You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Central Bank Communication in The Financial CrisisDocument16 pagesCentral Bank Communication in The Financial CrisisDeepan Kumar DasNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- US-Mexico Economic RelationsDocument41 pagesUS-Mexico Economic RelationsDeepan Kumar DasNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- US-Mexico Economic RelationsDocument41 pagesUS-Mexico Economic RelationsDeepan Kumar DasNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- SharatChandra Rachanabali 3229pages Indexed 7.5MB PDF PanjabiwalaDocument3,229 pagesSharatChandra Rachanabali 3229pages Indexed 7.5MB PDF PanjabiwalaRana GhoshNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Central Bank Intervention and Exchange Rate VolatilityDocument23 pagesCentral Bank Intervention and Exchange Rate VolatilityDeepan Kumar DasNo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Effectiveness of Exchange Rate Communication and InterventionsDocument22 pagesEffectiveness of Exchange Rate Communication and InterventionsDeepan Kumar DasNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Drivers Handbook Study GuideDocument42 pagesDrivers Handbook Study GuideDeepan Kumar DasNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Macro News and Exchange Rates in BRICSDocument4 pagesMacro News and Exchange Rates in BRICSDeepan Kumar DasNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- A Commentary On Publish or Perish CultureDocument3 pagesA Commentary On Publish or Perish CultureDeepan Kumar DasNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Presentation Style Report: Submitted byDocument4 pagesPresentation Style Report: Submitted byDeepan Kumar DasNo ratings yet

- FRM Exam Calculator Guide FAQ 2018Document5 pagesFRM Exam Calculator Guide FAQ 2018Deepan Kumar DasNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Ba Ii Plus en PDFDocument115 pagesBa Ii Plus en PDFJudeNo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Descriptive Statistics of Selected Financials of The North American CompaniesDocument12 pagesDescriptive Statistics of Selected Financials of The North American CompaniesDeepan Kumar DasNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Publish or Perish Culture - Bane or Boon For Academic LifeDocument9 pagesPublish or Perish Culture - Bane or Boon For Academic LifeDeepan Kumar DasNo ratings yet

- Investment Analysis and Portfolio ManagementDocument102 pagesInvestment Analysis and Portfolio ManagementPankaj Bhasin88% (8)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Practice TestDocument1 pagePractice TestDeepan Kumar DasNo ratings yet

- The Effects of Shifts in A Return Distribution On Optimal PortfoliosDocument33 pagesThe Effects of Shifts in A Return Distribution On Optimal PortfoliosDeepan Kumar DasNo ratings yet

- Predicting Returns With Financial RatiosDocument30 pagesPredicting Returns With Financial RatiosDeepan Kumar DasNo ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Testing Portfolio Efficiency With Conditioning InformationDocument26 pagesTesting Portfolio Efficiency With Conditioning InformationDeepan Kumar DasNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- NCFM Module - 1 Financial Markets: A Beginner's Module by Wahid311Document93 pagesNCFM Module - 1 Financial Markets: A Beginner's Module by Wahid311Abdul Wahid KhanNo ratings yet

- Chandana DebnathDocument45 pagesChandana DebnathDeepan Kumar DasNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Commodities MKT ModuleDocument154 pagesCommodities MKT ModulecasachinNo ratings yet

- SharatChandra Rachanabali 3229pages Indexed 7.5MB PDF PanjabiwalaDocument3,229 pagesSharatChandra Rachanabali 3229pages Indexed 7.5MB PDF PanjabiwalaRana GhoshNo ratings yet

- International Credential GuidebookDocument86 pagesInternational Credential GuidebookDeepan Kumar DasNo ratings yet

- The Loyalty That The Youths of Dhaka Have Toward Their Mobile OperatorsDocument28 pagesThe Loyalty That The Youths of Dhaka Have Toward Their Mobile OperatorsDeepan Kumar DasNo ratings yet

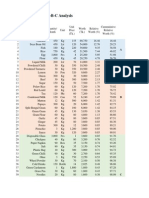

- ABC AnalysisDocument2 pagesABC AnalysisDeepan Kumar DasNo ratings yet

- An Overview of Financial System in BangladeshDocument4 pagesAn Overview of Financial System in BangladeshDeepan Kumar DasNo ratings yet

- Banglalink E-Tyaka ( - )Document13 pagesBanglalink E-Tyaka ( - )Deepan Kumar DasNo ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Isbf - Investment WorkbookDocument5 pagesIsbf - Investment WorkbookDeepan Kumar DasNo ratings yet

- User's Manual For SPC XLDocument104 pagesUser's Manual For SPC XLGlenn PeirisNo ratings yet

- Data Analysis and Decision Making PDFDocument97 pagesData Analysis and Decision Making PDFNaseer AhmadNo ratings yet

- Chapter 08 PowerPointDocument18 pagesChapter 08 PowerPointBondzanNo ratings yet

