You might also like

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Li YDocument159 pagesLi YkhandeliavivekNo ratings yet

- Policies 1999 OnwardsDocument19 pagesPolicies 1999 OnwardskhandeliavivekNo ratings yet

- Motive of Holding CashDocument8 pagesMotive of Holding CashkhandeliavivekNo ratings yet

- Role of Financial InstitutionDocument20 pagesRole of Financial InstitutionSheebu ShamimNo ratings yet

- Section 7Document27 pagesSection 7khandeliavivekNo ratings yet

- Correlation: Dibyojyoti BhattacharjeeDocument17 pagesCorrelation: Dibyojyoti BhattacharjeekhandeliavivekNo ratings yet

- To Keep Systematic RecordsDocument1 pageTo Keep Systematic RecordskhandeliavivekNo ratings yet

- Dept. of Business Administration Assam University, SilcharDocument5 pagesDept. of Business Administration Assam University, SilcharkhandeliavivekNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

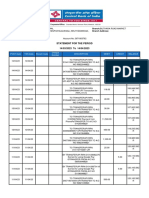

- Statement For The Period 14/03/2023 To 14/04/2023Document6 pagesStatement For The Period 14/03/2023 To 14/04/2023Adrian LamoNo ratings yet

- Lundolm & Sloan. Equity Valuation and Analysis With Eval. 3rd Edition Chp02Document6 pagesLundolm & Sloan. Equity Valuation and Analysis With Eval. 3rd Edition Chp02Peter Pa NNo ratings yet

- 3-Statement Model (Complete)Document16 pages3-Statement Model (Complete)James BondNo ratings yet

- Dividir Las Siguientes Oraciones en Frases y TraducirlasDocument3 pagesDividir Las Siguientes Oraciones en Frases y TraducirlasHoken ProduccionNo ratings yet

- 8b7a06d13b285552e9cf244a44f1537cDocument12 pages8b7a06d13b285552e9cf244a44f1537cTo Vinh BangNo ratings yet

- Resilient PreppingDocument157 pagesResilient PreppingLIBRERIA GRNo ratings yet

- Accounting Concepts and PrinciplesDocument4 pagesAccounting Concepts and PrinciplesJustine VeralloNo ratings yet

- Coca Cola To Produce Paper Bottles British English TeacherDocument9 pagesCoca Cola To Produce Paper Bottles British English TeacherNil SierraNo ratings yet

- Chart Patterns, Trading, and Dan ZangerDocument5 pagesChart Patterns, Trading, and Dan ZangerLNo ratings yet

- BearingDocument3 pagesBearingZul FaijarNo ratings yet

- Q2 Simple InterestDocument3 pagesQ2 Simple InterestElsa Mae NocquiaoNo ratings yet

- How To Fill-Out The AtdDocument1 pageHow To Fill-Out The AtdMa Barbara T AustriaNo ratings yet

- Unit 1 Econ VocabDocument5 pagesUnit 1 Econ VocabNatalia HowardNo ratings yet

- Chapter 9Document7 pagesChapter 9Kotryna RudelytėNo ratings yet

- PPF Excel Calculator Stable InvestorDocument17 pagesPPF Excel Calculator Stable InvestorAayushKumarNo ratings yet

- W-8BEN: Certificate of Foreign Status of Beneficial Owner For United States Tax Withholding and Reporting (Individuals)Document1 pageW-8BEN: Certificate of Foreign Status of Beneficial Owner For United States Tax Withholding and Reporting (Individuals)Adam AkbarNo ratings yet

- Tullow Oil PLC 2020 Annual Report and AccountsDocument158 pagesTullow Oil PLC 2020 Annual Report and Accountsforina harissonNo ratings yet

- International Economics 3rd Edition Feenstra Test BankDocument26 pagesInternational Economics 3rd Edition Feenstra Test BankNicholasSolisdiwex100% (13)

- Zlib - Pub - The Economics of Property and Planning Future ValueDocument231 pagesZlib - Pub - The Economics of Property and Planning Future ValueAinun Devi AlfiaNo ratings yet

- BYJUS Exam Prep IAS Indian Economy 3Document9 pagesBYJUS Exam Prep IAS Indian Economy 3Navish KotwalNo ratings yet

- DIOMIS Romania InfoDocument79 pagesDIOMIS Romania InfoIrina AtudoreiNo ratings yet

- Maximum Social AdvantageDocument18 pagesMaximum Social AdvantageMehak KaushikkNo ratings yet

- Contemporary Financial Management 13th Edition Moyer Test BankDocument25 pagesContemporary Financial Management 13th Edition Moyer Test BankHannahMendozaxznr100% (60)

- Reaction Paper On The Article: DBM Trims Departments' Budget For COVID FundDocument3 pagesReaction Paper On The Article: DBM Trims Departments' Budget For COVID FundMa YaNo ratings yet

- BB 107 Tutorial 5Document4 pagesBB 107 Tutorial 5Frederick Goldwin SoegihartoNo ratings yet

- AFGIS 212 Survival Benefit Claim FormDocument1 pageAFGIS 212 Survival Benefit Claim FormSashank NalluriNo ratings yet

- Balance Sheet Ay 2023-24 Priyanka Gawade..Document5 pagesBalance Sheet Ay 2023-24 Priyanka Gawade..cagopalofficebackupNo ratings yet

- Revenue Recognition - Long-Term Construction Contracts (Part 2)Document6 pagesRevenue Recognition - Long-Term Construction Contracts (Part 2)CaliNo ratings yet

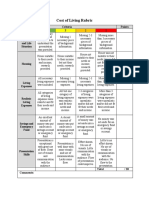

- Cost of Living Rubric - Budget UnitDocument2 pagesCost of Living Rubric - Budget Unitapi-467206648No ratings yet

- Pagibig MDFDocument2 pagesPagibig MDFRalph Andrei CustodioNo ratings yet