You might also like

- Resources Understanding ISO20022 NACHA Payments 2013Document121 pagesResources Understanding ISO20022 NACHA Payments 2013Rajendra PilludaNo ratings yet

- Steps in Registering Your Business in The PhilippinesDocument7 pagesSteps in Registering Your Business in The PhilippinesJonas Celiz DatorNo ratings yet

- Introduction To International TradeDocument46 pagesIntroduction To International TradeBalasingam PrahalathanNo ratings yet

- Multinational CorporationsDocument43 pagesMultinational CorporationsBalasingam PrahalathanNo ratings yet

- Multinational CorporationsDocument43 pagesMultinational CorporationsBalasingam PrahalathanNo ratings yet

- 8.foreign Direct Investment and Foreign AidDocument7 pages8.foreign Direct Investment and Foreign AidBalasingam PrahalathanNo ratings yet

- Open Item Management in SapDocument17 pagesOpen Item Management in SapSwatantra BarikNo ratings yet

- The Functional Microfinance Bank: Strategies for SurvivalFrom EverandThe Functional Microfinance Bank: Strategies for SurvivalNo ratings yet

- Reward Current Account 31 March 2022 To 30 April 2022: Your Account Arranged Overdraft Limit 1,000Document4 pagesReward Current Account 31 March 2022 To 30 April 2022: Your Account Arranged Overdraft Limit 1,000ITNo ratings yet

- Your RBC Personal Banking Account StatementDocument2 pagesYour RBC Personal Banking Account Statementdrgt ggNo ratings yet

- Micro-Finance Management & Critical Analysis in IndiaDocument72 pagesMicro-Finance Management & Critical Analysis in IndiaAtul MangaleNo ratings yet

- Microfinance (D)Document75 pagesMicrofinance (D)smithNo ratings yet

- Micro-Financing and the Economic Health of a NationFrom EverandMicro-Financing and the Economic Health of a NationNo ratings yet

- Notes On Insurance - Rene Callanta Insurance Code: (P.D. 1460, As Amended)Document22 pagesNotes On Insurance - Rene Callanta Insurance Code: (P.D. 1460, As Amended)Cervus Augustiniana LexNo ratings yet

- History of Microfinance in NigeriaDocument9 pagesHistory of Microfinance in Nigeriahardmanperson100% (1)

- Overview of Micro FinanceDocument9 pagesOverview of Micro FinanceRafiuddin BiplabNo ratings yet

- MeralcoDocument2 pagesMeralcoTheo Amadeus100% (4)

- Sbi PDFDocument4 pagesSbi PDFMufaddal RashidNo ratings yet

- MicrofinanceDocument58 pagesMicrofinanceSamuel Davis100% (1)

- Deed of Agreement Standby Letter of Credit (SBLC) : Private & ConfidentialDocument46 pagesDeed of Agreement Standby Letter of Credit (SBLC) : Private & ConfidentialSumantriNo ratings yet

- Report On Micro FinanceDocument55 pagesReport On Micro FinanceSudeepti TanejaNo ratings yet

- Confessions of a Microfinance Heretic: How Microlending Lost Its Way and Betrayed the PoorFrom EverandConfessions of a Microfinance Heretic: How Microlending Lost Its Way and Betrayed the PoorRating: 3.5 out of 5 stars3.5/5 (5)

- MicrofinanceDocument57 pagesMicrofinancepallavi gurav100% (1)

- Motion For Satisfaction of JudgmentDocument19 pagesMotion For Satisfaction of JudgmentBarry EskanosNo ratings yet

- MicrofinanceDocument6 pagesMicrofinanceyasirseyyid100% (1)

- Chapter 1Document44 pagesChapter 1suraj BanavalkarNo ratings yet

- Unit One Microfinance OverviewDocument15 pagesUnit One Microfinance OverviewCome-all NathNo ratings yet

- Assignment of Financial InstitutionDocument9 pagesAssignment of Financial InstitutionKamalpreet_Mad_6500No ratings yet

- Empowering Women Through MicrofinancingDocument81 pagesEmpowering Women Through MicrofinancingSuraj DubeyNo ratings yet

