You might also like

- Answer Key Chapter 3Document5 pagesAnswer Key Chapter 3Donna Zandueta-TumalaNo ratings yet

- Comparitive Analysis of Certain Sections of Companies Act, 1956 & Companies Act, 2013Document11 pagesComparitive Analysis of Certain Sections of Companies Act, 1956 & Companies Act, 2013MOUSOM ROYNo ratings yet

- National Highway, Songkoy, Kitcharao - Alegria Boundary Agusan Del Norte 8609 - PhilippinesDocument9 pagesNational Highway, Songkoy, Kitcharao - Alegria Boundary Agusan Del Norte 8609 - PhilippinesRODRIGO JR. MADRAZO0% (1)

- Accounting Principle Task 2Document22 pagesAccounting Principle Task 2ryandina octaviana100% (5)

- Letter of GrantDocument3 pagesLetter of GrantAnjali SharmaNo ratings yet

- Vanishing CompaniesDocument7 pagesVanishing CompaniesVinay Artwani100% (1)

- Final Ratlami SevDocument14 pagesFinal Ratlami SevrahulNo ratings yet

- Fema (Foreign Exchange Management ActDocument25 pagesFema (Foreign Exchange Management ActMayank GargNo ratings yet

- SSRN Id2942684 PDFDocument16 pagesSSRN Id2942684 PDFSriNo ratings yet

- Consumer Protection 1Document12 pagesConsumer Protection 1Shailesh KumarNo ratings yet

- PetitionerDocument21 pagesPetitionermohan kumarNo ratings yet

- Project Report TRIPSDocument18 pagesProject Report TRIPSAditya MayekarNo ratings yet

- A Critical Study On Role of Adr in Consumer Protection IndiaDocument13 pagesA Critical Study On Role of Adr in Consumer Protection IndiaRaghav DhootNo ratings yet

- Compendium On Landmark Cases: Trade Mark: AuthorsDocument45 pagesCompendium On Landmark Cases: Trade Mark: AuthorsPrateek Chahar100% (1)

- Competition Law (Final)Document22 pagesCompetition Law (Final)amitbhmcNo ratings yet

- Judicial Intervention in International Arbitration: TH THDocument26 pagesJudicial Intervention in International Arbitration: TH THtayyaba redaNo ratings yet

- Critical Analysis of Judicial Developments in The Realm of Indian ArbitrationDocument11 pagesCritical Analysis of Judicial Developments in The Realm of Indian ArbitrationNAOMI S 2257143No ratings yet

- Evidence ProjectDocument9 pagesEvidence ProjectDaniyal sirajNo ratings yet

- Project DikshaDocument18 pagesProject DikshaSAVINo ratings yet

- Strikes and Lockouts: Presented By: Nikita Begum TalukdarDocument50 pagesStrikes and Lockouts: Presented By: Nikita Begum Talukdarsanjana seth100% (1)

- K&K Screening ExerciseDocument3 pagesK&K Screening ExerciseSakshi PriyaNo ratings yet

- Advertising by Advocates in India: The Right To Advertise Professional EthicsDocument4 pagesAdvertising by Advocates in India: The Right To Advertise Professional EthicsanaNo ratings yet

- Business Law - Competition LawDocument16 pagesBusiness Law - Competition LawJaspreet ChandiNo ratings yet

- Competition Commission of India (CCI)Document27 pagesCompetition Commission of India (CCI)Supriya Pawar100% (1)

- Reasons For LLP Legislation: Vehicle To Professionals and EnterprisesDocument39 pagesReasons For LLP Legislation: Vehicle To Professionals and EnterprisesAnuj SoodNo ratings yet

- What Incomes Are Deemed To Accrue or Arise in India - Varun RajaDocument5 pagesWhat Incomes Are Deemed To Accrue or Arise in India - Varun Rajabakayaro92No ratings yet

- Raghavan Committee ReportDocument13 pagesRaghavan Committee ReportAngel AngelNo ratings yet

- Renusagar Power Co. Limited V. General Electric Co.: Kousini Gupta PRN: 15010324253Document5 pagesRenusagar Power Co. Limited V. General Electric Co.: Kousini Gupta PRN: 15010324253Kousini GuptaNo ratings yet

- MCX Vs NseDocument4 pagesMCX Vs NseRishu SharmaNo ratings yet

- T Infringement by C A: Rademark Omparative Dvertising in IndiaDocument13 pagesT Infringement by C A: Rademark Omparative Dvertising in IndiashiviNo ratings yet

- Manufacturing LawDocument7 pagesManufacturing LawSamay KhobragadeNo ratings yet

- Health Laws - 9th SemesterDocument11 pagesHealth Laws - 9th SemesterRupesh 1312No ratings yet

