ChettiarNo ratings yet

- Unit 1 Book Keeping, Accounting, AS & IFRS PDFDocument43 pagesUnit 1 Book Keeping, Accounting, AS & IFRS PDFShreyash PardeshiNo ratings yet

- Class Notes: Class: XI Topic: Financial StatementDocument3 pagesClass Notes: Class: XI Topic: Financial StatementRajeev ShuklaNo ratings yet

- Final AccountsDocument12 pagesFinal AccountsPraveenNo ratings yet

- Final AcccountDocument20 pagesFinal Acccountbtamilarasan88No ratings yet

- Final AccountDocument10 pagesFinal AccountSaket AgarwalNo ratings yet

- PGBPDocument14 pagesPGBPSaurav MedhiNo ratings yet

- Final AccountDocument47 pagesFinal Accountsakshi tomarNo ratings yet

- Final Accounts (Financial Statements)Document6 pagesFinal Accounts (Financial Statements)Raaghav SrinivasanNo ratings yet

- Acctng NotesDocument13 pagesAcctng NotesJeremae EtiongNo ratings yet

- Final AccountsDocument7 pagesFinal Accountssubhasishmajumdar0% (2)

- PARTNERSHIPDocument72 pagesPARTNERSHIPDivya RaniNo ratings yet

- Types of Valuing Goodwill: (A) Simple Profit MethodDocument3 pagesTypes of Valuing Goodwill: (A) Simple Profit MethodcnagadeepaNo ratings yet

- Chapter 2. Financial Mangerial ReportingDocument9 pagesChapter 2. Financial Mangerial Reportingnaveen728No ratings yet

- Fabm ReviewerDocument16 pagesFabm Reviewersab lightningNo ratings yet

- Chapter-02 Statement of Cash FlowsDocument16 pagesChapter-02 Statement of Cash Flowsmd. hasanuzzamanNo ratings yet

- Statement of Comprehensive IncomeDocument13 pagesStatement of Comprehensive IncomeJethro RafaNo ratings yet

- Final Accounts NotesDocument6 pagesFinal Accounts NotesVinay K TanguturNo ratings yet

- Chapter - 2 Problem Related Financial StatementDocument6 pagesChapter - 2 Problem Related Financial StatementAshfaq ZameerNo ratings yet

- Module 3 Final AccountsDocument31 pagesModule 3 Final Accountskaushalrajsinhjanvar427No ratings yet

- MEFA 5 UnitDocument30 pagesMEFA 5 UnitSuhasNo ratings yet

- Adobe Scan 20-Apr-2023Document6 pagesAdobe Scan 20-Apr-2023Notes GlobeNo ratings yet

- Acf100 New ImportantDocument10 pagesAcf100 New ImportantNikunjGuptaNo ratings yet

- ECO 415 Chapter 8Document34 pagesECO 415 Chapter 8Nur NazirahNo ratings yet

- Funds Flow and Cash Flow NotesDocument12 pagesFunds Flow and Cash Flow NotesSoumendra RoyNo ratings yet

- Notes-Unit-3-Final Accounts - (Partial)Document12 pagesNotes-Unit-3-Final Accounts - (Partial)happy lifeNo ratings yet

- AccountancyDocument45 pagesAccountancyBRISTI SAHANo ratings yet

- Presentation of Financial Statements (IAS 1)Document30 pagesPresentation of Financial Statements (IAS 1)Ashura ShaibNo ratings yet

- Cash FlowDocument8 pagesCash FlowSUPERHERO WORLDNo ratings yet

- Introduction To Regular Income TaxationDocument45 pagesIntroduction To Regular Income Taxationcarl patNo ratings yet

- Final AccountsDocument43 pagesFinal AccountsJincy Geevarghese100% (1)

- 1 Deductions From Gross Income-FinalDocument24 pages1 Deductions From Gross Income-FinalSharon Ann BasulNo ratings yet

- Lecture 3 2015Document31 pagesLecture 3 2015Ashish MathewNo ratings yet

- Explain The Procedure of Reconciliation of Financial and Cost Accounting DataDocument6 pagesExplain The Procedure of Reconciliation of Financial and Cost Accounting DataKritika JainNo ratings yet

