You might also like

- All You Need to Know About Payday LoansFrom EverandAll You Need to Know About Payday LoansRating: 5 out of 5 stars5/5 (1)

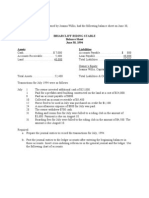

- Cash Flow ProblemsDocument6 pagesCash Flow Problemsvkbm42No ratings yet

- Montealto FinMan Chapter910Document7 pagesMontealto FinMan Chapter910Rey HandumonNo ratings yet

- Fund - Finance - Lecture 2 - Time Value of Money - 2011Document101 pagesFund - Finance - Lecture 2 - Time Value of Money - 2011lucipigNo ratings yet

- Guide to Modern Personal Finance: For Students and Young Adults: Guide to Modern Personal Finance, #1From EverandGuide to Modern Personal Finance: For Students and Young Adults: Guide to Modern Personal Finance, #1No ratings yet

- Forex Trading Tutorial PDFDocument75 pagesForex Trading Tutorial PDFneeds tripathiNo ratings yet

- Slide 3 - Retail Banking OperationsDocument73 pagesSlide 3 - Retail Banking OperationsRashi JainNo ratings yet

- Oil Palm Vca (Mindanao Cluster)Document79 pagesOil Palm Vca (Mindanao Cluster)DBSKfangirlNo ratings yet

- Process of Retail LendingDocument26 pagesProcess of Retail Lendingkaren sunil100% (1)

- Module 2 Solution Manual-2 PDFDocument41 pagesModule 2 Solution Manual-2 PDFMarvin MarianoNo ratings yet

- Banking Industry INDIANDocument26 pagesBanking Industry INDIANektapatelbmsNo ratings yet

- Aids To TradeDocument24 pagesAids To TradeVivek Shaw86% (14)

- Running Head: A Financial Forecast For New World Chemicals IncDocument9 pagesRunning Head: A Financial Forecast For New World Chemicals IncTimNo ratings yet

- Bilant LB Engleza Model 2003Document5 pagesBilant LB Engleza Model 2003Monica FrangetiNo ratings yet

- Retail Banking - IcicibankDocument69 pagesRetail Banking - IcicibankKaataRanjithkumarNo ratings yet

- Chapter 11 PDFDocument57 pagesChapter 11 PDFswapnil kaleNo ratings yet

- Consumer FinanceDocument24 pagesConsumer FinanceAdityaNo ratings yet

- Intermediary Services: Consumer Finance, Credit / Debit CardsDocument88 pagesIntermediary Services: Consumer Finance, Credit / Debit CardsAditya SawantNo ratings yet

- 5.tnasdc DBF Paper IV Module B Unit 9Document12 pages5.tnasdc DBF Paper IV Module B Unit 9dhanushtrack3No ratings yet

- EPM-3.1 Performance Evaluation of BanksDocument19 pagesEPM-3.1 Performance Evaluation of BanksSandeep Sonawane100% (1)

- Banking Assignment FinalDocument12 pagesBanking Assignment FinalNazmul HaqueNo ratings yet

- Prepared by PC15MBA-034: Basanti BagDocument23 pagesPrepared by PC15MBA-034: Basanti BagSusilPandaNo ratings yet

- CUBDocument22 pagesCUBsathishNo ratings yet

- Khalid RR1814B29 PFP 2NDDocument8 pagesKhalid RR1814B29 PFP 2NDRR1814B29No ratings yet

- RB Chapter 3 - Savings BankDocument10 pagesRB Chapter 3 - Savings BankHarish YadavNo ratings yet

- BankingDocument18 pagesBankingpiyush_ckNo ratings yet

- Banking Products & Operations: Session 7Document34 pagesBanking Products & Operations: Session 7Vaidyanathan RavichandranNo ratings yet

- Interim Report - Madhuti Saha - 211190Document7 pagesInterim Report - Madhuti Saha - 211190Soumiya BishtNo ratings yet

- 10 - AKPKs Workplace Financial Education ServicesDocument29 pages10 - AKPKs Workplace Financial Education ServicesLawrence KhohNo ratings yet

