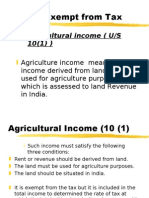

You might also like

- 11.tax Free Incomes FinalDocument40 pages11.tax Free Incomes FinalGhs ShahpurkandiNo ratings yet

- Module-1: Basic Concepts and DefinitionsDocument35 pagesModule-1: Basic Concepts and Definitions2VX20BA091No ratings yet

- Chapter - 1: Page - 1Document7 pagesChapter - 1: Page - 1Arunangsu ChandaNo ratings yet

- 11.tax Free Incomes FinalDocument38 pages11.tax Free Incomes FinalshineNo ratings yet

- Non Taxable Income, Income From Salary and Income From HPDocument35 pagesNon Taxable Income, Income From Salary and Income From HPAnonymous ckTjn7RCq8No ratings yet

- Non Taxable IncomeDocument35 pagesNon Taxable IncomeGayatri RaneNo ratings yet

- IT-03 Incomes Exempt From TaxDocument18 pagesIT-03 Incomes Exempt From TaxAkshat GoyalNo ratings yet

- 11.tax Free Incomes FinalDocument40 pages11.tax Free Incomes FinalKARTHIK ANo ratings yet

- 11.tax Free Incomes FinalDocument42 pages11.tax Free Incomes FinalAmit PandeyNo ratings yet

- Income Exempt From TaxDocument20 pagesIncome Exempt From TaxSaad AliNo ratings yet

- Tax Exemptions Under Section 10Document22 pagesTax Exemptions Under Section 10AnshuNo ratings yet

- Section-10: Income Exempt From TaxDocument21 pagesSection-10: Income Exempt From TaxJitendra VernekarNo ratings yet

- Section Eligible Assessee Type of Income Limits Conditions For Claiming ExemptionDocument32 pagesSection Eligible Assessee Type of Income Limits Conditions For Claiming ExemptionanilpeddamalliNo ratings yet

- Income ExemptDocument21 pagesIncome Exemptapi-3832224100% (1)

- Section-10: Income Exempt From TaxDocument21 pagesSection-10: Income Exempt From TaxRakesh SharmaNo ratings yet

- TaxDocument11 pagesTaxDilkash WaraichNo ratings yet

- Tax-Free Incomes ExplainedDocument37 pagesTax-Free Incomes ExplainedsaandoNo ratings yet

- 11 TaxDocument37 pages11 TaxArpita KapoorNo ratings yet

- MF0003 - Taxation ManagementDocument7 pagesMF0003 - Taxation ManagementushasnNo ratings yet

- Tax Free IncomesDocument45 pagesTax Free IncomesAayush GiriNo ratings yet

- Chinmayanand DTDocument5 pagesChinmayanand DTAnand PandeyNo ratings yet

- 11.tax Free Incomes FinalDocument45 pages11.tax Free Incomes FinalAyushi DixitNo ratings yet

- As Amended by Finance Act, 2017Document3 pagesAs Amended by Finance Act, 2017JonnyNo ratings yet

- 11.tax Free Incomes FinalDocument35 pages11.tax Free Incomes Finalpraveenr5883No ratings yet

- Income ExemptDocument25 pagesIncome Exemptapi-3832224No ratings yet

- Incomes Exempt Under Section 10Document10 pagesIncomes Exempt Under Section 10Rahul TiwariNo ratings yet

- Wa0004.Document64 pagesWa0004.dhruv MehtaNo ratings yet

- VND Openxmlformats-Officedocument WordprocessingmlDocument25 pagesVND Openxmlformats-Officedocument WordprocessingmlHimanshu RajputNo ratings yet

- Income Tax Law BasicsDocument44 pagesIncome Tax Law BasicsAbhishek BhatiaNo ratings yet

- Income from Other Sources SummaryDocument24 pagesIncome from Other Sources Summarynikhilk222No ratings yet

- A Book: Integrated Professional Competency Course (IPCC) Paper - 1: AccountingDocument12 pagesA Book: Integrated Professional Competency Course (IPCC) Paper - 1: AccountingSipoy SatishNo ratings yet

- 11.tax Free Incomes FinalDocument29 pages11.tax Free Incomes FinalRaun JainNo ratings yet

- Unit 4Document14 pagesUnit 4Rupesh PatilNo ratings yet

- Income From Other SourcesDocument12 pagesIncome From Other Sourcessanjul2008No ratings yet

- Incomes Which Do Not Form OF Total Income (Section 10) : Dr. P.Sree Sudha, Associate Professor, DsnluDocument48 pagesIncomes Which Do Not Form OF Total Income (Section 10) : Dr. P.Sree Sudha, Associate Professor, Dsnluleela naga janaki rajitha attiliNo ratings yet

- Chapter - 5 - TaxDocument15 pagesChapter - 5 - TaxAshek AHmedNo ratings yet

- Module - 1 Basic Concepts.Document11 pagesModule - 1 Basic Concepts.Dimple JainNo ratings yet

- What Is Section 10 of The Income Tax ActDocument15 pagesWhat Is Section 10 of The Income Tax Actdevam05006No ratings yet

- Taxs Law ExamDocument15 pagesTaxs Law ExamSaif AliNo ratings yet

- Name: Mohd - AqibDocument29 pagesName: Mohd - AqibMohd AqibNo ratings yet

- Articleship Exam QuestionsDocument33 pagesArticleship Exam QuestionsVarshiniNo ratings yet

- Gross Income Inc Exc DedDocument9 pagesGross Income Inc Exc DedMelbert BallaraNo ratings yet

- General Deductions (Under Section 80) : Basic Rules Governing Deductions Under Sections 80C To 80UDocument67 pagesGeneral Deductions (Under Section 80) : Basic Rules Governing Deductions Under Sections 80C To 80UVENKATESAN DNo ratings yet

- The Income Tax ActDocument8 pagesThe Income Tax ActChakshuBehlNo ratings yet

- Exemptions Deductions Assessment: Principles of Taxation Income Tax Act 1961Document24 pagesExemptions Deductions Assessment: Principles of Taxation Income Tax Act 1961Presidency UniversityNo ratings yet

- Study Note - 13: Incomes Which Do Not Form Part of Total IncomeDocument37 pagesStudy Note - 13: Incomes Which Do Not Form Part of Total Incomes4sahithNo ratings yet

- 11.tax Free Incomes FinalDocument48 pages11.tax Free Incomes FinalaeeciviltrNo ratings yet

- Exempted Incomes Section 10Document24 pagesExempted Incomes Section 10jerin joshy100% (1)

- Direct Tax SLE-1 Roll No KSPMCAA012 Dev Shah Mcom Part 1 Sem 3 2022-2023 Exemption Under Sec 10Document20 pagesDirect Tax SLE-1 Roll No KSPMCAA012 Dev Shah Mcom Part 1 Sem 3 2022-2023 Exemption Under Sec 10Dev ShahNo ratings yet

- Midterm Reviewer - Taxation Key ConceptsDocument5 pagesMidterm Reviewer - Taxation Key ConceptsMaria RochelleNo ratings yet

- Union Budget 2013-14 - Highlights of Direct Tax ProposalsDocument5 pagesUnion Budget 2013-14 - Highlights of Direct Tax Proposalsankit403No ratings yet

- TaxationDocument13 pagesTaxationAubrey LegaspiNo ratings yet

- Income Tax Tables for Individuals and CorporationsDocument9 pagesIncome Tax Tables for Individuals and Corporationshaze_toledo5077No ratings yet

- In Come Tax TableDocument9 pagesIn Come Tax TablejorjirubiNo ratings yet

- Income Exempted From Tax: Provident Fund (Sec. 10 (11) )Document1 pageIncome Exempted From Tax: Provident Fund (Sec. 10 (11) )Shinam JainNo ratings yet

- CHAPTER 4 Part 1Document21 pagesCHAPTER 4 Part 1assadrafaqNo ratings yet

- Army Institute of Law: Concept of Income and Total IncomeDocument17 pagesArmy Institute of Law: Concept of Income and Total IncomeMehr MunjalNo ratings yet

- Section 10 of The Income Tax ActDocument10 pagesSection 10 of The Income Tax ActVANSHIKA SINGHNo ratings yet

- Calculating Net Taxable Salary IncomeDocument6 pagesCalculating Net Taxable Salary IncomeShital PujaraNo ratings yet