- Synopsis Micro FinaceDocument10 pagesSynopsis Micro Finacearoranitin35No ratings yet

- Unit 3 Micro FinanceDocument6 pagesUnit 3 Micro FinanceDeveshi JhawarNo ratings yet

- FN212 Topic 1Document23 pagesFN212 Topic 1rajabushabani321No ratings yet

- Microfinance Principles and PracticeDocument17 pagesMicrofinance Principles and Practicejamesamani2001No ratings yet

- Topic: Financial Inclusion, Micro Finance and Micro InsuranceDocument14 pagesTopic: Financial Inclusion, Micro Finance and Micro InsuranceBalendu BhagatNo ratings yet

- NavdeepDocument18 pagesNavdeepArshdeep SinghNo ratings yet

- Notes On MicrofinanceDocument8 pagesNotes On MicrofinanceMapuia Lal Pachuau100% (2)

- Problem Identification and Objective of The ReportDocument33 pagesProblem Identification and Objective of The ReportGhazal AijazNo ratings yet

- Microfinance 8431683779625937Document25 pagesMicrofinance 8431683779625937AR47No ratings yet

- Micro-Finance/credit Institution: Its Principles, and Relevance in Liberia's Post-War ReconstructionDocument9 pagesMicro-Finance/credit Institution: Its Principles, and Relevance in Liberia's Post-War ReconstructionGleh Huston Appleton100% (4)

- MICROFINANCEDocument35 pagesMICROFINANCEChinmayee ParhiNo ratings yet

- Chapter 1 NotesDocument15 pagesChapter 1 Notesthete.ashishNo ratings yet

- 1 What Is MicrofinanceDocument39 pages1 What Is MicrofinanceAbhishek GargNo ratings yet

- Vikas ProjectDocument49 pagesVikas ProjectVinay KhannaNo ratings yet

- Icro Inance S: 6.M F & SHGDocument10 pagesIcro Inance S: 6.M F & SHGYayati DandekarNo ratings yet

- Micro FinanceDocument30 pagesMicro FinanceSakshi BhaskarNo ratings yet

- MICROFINANCEDocument16 pagesMICROFINANCEGulshan JangidNo ratings yet

- 05 Chapter-1 PDFDocument52 pages05 Chapter-1 PDFRohitNo ratings yet

- Microfinance PresentationDocument5 pagesMicrofinance Presentationnidhi1726No ratings yet

- Case Study On MicrofinanceDocument18 pagesCase Study On MicrofinanceTusharika RajpalNo ratings yet

- Microfinance Is The Provision ofDocument13 pagesMicrofinance Is The Provision ofHarnaaz Preet SinghNo ratings yet

- Project Report On "A Critical Analysis of Micro Finance in India"Document55 pagesProject Report On "A Critical Analysis of Micro Finance in India"Om Prakash MishraNo ratings yet

- A. About Microfinance: Microfinance Is A General Term To Describe Financial Services ToDocument32 pagesA. About Microfinance: Microfinance Is A General Term To Describe Financial Services ToAnshul ChawraNo ratings yet

- Micro FinanceDocument12 pagesMicro FinanceBhavya DayalNo ratings yet

- Micro Finance AssDocument24 pagesMicro Finance Assanuradha9787No ratings yet

- MicrofinanceDocument13 pagesMicrofinanceAkshay InamdarNo ratings yet

- Micro Finance - C'se W'KDocument3 pagesMicro Finance - C'se W'KbagumaNo ratings yet

- Micro Finance Ravi Mathur Mms-FinDocument55 pagesMicro Finance Ravi Mathur Mms-FinSwati KakadNo ratings yet

- Chapter 7Document73 pagesChapter 7Magix SmithNo ratings yet

- MicroDocument28 pagesMicro1k12No ratings yet

- Unit 1 Introduction To MicrofinanceDocument10 pagesUnit 1 Introduction To Microfinancejcmxqxz7tcNo ratings yet

- Unit 1Document92 pagesUnit 1Amrit KaurNo ratings yet

- Notes - Unit 2Document10 pagesNotes - Unit 2ishita sabooNo ratings yet

- Microfinance - IntroductionDocument7 pagesMicrofinance - Introductionbeena antuNo ratings yet

