You might also like

- Building Multi-Tier Web Applications in Virtual EnvironmentsDocument30 pagesBuilding Multi-Tier Web Applications in Virtual Environmentsssregens82No ratings yet

- Lussier 3 Ech 05Document50 pagesLussier 3 Ech 05ssregens82No ratings yet

- Orchestro State Inventory Management 2015Document8 pagesOrchestro State Inventory Management 2015ssregens82No ratings yet

- Judicial Power of Supreme CourtDocument2 pagesJudicial Power of Supreme Courtssregens82No ratings yet

- Risk and Rates of Return: Learning ObjectivesDocument36 pagesRisk and Rates of Return: Learning Objectivesssregens82No ratings yet

- Supplier General QualificationsDocument3 pagesSupplier General Qualificationsssregens82No ratings yet

- CHP 3Document2 pagesCHP 3ssregens82No ratings yet

- Problems, Problem Spaces and Search: Dr. Suthikshn KumarDocument47 pagesProblems, Problem Spaces and Search: Dr. Suthikshn Kumarssregens82No ratings yet

- Chapter 1 BowersoxDocument38 pagesChapter 1 Bowersoxssregens82100% (1)

- Static Picture Effects For Powerpoint Slides: Reproductio N Instructions Printing Instructions Removing InstructionsDocument17 pagesStatic Picture Effects For Powerpoint Slides: Reproductio N Instructions Printing Instructions Removing Instructionsssregens82No ratings yet

- Week 8 AssignmentDocument5 pagesWeek 8 Assignmentssregens82100% (2)

- Transportation and Logistics OptimizationDocument18 pagesTransportation and Logistics Optimizationssregens82No ratings yet

- Process StepsDocument1 pageProcess Stepsssregens82No ratings yet

- Time Value PracticeDocument1 pageTime Value Practicessregens82No ratings yet

- Vcost DemoDocument2 pagesVcost Demossregens82No ratings yet

- AMIS 525 Pop Quiz - Chapters 22 and 23Document5 pagesAMIS 525 Pop Quiz - Chapters 22 and 23ssregens82No ratings yet

- V Ac - SC V (Aa Ar) - (Sa SR) V (Aa Ar) - (Aa SR) + (Aa SR) - (Sa SR) V ( (Aa Ar) - (Aa SR) ) + ( (Aa SR) - (Sa SR) )Document1 pageV Ac - SC V (Aa Ar) - (Sa SR) V (Aa Ar) - (Aa SR) + (Aa SR) - (Sa SR) V ( (Aa Ar) - (Aa SR) ) + ( (Aa SR) - (Sa SR) )ssregens82No ratings yet

- Regular Flow Irregular Flow Irregular Flow DepreciationDocument1 pageRegular Flow Irregular Flow Irregular Flow Depreciationssregens82No ratings yet

- TPRICEDocument1 pageTPRICEssregens82No ratings yet

- Signs For Income VarianceDocument1 pageSigns For Income Variancessregens82No ratings yet

- Ri RoiDocument1 pageRi Roissregens82No ratings yet

- I (P Q) - (V Q) - F: The Fundamental EquationDocument1 pageI (P Q) - (V Q) - F: The Fundamental Equationssregens82No ratings yet

- Percent DoneDocument1 pagePercent Donessregens82No ratings yet

- Total For 5 Years Each YearDocument1 pageTotal For 5 Years Each Yearssregens82No ratings yet

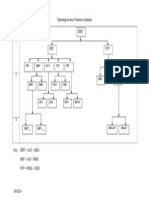

- Operating Income Variances DiagramDocument1 pageOperating Income Variances Diagramssregens82No ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Banker's Secret To Creating Wealth!Document3 pagesBanker's Secret To Creating Wealth!pbowen22375% (4)

- Pas 1: Presentation of Financial StatementsDocument9 pagesPas 1: Presentation of Financial StatementsJung Jeon0% (1)

- Case DigestDocument7 pagesCase DigestYolanda Janice Sayan FalingaoNo ratings yet

- Train LawDocument3 pagesTrain LawRONNEL SECADRONNo ratings yet

- Actionable ClaimDocument17 pagesActionable ClaimKrishna100% (2)

- Guaranty and Suretyship SummaryDocument12 pagesGuaranty and Suretyship SummaryBenn DegusmanNo ratings yet

- House Rent Agreement NewDocument2 pagesHouse Rent Agreement NewPrarthana Mohapatra100% (1)

- SARFAESI (Central Registry) Amendment Rules, 2016Document6 pagesSARFAESI (Central Registry) Amendment Rules, 2016Latest Laws Team100% (1)

- FORM16 CLTDocument4 pagesFORM16 CLTrajeevNo ratings yet

- 1CO1900A0903Document1 page1CO1900A0903jotham_sederstr7655No ratings yet

- Department of Labor: 96 22717Document11 pagesDepartment of Labor: 96 22717USA_DepartmentOfLaborNo ratings yet

- Banking The Customer Experience Dividend PDFDocument32 pagesBanking The Customer Experience Dividend PDFAlex DincoviciNo ratings yet

- BOE Bonded TemplateDocument2 pagesBOE Bonded TemplateSuzanne Cristantiello100% (6)

- AKPF Fast Facts PDFDocument2 pagesAKPF Fast Facts PDFBernard Vincent Guitan MineroNo ratings yet

- Special Power of Attorney - PagibigDocument2 pagesSpecial Power of Attorney - PagibigKenneth Peter Molave100% (1)

- RESPA Letter To GreentreeDocument19 pagesRESPA Letter To GreentreeMark R.No ratings yet

- LICDocument39 pagesLICPrathamesh Wakade50% (2)

- Chapter 5 Time Value of Money Multiple Choice Questions PDFDocument36 pagesChapter 5 Time Value of Money Multiple Choice Questions PDFImran Zulfiqar100% (3)

- Ratio AnalysisDocument8 pagesRatio AnalysisPrakash ChandraNo ratings yet

- Lapulapu V CA (Digested)Document1 pageLapulapu V CA (Digested)Eds GalinatoNo ratings yet

- Indian Banking StructureDocument5 pagesIndian Banking StructureKarthik NadarNo ratings yet

- The Indian Weekender, Friday, February 7, 2020 Volume 11 Issue 45Document31 pagesThe Indian Weekender, Friday, February 7, 2020 Volume 11 Issue 45Indian WeekenderNo ratings yet

- Rose Packing v. CADocument3 pagesRose Packing v. CAJustin MoretoNo ratings yet

- Chapter 1Document10 pagesChapter 1arsykeiwayNo ratings yet

- Reflective Writing For Mortgage ProjectDocument2 pagesReflective Writing For Mortgage Projectapi-302548391No ratings yet

- A Study On Cooperative Banks in India With Special Reference To Lending PracticesDocument6 pagesA Study On Cooperative Banks in India With Special Reference To Lending PracticesSrikara Acharya100% (1)

- Course Outline PDFDocument5 pagesCourse Outline PDFMuhammad AsadNo ratings yet

- Ligj Nr. 34, Dt. 17.6.2019 Ligji I Ri - EN (1) OkDocument15 pagesLigj Nr. 34, Dt. 17.6.2019 Ligji I Ri - EN (1) OkEgiNo ratings yet

- 3 Mendoza Vs ReyesDocument16 pages3 Mendoza Vs ReyesEMNo ratings yet

- Group Assignment-Land Law.Document7 pagesGroup Assignment-Land Law.Tiffany NkhomaNo ratings yet