- BIO DATA. FinalDocument2 pagesBIO DATA. FinalmanikaNo ratings yet

- Haryana Public Service Commission: Bays No 1-10, Block-B, Sector - 4, PanchkulaDocument19 pagesHaryana Public Service Commission: Bays No 1-10, Block-B, Sector - 4, PanchkulaJohn WickNo ratings yet

- Suruchi Bansal Bio DataDocument2 pagesSuruchi Bansal Bio DatamanikaNo ratings yet

- The Reserve Bank of India Is The Central Bank Which Was Established On The RecommendationDocument3 pagesThe Reserve Bank of India Is The Central Bank Which Was Established On The RecommendationmanikaNo ratings yet

- Vinay Pathak and His Wife VDocument2 pagesVinay Pathak and His Wife Vmanika67% (3)

- BIO DATA. FinalDocument2 pagesBIO DATA. FinalmanikaNo ratings yet

- SonakshiJain BiodataDocument2 pagesSonakshiJain BiodatamanikaNo ratings yet

- What Is A Bank ? IntroductionDocument7 pagesWhat Is A Bank ? IntroductionmanikaNo ratings yet

- Patent NotesDocument9 pagesPatent NotesmanikaNo ratings yet

- Imp BriefDocument10 pagesImp BriefmanikaNo ratings yet

- The Punjab Land Revenue ActDocument65 pagesThe Punjab Land Revenue ActHumayoun Ahmad FarooqiNo ratings yet

- Trademark Registration Process and Its EffectsDocument10 pagesTrademark Registration Process and Its EffectsAllen Jones100% (1)

- Trademark Law Basics- Rights, Functions & RegistrationDocument10 pagesTrademark Law Basics- Rights, Functions & RegistrationmanikaNo ratings yet

- Role of Banking in Eco DevelopmentDocument4 pagesRole of Banking in Eco DevelopmentmanikaNo ratings yet

- Advantages of GSTDocument8 pagesAdvantages of GSTmanikaNo ratings yet

- Tax Law NotesDocument85 pagesTax Law NotesmanikaNo ratings yet

- Caste As Racial DiscriminationDocument4 pagesCaste As Racial DiscriminationmanikaNo ratings yet

- Human Rights Notes NewDocument12 pagesHuman Rights Notes NewAayushNo ratings yet

- Tax Law Final NotesDocument32 pagesTax Law Final NotesmanikaNo ratings yet

- Appeals Proceedings and Revision Under Income Tax ActDocument8 pagesAppeals Proceedings and Revision Under Income Tax ActmanikaNo ratings yet

- Unit - 1 - Introduction To Human RightsDocument23 pagesUnit - 1 - Introduction To Human RightsjeganrajrajNo ratings yet

- RELIGION - (ICCPR) A.18 - Freedom of Thought, Conscience, Religion-Subject To Public Safety, OrderDocument6 pagesRELIGION - (ICCPR) A.18 - Freedom of Thought, Conscience, Religion-Subject To Public Safety, OrdermanikaNo ratings yet

- Human Rights Chapter SummaryDocument28 pagesHuman Rights Chapter Summaryflippchick100% (15)

- Advantages of GSTDocument8 pagesAdvantages of GSTmanikaNo ratings yet

- Human Rights AssignmentDocument5 pagesHuman Rights AssignmentmanikaNo ratings yet

- Caste As Racial DiscriminationDocument7 pagesCaste As Racial DiscriminationmanikaNo ratings yet

- Caste As Racial DiscriminationDocument4 pagesCaste As Racial DiscriminationmanikaNo ratings yet

- Human Rights AssignmentDocument5 pagesHuman Rights AssignmentmanikaNo ratings yet

- Scanned With CamscannerDocument14 pagesScanned With CamscannermanikaNo ratings yet

- Draft Offer Letter PAS 4Document12 pagesDraft Offer Letter PAS 4binodgstpNo ratings yet

- The Nature and Importance of Economics: Prof. Dang Gannaban CASDocument43 pagesThe Nature and Importance of Economics: Prof. Dang Gannaban CASCindy JavaNo ratings yet

- Adjusting Journal EntriesDocument11 pagesAdjusting Journal EntriesKatrina RomasantaNo ratings yet

- Preliminary Topic Five - Financial MarketsDocument12 pagesPreliminary Topic Five - Financial MarketsBaro LeeNo ratings yet

