You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5795)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Amalgamantion and External ReconstructionDocument67 pagesAmalgamantion and External Reconstructionkhuranaamanpreet7gmailcomNo ratings yet

- AuditingDocument21 pagesAuditingShilpan ShahNo ratings yet

- FMChap 1Document46 pagesFMChap 1Khang NguyễnNo ratings yet

- Chapter 14 - Percentage Taxes2013Document11 pagesChapter 14 - Percentage Taxes2013JB RealizaNo ratings yet

- Stock Holding Corporation of India LimitedDocument10 pagesStock Holding Corporation of India LimitedSOMA15No ratings yet

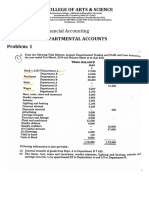

- Departmental Account Problems & AnswerDocument7 pagesDepartmental Account Problems & Answeranand dpiNo ratings yet

- CHP 17 - Commercial Bank Sources & Uses of FundsDocument22 pagesCHP 17 - Commercial Bank Sources & Uses of Fundsrashu892No ratings yet

- Fund Formation Attracting Global Investors PDFDocument87 pagesFund Formation Attracting Global Investors PDFSushimNo ratings yet

- Introduction On Financial InstitutionsDocument73 pagesIntroduction On Financial InstitutionsDipon MajumderNo ratings yet

- 12th Book Keeping Board Papers PDFDocument50 pages12th Book Keeping Board Papers PDFRam IyerNo ratings yet

- ThesisDocument449 pagesThesisHang VeasnaNo ratings yet

- Chapter 7 Angel Ann E. Orola Bsba HR1 1Document90 pagesChapter 7 Angel Ann E. Orola Bsba HR1 1Gwen Stefani DaugdaugNo ratings yet

- 3.1 Sources of Finance 2021Document22 pages3.1 Sources of Finance 2021Sahitya AnandNo ratings yet

- The Whipping PostDocument2 pagesThe Whipping PostAdam SussmanNo ratings yet

- The Role of Mutual Funds in Pakistan TopicDocument11 pagesThe Role of Mutual Funds in Pakistan TopicArif AmanNo ratings yet

- Complete Worksheet of Mod 1-Final Accounts of CompaniesDocument10 pagesComplete Worksheet of Mod 1-Final Accounts of CompaniesNaomi SaldanhaNo ratings yet

- Subros Limited Annual - Report 2012-13Document115 pagesSubros Limited Annual - Report 2012-13Selvaraji MuthuNo ratings yet

- Breakfast With Dave 110509Document7 pagesBreakfast With Dave 110509ejlamasNo ratings yet

- Merger Analysis of HDFC and CBOPDocument18 pagesMerger Analysis of HDFC and CBOPHeidi BellNo ratings yet

- SFM Formulae PDFDocument255 pagesSFM Formulae PDFpiyush bansalNo ratings yet

- Important Banking Awareness Handy NotesDocument29 pagesImportant Banking Awareness Handy NotesShaik UzmaNo ratings yet

- Week 4 Quiz 3Document8 pagesWeek 4 Quiz 3Dawna Lee BerryNo ratings yet

- News Oct 2009Document21 pagesNews Oct 2009Financial HubNo ratings yet

- (Andrew E. Schwartz, Deborah Zemke) Performance Ma (BookFi)Document138 pages(Andrew E. Schwartz, