You might also like

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- HRM Project ON A COMPANYDocument12 pagesHRM Project ON A COMPANYprernashukla100% (3)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Standard Bank: Miss. Nthabiseng Rebecca LetabolaDocument9 pagesStandard Bank: Miss. Nthabiseng Rebecca LetabolaMpho100% (1)

- Ebay Order Baterias 9V - Edenorte-FusionadoDocument4 pagesEbay Order Baterias 9V - Edenorte-FusionadoYamilka MedranoNo ratings yet

- Aaca Receivables and Sales ReviewerDocument13 pagesAaca Receivables and Sales ReviewerLiberty NovaNo ratings yet

- WB 2 PDFDocument4 pagesWB 2 PDFAnnie LamNo ratings yet

- Presentation of SapmDocument17 pagesPresentation of Sapmneetz13No ratings yet

- Mutual FundDocument38 pagesMutual Fundneetz13No ratings yet

- Wipro Technologies LimitedDocument10 pagesWipro Technologies Limitedneetz13No ratings yet

- BLL15 - Holder in Due Course and Protection To Bankers, CrossingDocument5 pagesBLL15 - Holder in Due Course and Protection To Bankers, Crossingsvm kishore100% (1)

- Chapter 16 International Trade Finance: Multinational Business Finance, 14e (Eiteman)Document20 pagesChapter 16 International Trade Finance: Multinational Business Finance, 14e (Eiteman)EnciciNo ratings yet

- Model Questions BBM Third Semester Business Finance - 2 PDFDocument4 pagesModel Questions BBM Third Semester Business Finance - 2 PDFKusum GopalNo ratings yet

- Account Statement: Description DateDocument11 pagesAccount Statement: Description DateBoni MondalNo ratings yet

- All Forms For SHGDocument23 pagesAll Forms For SHGSurbhi SinghNo ratings yet

- PT Kmdi QQ PT Roz Voz Auta Palembang-Pekanbaru 24 November 2022Document1 pagePT Kmdi QQ PT Roz Voz Auta Palembang-Pekanbaru 24 November 2022337Corp -HardCORENo ratings yet

- NIC Group PLC Audited Financial Results For The Period Ended 31st December 2017Document3 pagesNIC Group PLC Audited Financial Results For The Period Ended 31st December 2017Anonymous KAIoUxP7No ratings yet

- AFAR 3 AnswersDocument5 pagesAFAR 3 AnswersTyrelle Dela CruzNo ratings yet

- Credit Rating: Need, Process and LimitationsDocument24 pagesCredit Rating: Need, Process and LimitationsRupam Aryan BorahNo ratings yet

- HDFC Life Insurance Ltd. Co.: Fundamental & Technical Analysis OF "HOSPITALITY SECTOR (Mid-Cap) "Document68 pagesHDFC Life Insurance Ltd. Co.: Fundamental & Technical Analysis OF "HOSPITALITY SECTOR (Mid-Cap) "Shubham SuryavanshiNo ratings yet

- Client Assistance ScheduleDocument9 pagesClient Assistance SchedulesefanitNo ratings yet

- Soal Dan Jawaban Advance 2Document6 pagesSoal Dan Jawaban Advance 2nicholas adityaNo ratings yet

- Lesson 5 - Basic Financial Accounting & Reporting: Lesson 5 - 1 Recording Business TransactionsDocument7 pagesLesson 5 - Basic Financial Accounting & Reporting: Lesson 5 - 1 Recording Business TransactionsJulliene Sanchez DamianNo ratings yet

- University of The Punjab: Challan/PV NoDocument1 pageUniversity of The Punjab: Challan/PV NoUmer ShahzadNo ratings yet

- Jilsha K GeorgeDocument93 pagesJilsha K Georgeanjanava222No ratings yet

- Migrations: Financial ServicesDocument31 pagesMigrations: Financial ServicesSachin PoojaryNo ratings yet

- PNB Doctor - S DelightDocument18 pagesPNB Doctor - S DelightNishesh KumarNo ratings yet

- Group 7:: Abhishek Goyal Dhanashree Baxy Ipshita Ghosh Puja Priya Shivam Pandey Vidhi KothariDocument26 pagesGroup 7:: Abhishek Goyal Dhanashree Baxy Ipshita Ghosh Puja Priya Shivam Pandey Vidhi KothariABHISHEK GOYALNo ratings yet

- Upper Tamakoshi Hydropower ProjectDocument5 pagesUpper Tamakoshi Hydropower ProjectShreya ChitrakarNo ratings yet

- UEU Manajemen Keuangan Pertemuan 3Document51 pagesUEU Manajemen Keuangan Pertemuan 3HendriMaulanaNo ratings yet

- Accounting Policies, Changes in Accounting Estimates and ErrorsDocument32 pagesAccounting Policies, Changes in Accounting Estimates and ErrorsAmrita TamangNo ratings yet

- ONYXX Investment Unlocking The Future Scott TwyfordDocument2 pagesONYXX Investment Unlocking The Future Scott Twyfordscott3952No ratings yet

- Activity 1.3 - Think Like An AuditorDocument2 pagesActivity 1.3 - Think Like An AuditorIan Christian Alangilan BarrugaNo ratings yet

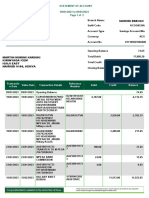

- Martin Murimi KariukiDocument2 pagesMartin Murimi KariukiKameneja LeeNo ratings yet

- Bank Mandiri (Persero) TBK.: Company Report: July 2014 As of 25 July 2014Document3 pagesBank Mandiri (Persero) TBK.: Company Report: July 2014 As of 25 July 2014davidwijaya1986No ratings yet

- MTH 154-Preview - Final ExamDocument5 pagesMTH 154-Preview - Final Exampro mansaNo ratings yet