- Perbandingan Kinerja Keuangan Perusahaan Manufaktur Menggunakan Analisis Rasio KeuanganDocument22 pagesPerbandingan Kinerja Keuangan Perusahaan Manufaktur Menggunakan Analisis Rasio KeuanganIrma Retno DewiNo ratings yet

- The Future of Marine Engine Remote Monitoring in Marine ApplicationsDocument8 pagesThe Future of Marine Engine Remote Monitoring in Marine ApplicationsMakis MathsNo ratings yet

- Al-Fayed Goes Out in Style As Harrods Leaps 40 Per Cent: FinanceDocument4 pagesAl-Fayed Goes Out in Style As Harrods Leaps 40 Per Cent: FinanceDuyên Võ ThịNo ratings yet

- Reyes vs. National Housing Authority Case Digest Full TextDocument10 pagesReyes vs. National Housing Authority Case Digest Full TextgielNo ratings yet

- For Each Question 23 - 30, Mark One Letter (A, B or C) For The Correct Answer. - You Will Hear The Conversation TwiceDocument2 pagesFor Each Question 23 - 30, Mark One Letter (A, B or C) For The Correct Answer. - You Will Hear The Conversation TwiceMa Emilia100% (1)

- (English) Accounting Basics Explained Through A Story (DownSub - Com)Document8 pages(English) Accounting Basics Explained Through A Story (DownSub - Com)Kenneth MallariNo ratings yet

- Understanding The 3 Financial Statements 1653805473Document11 pagesUnderstanding The 3 Financial Statements 1653805473RaikhanNo ratings yet

- (SpringerBriefs in Economics) Ashima Goyal (Auth.) - History of Monetary Policy in India Since Independence-Springer India (2014)Document89 pages(SpringerBriefs in Economics) Ashima Goyal (Auth.) - History of Monetary Policy in India Since Independence-Springer India (2014)Dinesh MahapatraNo ratings yet

- Tax Cases SummaryDocument10 pagesTax Cases SummaryBikoy EstoqueNo ratings yet

- David Aaker Be PDFDocument8 pagesDavid Aaker Be PDFPreeti BajajNo ratings yet

- 2018 TranscriptsDocument316 pages2018 TranscriptsOnePunchManNo ratings yet

- PWC Indonesia-Oil-And-Gas-Guide-2016 PDFDocument172 pagesPWC Indonesia-Oil-And-Gas-Guide-2016 PDFberiawiekeNo ratings yet

- Carson ExplanationDocument16 pagesCarson ExplanationlambertwatchNo ratings yet

- Bloomberg ExcelDocument52 pagesBloomberg Exceldbjn100% (2)

- Citi BankDocument40 pagesCiti BankZeeshan Mobeen100% (1)

- Britannia Industries: PrintDocument1 pageBritannia Industries: PrintTejaswiniNo ratings yet

- Rbi ThesisDocument51 pagesRbi ThesisAnil Anayath100% (8)

- U.S. Workers Most Productive Due to Longer Hours Worked AnnuallyDocument13 pagesU.S. Workers Most Productive Due to Longer Hours Worked AnnuallyShakil MimNo ratings yet

- F9FM-Session10 d08vzzxDocument26 pagesF9FM-Session10 d08vzzxErclanNo ratings yet

- Stress Testing For Bangladesh Private Commercial BanksDocument11 pagesStress Testing For Bangladesh Private Commercial Banksrubayee100% (1)

- Tri Level 2 Promo 17Document5 pagesTri Level 2 Promo 17asdfafNo ratings yet

- Chapter 12 Solution of Fundamental of Financial Accouting by EDMONDS (4th Edition)Document67 pagesChapter 12 Solution of Fundamental of Financial Accouting by EDMONDS (4th Edition)Awais AzeemiNo ratings yet

- Presentation - Payment BanksDocument14 pagesPresentation - Payment BanksAstral HeightsNo ratings yet

- International Capital Budgeting: Dr. Ch. Venkata Krishna Reddy Associate ProfessorDocument39 pagesInternational Capital Budgeting: Dr. Ch. Venkata Krishna Reddy Associate Professorkrishna reddyNo ratings yet

- FDI 2022 - enDocument244 pagesFDI 2022 - enBekele Guta GemeneNo ratings yet

- Financial Markets Notes for ExamsDocument10 pagesFinancial Markets Notes for ExamsAadeesh JainNo ratings yet