You might also like

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Notice of Pre Trial ConferenceDocument2 pagesNotice of Pre Trial Conferencesitty hannan mangotara100% (1)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Hamer v. SidwayDocument3 pagesHamer v. SidwayAnonymous eJBhs9CgNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- Company FNLDocument30 pagesCompany FNLpriyaNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- People of The Philippines Vs - Eddie ManansalaDocument2 pagesPeople of The Philippines Vs - Eddie ManansalaDennis Jay A. Paras100% (2)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- CCXCXCXDocument9 pagesCCXCXCXJeffrey Constantino PatacsilNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Nature and Functions of Bill Of Lading CaseDocument3 pagesNature and Functions of Bill Of Lading CaseJoey MapaNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Part M Implementation PresentationDocument21 pagesPart M Implementation Presentationbudiaero100% (1)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Pak-US Relations 1947-1990Document13 pagesPak-US Relations 1947-1990Hassan Bin ShahbazNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Technosoft License Agreement PDFDocument12 pagesTechnosoft License Agreement PDFRoberto TorresNo ratings yet

- Cheeseboro Govt MemoDocument9 pagesCheeseboro Govt MemoThe Valley IndyNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

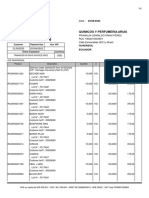

- Factura ComercialDocument6 pagesFactura ComercialKaren MezaNo ratings yet

- Family Law1Document406 pagesFamily Law1Cheezy ChinNo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- People Vs CA and Maquiling (Re GAD)Document13 pagesPeople Vs CA and Maquiling (Re GAD)Vern CastilloNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Remedial Law Review I: Civil Procedure OverviewDocument27 pagesRemedial Law Review I: Civil Procedure Overviewmelaniem_1100% (1)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- STATUTORY CONSTRUCTION LATIN MAXIMSDocument10 pagesSTATUTORY CONSTRUCTION LATIN MAXIMSIa BolosNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Customs Seizure of Ships UpheldDocument2 pagesCustoms Seizure of Ships UpheldFgmtNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

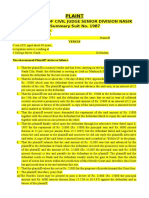

- Plaint: in The Court of Civil Judge Senior Division Nasik Summary Suit No. 1987Document10 pagesPlaint: in The Court of Civil Judge Senior Division Nasik Summary Suit No. 1987Kumar RameshNo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- RUBI v. Provincial BoardDocument3 pagesRUBI v. Provincial BoardMaila Fortich RosalNo ratings yet

- Rogelio Reyes Rodriguez, A205 920 648 (BIA June 23, 2017)Document6 pagesRogelio Reyes Rodriguez, A205 920 648 (BIA June 23, 2017)Immigrant & Refugee Appellate Center, LLCNo ratings yet

- 9 Lopez vs. RamosDocument2 pages9 Lopez vs. Ramosmei atienzaNo ratings yet

- Teoría Producción Por LotesDocument3 pagesTeoría Producción Por LotesGedeón PizarroNo ratings yet

- SOP Contingent I Hiring ProcessDocument15 pagesSOP Contingent I Hiring ProcesskausarNo ratings yet

- Lecture Notes in Criminal Law 2Document5 pagesLecture Notes in Criminal Law 2Vin DualbzNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Student Activity Permit Approval ProcessDocument1 pageStudent Activity Permit Approval ProcessJorge Erwin RadaNo ratings yet

- Commart To San Miguel Case DigestDocument4 pagesCommart To San Miguel Case DigestYolanda Janice Sayan FalingaoNo ratings yet

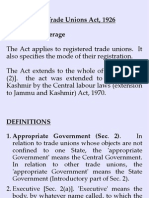

- Trade Unions ActDocument35 pagesTrade Unions ActAnam AminNo ratings yet

- Evolution of Judicial System in India During BritishDocument7 pagesEvolution of Judicial System in India During BritishJay DattaNo ratings yet

- Universal Food Corp. v. CADocument2 pagesUniversal Food Corp. v. CAAiress Canoy CasimeroNo ratings yet

- CTA ProcedureDocument60 pagesCTA ProcedureNori LolaNo ratings yet

- Project Ubing Flow ChartDocument1 pageProject Ubing Flow ChartPaul Angelo 黃種 武No ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)