- Manoj Narula CaseDocument44 pagesManoj Narula CaseSunil beniwal100% (1)

- Real Estate ProjectDocument13 pagesReal Estate ProjectAnkana MukherjeeNo ratings yet

- Article - Entry of Foreign Law Firms in IndiaDocument5 pagesArticle - Entry of Foreign Law Firms in IndiaManish Ojha100% (1)

- Decentralization, Corruption & Social Capital - Sten Widmalm - 2007 PDFDocument232 pagesDecentralization, Corruption & Social Capital - Sten Widmalm - 2007 PDFAji DeniNo ratings yet

- SEBI (Substantial Acquisition of Shares and Takeovers) Regulations, 2011 - Some Key FeaturesDocument6 pagesSEBI (Substantial Acquisition of Shares and Takeovers) Regulations, 2011 - Some Key FeaturesJimlee DasNo ratings yet

- N The Matter ofDocument35 pagesN The Matter ofTulika GuptaNo ratings yet

- Competition Law in IndiaDocument88 pagesCompetition Law in IndiaSomesh KhandelwalNo ratings yet

- Patented Drugs, Counterfeiting Drugs, Spurious Drugs-Under Drug and Cosmetic Act and Impact of World Health Organization - A StudyDocument22 pagesPatented Drugs, Counterfeiting Drugs, Spurious Drugs-Under Drug and Cosmetic Act and Impact of World Health Organization - A StudyJasween GujralNo ratings yet

- Investment and SecuritiesDocument10 pagesInvestment and SecuritiesGaurav Pandey100% (1)

- Vodafone Tax CaseDocument15 pagesVodafone Tax CaseBharti BansalNo ratings yet

- Hidayatullah National Law University Raipur, C.G.: Parody in India-Against Trademark InfringementDocument18 pagesHidayatullah National Law University Raipur, C.G.: Parody in India-Against Trademark InfringementPrashant Paul KerkettaNo ratings yet

- National Law University Odisha: (Semester Vii)Document16 pagesNational Law University Odisha: (Semester Vii)AnanyaSinghalNo ratings yet

- Taxation Assignment: An Overview of Double Taxation Avoidance Agreements: IndiaDocument12 pagesTaxation Assignment: An Overview of Double Taxation Avoidance Agreements: IndiaNasif MustahidNo ratings yet

- CMSR - Case Analysis 22.10.2021Document10 pagesCMSR - Case Analysis 22.10.2021prarthana rameshNo ratings yet

- 10 Kapila Hingorani CaseDocument39 pages10 Kapila Hingorani CaseAshutosh KumarNo ratings yet

- Chapter 4Document123 pagesChapter 4Satyam singhNo ratings yet

- Comparative Advertising in Us Uk IndiaDocument3 pagesComparative Advertising in Us Uk IndiaPriyanshi AgarwalNo ratings yet

- Anti-Dumping Duties: An Assignment OnDocument24 pagesAnti-Dumping Duties: An Assignment OnAshish pariharNo ratings yet

- Advertising by Advocates: Submitted By: Ishan Arora Amity Law School Noida Uttar PradeshDocument27 pagesAdvertising by Advocates: Submitted By: Ishan Arora Amity Law School Noida Uttar Pradeshiarora88No ratings yet

- Labour Law-Roll No. 213112Document20 pagesLabour Law-Roll No. 213112Anita SudalaimaniNo ratings yet

- Role of Courts in ArbitrationDocument19 pagesRole of Courts in Arbitrationjc forlife1No ratings yet

- Trademark, Passsing Off and Reverse Passing Off: A Critical AnalysisDocument7 pagesTrademark, Passsing Off and Reverse Passing Off: A Critical AnalysisShivani ChoudharyNo ratings yet

- 0 - Aditya MNC Assignment PDFDocument22 pages0 - Aditya MNC Assignment PDFAshish pariharNo ratings yet

- Relationship Between A Lawyer & A ClientDocument23 pagesRelationship Between A Lawyer & A ClientSoumya SinhaNo ratings yet

- Damodaram Sanjivayya National Law University Visakhapatnam, A.P., IndiaDocument22 pagesDamodaram Sanjivayya National Law University Visakhapatnam, A.P., IndiaDileep ChowdaryNo ratings yet

- TOPSDocument13 pagesTOPSSumit SinghNo ratings yet

- Competition Law and Pharmaceutical SectorDocument12 pagesCompetition Law and Pharmaceutical SectorChirag shahNo ratings yet