- Customer Satisfaction On Housing Loan in SBI BankDocument23 pagesCustomer Satisfaction On Housing Loan in SBI BankDebjyoti Rakshit100% (2)

- Sources of Funds Liabilities ManagementDocument22 pagesSources of Funds Liabilities ManagementAMukherjeeNo ratings yet

- Account Opening DepartmentDocument24 pagesAccount Opening DepartmentSarfraz AliNo ratings yet

- Retail BankingDocument25 pagesRetail BankingTrusha Hodiwala80% (5)

- Idbi Loan ProductsDocument23 pagesIdbi Loan ProductsHemantHembromNo ratings yet

- MicrofinanceDocument27 pagesMicrofinancevchouha9993No ratings yet

- OM v1.1Document34 pagesOM v1.1Madhav MishraNo ratings yet

- UNITIIDocument66 pagesUNITIIlokesh palNo ratings yet

- Final Presentation On: Presented To: Sir Ejaz MustafaDocument59 pagesFinal Presentation On: Presented To: Sir Ejaz Mustafashehzaib sunnyNo ratings yet

- Wholesale and Retail BankingDocument24 pagesWholesale and Retail BankingNazmul H. PalashNo ratings yet

- "Standared Chartered Bank LTD.": Performance Evaluation ofDocument32 pages"Standared Chartered Bank LTD.": Performance Evaluation ofjahid262No ratings yet

- Credit Mandiri BankDocument8 pagesCredit Mandiri BankVie ViEnNo ratings yet

- By R.Dinesh Kumar: Submitted To The Department ofDocument77 pagesBy R.Dinesh Kumar: Submitted To The Department ofDrRashmiranjan PanigrahiNo ratings yet

- Marketing Analysis of DBBL in BangladeshDocument40 pagesMarketing Analysis of DBBL in BangladeshAftab UddinNo ratings yet

- Comparative Analysis of Home Loan in UTI BankDocument95 pagesComparative Analysis of Home Loan in UTI BankMitesh SonegaraNo ratings yet

- Education Loan: Submitted To:-Mr. SusheelDocument21 pagesEducation Loan: Submitted To:-Mr. SusheelakbarreadsNo ratings yet

- Unit 4 Credit - For WEBSITEDocument46 pagesUnit 4 Credit - For WEBSITEASHISH KUMARNo ratings yet

- Session - 8 - 9 Retail Asset ProductsDocument11 pagesSession - 8 - 9 Retail Asset ProductsLagishetty AbhiramNo ratings yet

- Pratul C Lobo - MMS Marketing - Need Analysis of Auto Loan Customers - ICICI BankDocument51 pagesPratul C Lobo - MMS Marketing - Need Analysis of Auto Loan Customers - ICICI Bankankit0225No ratings yet

- Final B-307 SlidesDocument33 pagesFinal B-307 SlidesAftab UddinNo ratings yet

- Saving Account GeneralDocument6 pagesSaving Account GeneralDurgeshNo ratings yet

- Questionnaire Auto Loan CustomersDocument51 pagesQuestionnaire Auto Loan Customerssarvesh.bharti71% (7)

- Rationale of The Study: Chapter: OneDocument22 pagesRationale of The Study: Chapter: OneHumayun KabirNo ratings yet

- RBI Guidelines For Licensing of Small Finance Bank RBI Guidelines For Licensing of Payments BankDocument35 pagesRBI Guidelines For Licensing of Small Finance Bank RBI Guidelines For Licensing of Payments BankNovi KapoorNo ratings yet

- Banking: Presented by Mukundan SDocument31 pagesBanking: Presented by Mukundan SRajalingam100% (1)

- Financial InclusionDocument425 pagesFinancial InclusionNishad ThakurNo ratings yet

- Developing Products For Rural Markets: Annie Duflo Centre For Micro Finance at IFMR February 14, 2007Document57 pagesDeveloping Products For Rural Markets: Annie Duflo Centre For Micro Finance at IFMR February 14, 2007sharmi8No ratings yet