- Egyptian Income Tax Part OneDocument14 pagesEgyptian Income Tax Part OneAhmed Abdel-FattahNo ratings yet

- Minimum Corporate Income Tax (MCIT) Improperly Accumulated Earnings Tax (IAET) Gross Income Tax (GIT)Document18 pagesMinimum Corporate Income Tax (MCIT) Improperly Accumulated Earnings Tax (IAET) Gross Income Tax (GIT)Anne Mel Bariquit100% (1)

- Chapter-02-Cash Flow SatementDocument21 pagesChapter-02-Cash Flow SatementSafeen LabibNo ratings yet

- Mbaf0701 - Far - Unit - 2Document13 pagesMbaf0701 - Far - Unit - 2RahulNo ratings yet

- DAIBB Management of AccountingDocument4 pagesDAIBB Management of AccountingMuhammad Akmal HossainNo ratings yet

- Free Basic Short Financial Accounting - 2f20dc43 314d 49bf A7e8 F398e2c49e3dDocument32 pagesFree Basic Short Financial Accounting - 2f20dc43 314d 49bf A7e8 F398e2c49e3dCareer and TechnologyNo ratings yet

- Financial, Managerial Accounting and ReportingDocument29 pagesFinancial, Managerial Accounting and ReportingleenajaiswalNo ratings yet

- Statement of Comprehensive Income (Reviewer)Document4 pagesStatement of Comprehensive Income (Reviewer)ChinNo ratings yet

- Final Accounts Notes and Numericals 2023 To Be Solved in ClassDocument8 pagesFinal Accounts Notes and Numericals 2023 To Be Solved in ClassDishuNo ratings yet

- M3 T5 Financial StatementsDocument15 pagesM3 T5 Financial StatementsPrshnt MishraNo ratings yet

- B203B - Accounting and Finance (Part BDocument32 pagesB203B - Accounting and Finance (Part Bahmed helmyNo ratings yet

- Intriioiiducintrotioniiiiiiiiiiiiiiiiiiiiiiiiiiiiii To Income StatementDocument3 pagesIntriioiiducintrotioniiiiiiiiiiiiiiiiiiiiiiiiiiiiii To Income StatementYashika RanaNo ratings yet

- Trading AccountDocument12 pagesTrading AccountVinay NaikNo ratings yet

- Trading, P & L and BSDocument25 pagesTrading, P & L and BSshreyu14796No ratings yet

- CPA Review Notes 2019 - FAR (Financial Accounting and Reporting)From EverandCPA Review Notes 2019 - FAR (Financial Accounting and Reporting)Rating: 3.5 out of 5 stars3.5/5 (17)

- 0998-483-0847 - 0915-551-0558 C7 Doña Segundina Townhomes, 32 National Road, Brgy. Putatan, Muntinlupa City, Metro Manila Taclindo-385999206Document1 page0998-483-0847 - 0915-551-0558 C7 Doña Segundina Townhomes, 32 National Road, Brgy. Putatan, Muntinlupa City, Metro Manila Taclindo-385999206aishwaryaNo ratings yet

- Alumni FormDocument1 pageAlumni FormaishwaryaNo ratings yet

- Marketing Project Report On Diagnostic Centre in Ahmedabad - 151671194Document106 pagesMarketing Project Report On Diagnostic Centre in Ahmedabad - 151671194aishwarya100% (3)

- Amity Fee 25-07-2017Document1 pageAmity Fee 25-07-2017aishwaryaNo ratings yet

- Document and Communicate ResponsibilitiesDocument3 pagesDocument and Communicate ResponsibilitiesaishwaryaNo ratings yet

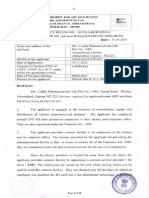

- 12 V671 - Cadila Pharmaceutic Aar-Bn-511381 GSTDocument12 pages12 V671 - Cadila Pharmaceutic Aar-Bn-511381 GSTVivek SharmaNo ratings yet

- Form 11Document44 pagesForm 11gilbert.belciugNo ratings yet

- Cash Flow ProjectionsDocument36 pagesCash Flow ProjectionsJoy FaruzNo ratings yet

- Sap Withholding Tax Configuration Tds GuideDocument28 pagesSap Withholding Tax Configuration Tds Guidevenkat62990% (1)