- Unit-1 Over View: Microfinance Rural Banking and Development FinanceDocument46 pagesUnit-1 Over View: Microfinance Rural Banking and Development FinanceAMIT SINDHUNo ratings yet

- Microfinance: Microfinance Is The Provision ofDocument13 pagesMicrofinance: Microfinance Is The Provision ofAndrew SitwalaNo ratings yet

- Microfinance and MicrocreditDocument7 pagesMicrofinance and Microcreditsukriti94No ratings yet

- Microfinance: Microfinance Is The Provision of Financial Services To Low-Income ClientsDocument20 pagesMicrofinance: Microfinance Is The Provision of Financial Services To Low-Income ClientsJatinChadhaNo ratings yet

- MICRPFINANCE IN INDIA WordDocument14 pagesMICRPFINANCE IN INDIA WordA08 Ratika KambleNo ratings yet

- Submitted To: Submitted By: Ambuj Gupta Sangram Keshari Panigrahi 2k91/BFS/43Document36 pagesSubmitted To: Submitted By: Ambuj Gupta Sangram Keshari Panigrahi 2k91/BFS/43Sangram PanigrahiNo ratings yet

- Microfinance and Poverty AlleviationDocument27 pagesMicrofinance and Poverty AlleviationIzma HussainNo ratings yet

- Microfinance: Microfinance Refers To The Provision of Financial Services To Low-Income ClientsDocument8 pagesMicrofinance: Microfinance Refers To The Provision of Financial Services To Low-Income ClientsRohan_Kapoor_4806No ratings yet

- CH Allen EgsDocument5 pagesCH Allen EgsY N S Y SNo ratings yet

- How Will The Goal Be Achieved?: MicrocreditDocument4 pagesHow Will The Goal Be Achieved?: MicrocreditthundergssNo ratings yet

- Date: International Learning Institute Assignment On MicrofinanceDocument12 pagesDate: International Learning Institute Assignment On MicrofinanceSubhash SoniNo ratings yet

- Working Capital ManagementDocument10 pagesWorking Capital ManagementBalasingam PrahalathanNo ratings yet

- Com 21034 - Session - 1Document36 pagesCom 21034 - Session - 1Balasingam PrahalathanNo ratings yet

- Session - 4Document27 pagesSession - 4Balasingam PrahalathanNo ratings yet

- Handout 8Document43 pagesHandout 8Balasingam PrahalathanNo ratings yet

- Com 21034 - Session - 1Document36 pagesCom 21034 - Session - 1Balasingam PrahalathanNo ratings yet

- An Empirical Analysis of The Impact of Total Debt On The Economic Growth of Sri LankaDocument31 pagesAn Empirical Analysis of The Impact of Total Debt On The Economic Growth of Sri LankaBalasingam PrahalathanNo ratings yet

- 113 AbbreviationsDocument2 pages113 AbbreviationsBalasingam PrahalathanNo ratings yet

- H - O ModelDocument14 pagesH - O ModelBalasingam PrahalathanNo ratings yet

- Session 5 IDocument17 pagesSession 5 IBalasingam PrahalathanNo ratings yet

- Com 21034 - Session - 1Document36 pagesCom 21034 - Session - 1Balasingam PrahalathanNo ratings yet

- Com 21034 - Session - 1Document36 pagesCom 21034 - Session - 1Balasingam PrahalathanNo ratings yet

- Session 5 IiDocument65 pagesSession 5 IiBalasingam PrahalathanNo ratings yet

- Vision, Mission, Objectives, and Strategy: Session - 02Document67 pagesVision, Mission, Objectives, and Strategy: Session - 02Balasingam PrahalathanNo ratings yet

- Business Information System - 3Document9 pagesBusiness Information System - 3Balasingam PrahalathanNo ratings yet

- Strategic Analysis Evaluating A Company's External EnvironmentDocument27 pagesStrategic Analysis Evaluating A Company's External EnvironmentBalasingam PrahalathanNo ratings yet

- Main Market Forms and Revenue TheoryDocument48 pagesMain Market Forms and Revenue TheoryBalasingam PrahalathanNo ratings yet