- Consumer Credit: Advantages, Disadvantages, Sources, and CostsDocument46 pagesConsumer Credit: Advantages, Disadvantages, Sources, and CostsAvi ThakurNo ratings yet

- Retail BankingDocument6 pagesRetail Bankingtejasvgahlot05No ratings yet

- Banking Products and Operations: Ravi For IBADocument33 pagesBanking Products and Operations: Ravi For IBAVaidyanathan RavichandranNo ratings yet

- 7 P's of IciciDocument8 pages7 P's of IciciNikhil ChaturvediNo ratings yet

- Co-Operative and Commercial Banks in IndiaDocument44 pagesCo-Operative and Commercial Banks in IndiaLove PreetNo ratings yet

- 7 P's of Marketing For ICICI BANKDocument8 pages7 P's of Marketing For ICICI BANKIshan Vyas60% (5)

- Banking N Session-4 & 5Document49 pagesBanking N Session-4 & 5Vaibhav AggarwalNo ratings yet

- 7 P S of Marketing For ICICI BANKDocument10 pages7 P S of Marketing For ICICI BANK007chetanNo ratings yet

- Raj UCO SynopsisDocument9 pagesRaj UCO SynopsisRaj Kamal100% (1)

- Ee Announcement Presentation FinalDocument31 pagesEe Announcement Presentation Finalkoundi_3No ratings yet

- Manage Work Priorities and Professional LevelDocument6 pagesManage Work Priorities and Professional Levelparul sharmaNo ratings yet

- Question No. 1 Is Compulsory. Attempt Any Four Questions From The Remaining Five Questions. Working Notes Should Form Part of The AnswerDocument15 pagesQuestion No. 1 Is Compulsory. Attempt Any Four Questions From The Remaining Five Questions. Working Notes Should Form Part of The Answerritz meshNo ratings yet

- Business Breif U06-2 PDFDocument1 pageBusiness Breif U06-2 PDFAdam MichałekNo ratings yet

- Present Worth Analysis: Engineering Economy With AccountingDocument21 pagesPresent Worth Analysis: Engineering Economy With AccountingCamilo Dela Cruz Jr.No ratings yet

- Annual Report 2018 2019Document272 pagesAnnual Report 2018 2019Nishita AkterNo ratings yet

- 2012 Annual ReportDocument108 pages2012 Annual ReportphuawlNo ratings yet

- Fiscal PlanningDocument3 pagesFiscal PlanningmalleshNo ratings yet

- MAN385.23 - Entrepreneurial Management - Graebner - 04470Document15 pagesMAN385.23 - Entrepreneurial Management - Graebner - 04470Dimitra TaslimNo ratings yet

- Chapter 3Document59 pagesChapter 3Lakachew GetasewNo ratings yet

- Certificate of Employers ' Liability Insurance (A)Document1 pageCertificate of Employers ' Liability Insurance (A)Vincent JohnNo ratings yet

- Shell Dividend PolicyDocument4 pagesShell Dividend PolicyAdrian SaputraNo ratings yet

- Ineffective Institutional Investors LawDocument19 pagesIneffective Institutional Investors LawJustin HalimNo ratings yet

- Business English VocabDocument18 pagesBusiness English VocabAnna100% (1)

- Shivam Popat CBMR SAPM RetailDocument4 pagesShivam Popat CBMR SAPM Retailshivampopat7658No ratings yet

- Taxguru - In-All About DEFERRED TAX and Its Entry in BooksDocument8 pagesTaxguru - In-All About DEFERRED TAX and Its Entry in Bookskumar45caNo ratings yet

- 22 31MR53Document10 pages22 31MR53overqualifiedNo ratings yet

- Project Report On Mutual Funds in IndiaDocument43 pagesProject Report On Mutual Funds in Indiapednekar_madhuraNo ratings yet

- Advance Test Schedule CS Executive Dec-23Document22 pagesAdvance Test Schedule CS Executive Dec-23Gungun ChetaniNo ratings yet

- Assignment 1Document6 pagesAssignment 1Haider Chelsea KhanNo ratings yet

- A Note On Tax ResearchDocument4 pagesA Note On Tax ResearchLeonel FerreiraNo ratings yet