You might also like

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Responsibility CenterDocument32 pagesResponsibility CenterNeneng WulandariNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Stocks and Their Valuation: Taufikur@ugm - Ac.idDocument43 pagesStocks and Their Valuation: Taufikur@ugm - Ac.idNeneng Wulandari100% (1)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Options and Corporate Finance: Basic ConceptsDocument68 pagesOptions and Corporate Finance: Basic ConceptsNeneng WulandariNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- CH 9 Bond and Their ValuationDocument40 pagesCH 9 Bond and Their ValuationNeneng WulandariNo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Mergers and Acquisitions: Rights Reserved. Mcgraw-Hill/IrwinDocument23 pagesMergers and Acquisitions: Rights Reserved. Mcgraw-Hill/Irwinkkn35No ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- AML Sesi 6Document3 pagesAML Sesi 6Neneng WulandariNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Strengthening A Company'S Competitive Position: Strategic Moves, Timing, and Scope of OperationsDocument16 pagesStrengthening A Company'S Competitive Position: Strategic Moves, Timing, and Scope of OperationsNeneng WulandariNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Strategies For Competing in International Markets: Student VersionDocument15 pagesStrategies For Competing in International Markets: Student VersionNeneng WulandariNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Penentuan Dan Peramalan Nilai TukarDocument4 pagesPenentuan Dan Peramalan Nilai TukarNeneng WulandariNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Transaction ExposureDocument13 pagesTransaction ExposureNeneng WulandariNo ratings yet

- ch30 M&ADocument32 pagesch30 M&ANeneng WulandariNo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Cost of Capital: Taufikur@ugm - Ac.idDocument31 pagesThe Cost of Capital: Taufikur@ugm - Ac.idNeneng WulandariNo ratings yet

- Audit PrinciplesDocument34 pagesAudit PrinciplesJhayanti Nithyananda KalyaniNo ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Transaction ExposureDocument13 pagesTransaction ExposureNeneng WulandariNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Management Accounting: Student EditionDocument28 pagesManagement Accounting: Student EditionNeneng WulandariNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

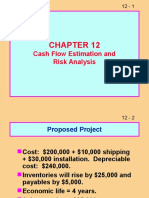

- CH 12 Cash Flow Estimatision and Risk AnalysisDocument39 pagesCH 12 Cash Flow Estimatision and Risk AnalysisNeneng WulandariNo ratings yet

- Book 1 BelajarDocument1 pageBook 1 BelajarNeneng WulandariNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Management Accounting: Student EditionDocument27 pagesManagement Accounting: Student EditionNeneng WulandariNo ratings yet

- Responsibility CenterDocument32 pagesResponsibility CenterNeneng WulandariNo ratings yet

- Management Accounting: Student EditionDocument24 pagesManagement Accounting: Student EditionNeneng WulandariNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- MAHM8e Chapter03.Ab - AzDocument27 pagesMAHM8e Chapter03.Ab - AzDinda OktavianiNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Managerial Accounting: Student EditionDocument21 pagesManagerial Accounting: Student EditionNeneng WulandariNo ratings yet

- 1 Effect of Governance On Credit DecitionsDocument21 pages1 Effect of Governance On Credit DecitionsANISANo ratings yet

- HTTP Tugas EnronDocument1 pageHTTP Tugas EnronNeneng WulandariNo ratings yet

- Test Bank - Chapter 2 Cost ConceptsDocument36 pagesTest Bank - Chapter 2 Cost ConceptsAiko E. Lara71% (7)

- Market Structure - Powerpoint1Document22 pagesMarket Structure - Powerpoint1Nessa MarasiganNo ratings yet

- CCIDocument2 pagesCCIAshutosh MishraNo ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Employee's Role in Service DeliveryDocument36 pagesEmployee's Role in Service DeliverySharath Hn100% (3)

- Sarfraz BDocument25 pagesSarfraz BSarfraz FrazNo ratings yet

- FCF Ch10 Excel Master StudentDocument32 pagesFCF Ch10 Excel Master StudentTosa EndrawanNo ratings yet

- Gujarat Electricity Regulatory Commission: Truing Up For FY 2018-19 and Determination of Tariff For FY 2020-21Document85 pagesGujarat Electricity Regulatory Commission: Truing Up For FY 2018-19 and Determination of Tariff For FY 2020-21Kamalesh BhargavNo ratings yet

- Chapter 22 NotesDocument5 pagesChapter 22 NotesQuintin Jerome BellNo ratings yet

- Grade 8 CommerceDocument4 pagesGrade 8 CommerceKavinda JayasingheNo ratings yet

- Gurgaon Brokers DataDocument11 pagesGurgaon Brokers DataAnuj DulloNo ratings yet

- Marketing Strategy: Assignment-1Document3 pagesMarketing Strategy: Assignment-1Susmita KayalNo ratings yet

- Incomplete Record - QuestionDocument4 pagesIncomplete Record - QuestionChandran Pachapan100% (3)

- Soumik Ghosh Roy Internship PresentationDocument9 pagesSoumik Ghosh Roy Internship PresentationSOUMIK GHOSH ROYNo ratings yet

- Financial and Managerial Accounting The Basis For Business Decisions 18th Edition Williams Solutions ManualDocument87 pagesFinancial and Managerial Accounting The Basis For Business Decisions 18th Edition Williams Solutions ManualEmilyJonesizjgp100% (17)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- DLF Group StrategyDocument15 pagesDLF Group Strategyblackberry7100g100% (1)

- Bharat Heavy Electricals LimitedDocument3 pagesBharat Heavy Electricals LimitedShafeeq KadevalappilNo ratings yet

- Experiential Learning Proposal SampleDocument6 pagesExperiential Learning Proposal SampleDaniel KarthikNo ratings yet

- Excel For MyobDocument4 pagesExcel For MyobargarinirizqiayuNo ratings yet

- Tugas Man PemasaranDocument36 pagesTugas Man Pemasaranmalik abdul aziz100% (1)

- Strategies For Retail Marketing: Dr. P.Suguna, Dr.V.B.MathipooraniDocument9 pagesStrategies For Retail Marketing: Dr. P.Suguna, Dr.V.B.MathipooraniMahima GuptaNo ratings yet

- Just in Time and TQMDocument8 pagesJust in Time and TQMBhramadhathNo ratings yet

- VenumDocument13 pagesVenumMatthias RinguetNo ratings yet

- Product and CostDocument49 pagesProduct and CostSahilNo ratings yet

- 07 08 Group - 8 - Assignment - Job - Order - CostingDocument1 page07 08 Group - 8 - Assignment - Job - Order - CostingNaurah Atika DinaNo ratings yet

- BOS Unit 2 - Forms of Business OrganisationDocument20 pagesBOS Unit 2 - Forms of Business OrganisationShubham PujariNo ratings yet

- Ms Quiz 2 Bsact Sir DDocument5 pagesMs Quiz 2 Bsact Sir DJustin Miguel IniegoNo ratings yet

- CZAR FARMS IAM EnhancementDocument23 pagesCZAR FARMS IAM EnhancementAbdulsalam ZainabNo ratings yet

- BAB 28 Pengangguran Dan InflasiDocument98 pagesBAB 28 Pengangguran Dan InflasiPutri Shery yulianiNo ratings yet

- Sales and Marketing ProfessionalDocument3 pagesSales and Marketing Professionalapi-78851785No ratings yet

- BBA SyllabusDocument47 pagesBBA SyllabusJoice FrancisNo ratings yet