- Production - HANDOUTDocument51 pagesProduction - HANDOUTBalasingam PrahalathanNo ratings yet

- 5.matrix AlgebraDocument31 pages5.matrix AlgebraBalasingam PrahalathanNo ratings yet

- Com 21034 - Session - 1Document36 pagesCom 21034 - Session - 1Balasingam PrahalathanNo ratings yet

- Cost of Production/Theory of CostDocument55 pagesCost of Production/Theory of CostBalasingam PrahalathanNo ratings yet

- Business Information SystemDocument10 pagesBusiness Information SystemBalasingam PrahalathanNo ratings yet

- Business Information System - 4Document8 pagesBusiness Information System - 4Balasingam PrahalathanNo ratings yet

- BUSINESS INFORMATION SYSTEM - HandoutDocument37 pagesBUSINESS INFORMATION SYSTEM - HandoutBalasingam PrahalathanNo ratings yet

- Floating (Flexible) Exchange Rate SystemDocument2 pagesFloating (Flexible) Exchange Rate SystemBalasingam PrahalathanNo ratings yet

- Marginal Utility AnalysisDocument47 pagesMarginal Utility AnalysisBalasingam PrahalathanNo ratings yet

- Guidebook To Financing Infrastructure For T&L Within NDDocument241 pagesGuidebook To Financing Infrastructure For T&L Within NDsunitaNo ratings yet

- Gorton and MetrikDocument43 pagesGorton and MetrikJustin EpsteinNo ratings yet

- Partnership Letter Anne 1.6Document4 pagesPartnership Letter Anne 1.6PRIYARATNA JHA100% (1)

- Some Bank Sort Code UpdatedDocument306 pagesSome Bank Sort Code UpdatedpapaskyNo ratings yet

- 104 2018 111 Bdo Usa LLPDocument68 pages104 2018 111 Bdo Usa LLPAdrienne GonzalezNo ratings yet

- Fireman's Fund v. JamillaDocument3 pagesFireman's Fund v. JamillaDominique PobeNo ratings yet

- Synopsis ON "Role and Need of Merchant Bankers in Ipo: M.Rajashekar (REG NO. 11SLCMA104)Document7 pagesSynopsis ON "Role and Need of Merchant Bankers in Ipo: M.Rajashekar (REG NO. 11SLCMA104)shiva7363No ratings yet

- Account Statement-1Document12 pagesAccount Statement-1adithyamukka369No ratings yet

- Registration FormDocument2 pagesRegistration FormBuddhi Bal ChidiNo ratings yet

- Promotion Study Material For BankDocument271 pagesPromotion Study Material For BankJack Meena100% (1)

- NUST Fee Challan Looks LikeDocument1 pageNUST Fee Challan Looks LikeZubair Ali100% (1)

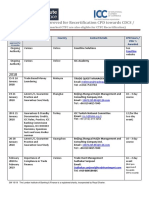

- 2018/19 - Courses Approved For Recertification CPD Towards CDCSDocument29 pages2018/19 - Courses Approved For Recertification CPD Towards CDCSMunshi Masudur RahamanNo ratings yet

- Mee Seva Hand Book Final PDFDocument216 pagesMee Seva Hand Book Final PDFREDDYGAARI ABBAYI0% (1)

- MEMORANDUM D17-1-5: in BriefDocument39 pagesMEMORANDUM D17-1-5: in Briefbiharris22No ratings yet

- Dep33 Aof With IntroDocument2 pagesDep33 Aof With IntroDesikanNo ratings yet

- Exam 2nd Year Without ANSWERDocument7 pagesExam 2nd Year Without ANSWERJohnAllenMarillaNo ratings yet

- Company Isin Description in NSDLDocument156 pagesCompany Isin Description in NSDLDhananjayan Gopinathan0% (1)

- Useful Numbers in BangaloreDocument5 pagesUseful Numbers in BangaloreJohn SavioNo ratings yet

- Account Statement DefinedDocument12 pagesAccount Statement DefinedRahul PambharNo ratings yet

- HDFC Life YoungStar Super Premium (SPL) IllustrationDocument0 pagesHDFC Life YoungStar Super Premium (SPL) IllustrationAnkur MittalNo ratings yet