- Manila Cavite Laguna Cebu Cagayan de Oro DavaoDocument8 pagesManila Cavite Laguna Cebu Cagayan de Oro DavaoRaymond RosalesNo ratings yet

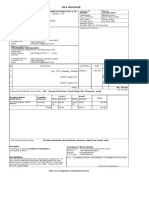

- Tax Invoice: Payment Terms: Installation AddressDocument1 pageTax Invoice: Payment Terms: Installation Address18-UPH-046 JEROME DANISH JNo ratings yet

- XLS EngDocument3 pagesXLS EngmonemNo ratings yet

- 2022 Tax TableDocument3 pages2022 Tax TableDiwakar reddyNo ratings yet

- Solved John and Marsha Are Married and Filed A Joint ReturnDocument1 pageSolved John and Marsha Are Married and Filed A Joint ReturnAnbu jaromiaNo ratings yet

- 2012 ITAD - BIR - Ruling - No. - 092 1220210505 11 1ig3ujmDocument4 pages2012 ITAD - BIR - Ruling - No. - 092 1220210505 11 1ig3ujmrian.lee.b.tiangcoNo ratings yet

- EB No. 2489Document4 pagesEB No. 2489jamNo ratings yet

- PdataDocument6 pagesPdataRazor11111No ratings yet

- Referencer - 6th CPC - SCPC - Sixth Central Pay Commission - Pay Calculator NewDocument6 pagesReferencer - 6th CPC - SCPC - Sixth Central Pay Commission - Pay Calculator News.k. nemaNo ratings yet

- Models of GSTDocument16 pagesModels of GSTGs AbhilashNo ratings yet

- Od 329974507178165100Document1 pageOd 329974507178165100aadarshishita2407No ratings yet

- Indian Income Tax Return Acknowledgement 2021-22: Assessment YearDocument1 pageIndian Income Tax Return Acknowledgement 2021-22: Assessment YearNarayan KumbharNo ratings yet

- Boldfit Shoe BagDocument1 pageBoldfit Shoe BagSundeep ChebroluNo ratings yet

- Return Note - BRH12188307Document1 pageReturn Note - BRH12188307JamesNo ratings yet

- LLQP Quick FormulasDocument2 pagesLLQP Quick FormulasRenato PuentesNo ratings yet

- Budget Budget Budget 2021-22 2021-22 2021-22 Union Union UnionDocument52 pagesBudget Budget Budget 2021-22 2021-22 2021-22 Union Union Unionkunal rajputNo ratings yet

- CIR v. MirantDocument7 pagesCIR v. MirantPaul Joshua SubaNo ratings yet

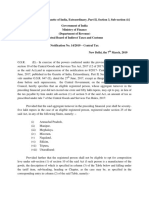

- Notfctn 14 Central Tax English 2019Document2 pagesNotfctn 14 Central Tax English 2019sathishmrNo ratings yet

- Bill NarzoDocument1 pageBill Narzomunnu2461No ratings yet

- Blinkit-Offer Letter-Yashas Nag. U!-SignedDocument2 pagesBlinkit-Offer Letter-Yashas Nag. U!-Signedvijaybhaskar damireddy100% (1)

- Only Invoice No MismatchedDocument49 pagesOnly Invoice No Mismatchedshubhamburnwal213No ratings yet

- Question 1: Ias 8 Policies, Estimates & Errors: Page 1 of 3Document3 pagesQuestion 1: Ias 8 Policies, Estimates & Errors: Page 1 of 3Bagudu Bilal GamboNo ratings yet

- Project On Capital GainsDocument14 pagesProject On Capital Gainsanuragsingh55No ratings yet

- Taxation Notes - DimaampaoDocument115 pagesTaxation Notes - DimaampaoNLainie OmarNo ratings yet

- Suggested Answers in Taxation Law Bar Examinations 1994 2006 PDFDocument86 pagesSuggested Answers in Taxation Law Bar Examinations 1994 2006 PDFGregorio AustralNo ratings yet

- Presumptive Input Tax-4% of Gross Value: He Will Be Allowed An Input Tax On His Inventory On The Transition DateDocument5 pagesPresumptive Input Tax-4% of Gross Value: He Will Be Allowed An Input Tax On His Inventory On The Transition DateLala AlalNo ratings yet