- Statistical Methods For Scientific Research Trainning Module1Document257 pagesStatistical Methods For Scientific Research Trainning Module1Ayalew Demek50% (2)

- Vibrations From Blasting For A Road Tunnel in Hong Kong - A Statistical Review - FINAL - PUBLISHED - VERSIONDocument18 pagesVibrations From Blasting For A Road Tunnel in Hong Kong - A Statistical Review - FINAL - PUBLISHED - VERSIONKristian Murfitt100% (1)

- Problems: MN) MNDocument11 pagesProblems: MN) MNNouran YNo ratings yet

- Sign Test Activity WorksheetDocument2 pagesSign Test Activity WorksheetGhalia DoshanNo ratings yet

- VaR Estimation Using GANs - 1553122463Document23 pagesVaR Estimation Using GANs - 1553122463StepanKalikaNo ratings yet

- A Guard-Band Strategy For Managing False Accept RiskDocument11 pagesA Guard-Band Strategy For Managing False Accept RiskcleitonmoyaNo ratings yet

- Mba-1-Sem-Business-Statistics-Mba-Aktu-Previous Year PaperDocument6 pagesMba-1-Sem-Business-Statistics-Mba-Aktu-Previous Year PaperNishant TripathiNo ratings yet

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Unit-3 The Geometric Distribution: Dr. Rupal C. Shroff 1Document18 pagesUnit-3 The Geometric Distribution: Dr. Rupal C. Shroff 1arnav deshpandeNo ratings yet

- PartialDocument3 pagesPartialFahma AmindaniarNo ratings yet

- 10th International Probabilistic WorkshopDocument398 pages10th International Probabilistic WorkshopHem MotraNo ratings yet

- A Primer On Strong Vs Weak Control of Familywise Error Rate: Michael A. Proschan Erica H. BrittainDocument7 pagesA Primer On Strong Vs Weak Control of Familywise Error Rate: Michael A. Proschan Erica H. BrittainjaczekNo ratings yet

- Unit 3 - Activity 15 - Excel Using Statistics Functions WorksheetDocument9 pagesUnit 3 - Activity 15 - Excel Using Statistics Functions WorksheetNidhi VyasNo ratings yet

- Coefficient of DeterminationDocument8 pagesCoefficient of DeterminationPremlata NaoremNo ratings yet

- Machine Learning (PG) : Assignment 2Document2 pagesMachine Learning (PG) : Assignment 2Arnav YadavNo ratings yet

- MIT18 05S14 Exam Final SolDocument11 pagesMIT18 05S14 Exam Final SolErwin Dave M. DahaoNo ratings yet

- Stat 250 Gunderson Lecture Notes Relationships Between Categorical Variables 12: Chi Square AnalysisDocument17 pagesStat 250 Gunderson Lecture Notes Relationships Between Categorical Variables 12: Chi Square AnalysisDuckieNo ratings yet

- Multivariate Analysis - MANOVADocument7 pagesMultivariate Analysis - MANOVAPhenda Uka UcinkkNo ratings yet

- 5 Tests of Significance SeemaDocument8 pages5 Tests of Significance SeemaFinance dmsrdeNo ratings yet

- Consequences of MulticollinearityDocument2 pagesConsequences of MulticollinearityYee Ting Ng100% (2)

- Michael J Panik - Regression Modeling - Methods, Theory, and Computation With SAS-CRC Press (2009)Document806 pagesMichael J Panik - Regression Modeling - Methods, Theory, and Computation With SAS-CRC Press (2009)NADASHREE BOSE 2248138No ratings yet

- Chapter 5 CORRELATION AND REGRESSIONDocument28 pagesChapter 5 CORRELATION AND REGRESSIONWerty Gigz DurendezNo ratings yet

- BinomialDocument6 pagesBinomialPaula De Las AlasNo ratings yet

- ECON 136 - Final ExamDocument2 pagesECON 136 - Final ExamPenny TratiaNo ratings yet

- Population Mean Hypothesis Testing For Large Samples: Exercise 1Document12 pagesPopulation Mean Hypothesis Testing For Large Samples: Exercise 1rgerergNo ratings yet

- ECON4150 - Introductory Econometrics Lecture 1: Introduction and Review of StatisticsDocument41 pagesECON4150 - Introductory Econometrics Lecture 1: Introduction and Review of StatisticsMwimbaNo ratings yet

- Pengaruh Alat Penyajian Disposableterhadap Sisa Makanan Pasien Di Ruang Rawat Inap Rsup Dr. Kariadi SemarangDocument9 pagesPengaruh Alat Penyajian Disposableterhadap Sisa Makanan Pasien Di Ruang Rawat Inap Rsup Dr. Kariadi SemarangPutri Wahidatul HasanaNo ratings yet

- Taller y No QuizDocument17 pagesTaller y No QuizFabian Ricardo VargasNo ratings yet