- ITL CompendiumDocument39 pagesITL Compendiumashita AGARWALNo ratings yet

- Maganlal Chhaganlal (P) Ltd. v. Municipal Corpn. of Greater BombayDocument2 pagesMaganlal Chhaganlal (P) Ltd. v. Municipal Corpn. of Greater BombayShivangi BajpaiNo ratings yet

- Comparison - Ratios - Tyre - DistributionDocument15 pagesComparison - Ratios - Tyre - DistributionParehjuiNo ratings yet

- Project Report Printin PressDocument5 pagesProject Report Printin Pressmanohar michaelNo ratings yet

- 2 Financial AnalysisDocument22 pages2 Financial AnalysisAB11A4-Condor, Joana MieNo ratings yet

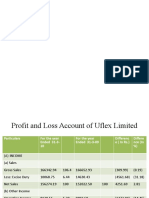

- Friday UFLEXDocument8 pagesFriday UFLEXOnkar TendulkarNo ratings yet

- 330 S12 IndSty MT AMongelluzzoDocument8 pages330 S12 IndSty MT AMongelluzzomongo9279No ratings yet

- Glainier Industríal CorporationDocument43 pagesGlainier Industríal CorporationGraceila CalopeNo ratings yet

- IHCL Corporate PresentationDocument62 pagesIHCL Corporate PresentationAnkitha TheresNo ratings yet

- Bike ExchangeDocument184 pagesBike ExchangeJuan PerezNo ratings yet

- TM 10 - Financial Planning and ForecastingDocument29 pagesTM 10 - Financial Planning and ForecastingTul KuntullNo ratings yet

- Ifrs Edition: Prepared by Coby Harmon University of California, Santa Barbara Westmont CollegeDocument71 pagesIfrs Edition: Prepared by Coby Harmon University of California, Santa Barbara Westmont CollegeRizki NurwikanNo ratings yet

- Long-Term Financial Planning and Growth: Mcgraw-Hill/IrwinDocument23 pagesLong-Term Financial Planning and Growth: Mcgraw-Hill/IrwinMSA-ACCA100% (2)

- Financial Model 1Document1 pageFinancial Model 1ahmedmostafaibrahim22No ratings yet

- Business Plan: Dpb2012 - Entrepreneurship Polytechnic VersionDocument77 pagesBusiness Plan: Dpb2012 - Entrepreneurship Polytechnic VersionKhalique SheikhNo ratings yet

- Mechanics of Break Even AnalysisDocument9 pagesMechanics of Break Even AnalysisGeetanjali BondeNo ratings yet

- Volkswagen 11Document49 pagesVolkswagen 11Frank BessiNo ratings yet

- HMCost2e SM Ch16Document35 pagesHMCost2e SM Ch16monsinNo ratings yet

- Gar34943 ch06 PDFDocument46 pagesGar34943 ch06 PDFbilalNo ratings yet

- MBJ Vol 4 2010Document9 pagesMBJ Vol 4 2010LokuliyanaNNo ratings yet

- Chapter 9 - Marginal - Absorption CostingDocument37 pagesChapter 9 - Marginal - Absorption CostingMaha IqrarNo ratings yet

- 87522Document17 pages87522Kateryna TernovaNo ratings yet

- Financial Accounting-Class 1Document46 pagesFinancial Accounting-Class 1Karen JoyceNo ratings yet

- Return On SalesDocument2 pagesReturn On SalesMa Terresa TejadaNo ratings yet

- Exercises-1-3-1-6-1-7-And-1-15-Managerial AccountingDocument8 pagesExercises-1-3-1-6-1-7-And-1-15-Managerial AccountingPhilip DyNo ratings yet

- Cost II Chap I-1Document52 pagesCost II Chap I-1Etsub SamuelNo ratings yet

- Preparation of FS To Post-Closing TB - Marge Orie Problem SolutionDocument32 pagesPreparation of FS To Post-Closing TB - Marge Orie Problem SolutionAngel Yohaiña Ramos SantiagoNo ratings yet

- Revision Test Paper Cap-Ii: Advanced Accounting Questions Accounting For DepartmentsDocument279 pagesRevision Test Paper Cap-Ii: Advanced Accounting Questions Accounting For Departmentsshankar k.c.No ratings yet

- WarOnWant ZambiaTaxReport WebDocument167 pagesWarOnWant ZambiaTaxReport WebengkjNo ratings yet

- P.G. IV Semester Business Ethics and Corporate Governance Code-MCO-1.4.18Document7 pagesP.G. IV Semester Business Ethics and Corporate Governance Code-MCO-1.4.18Punam GuptaNo ratings yet

- Accounting Principle Weygandt Kieso Kimmel 9thDocument12 pagesAccounting Principle Weygandt Kieso Kimmel 9thMG SHAFEINo ratings yet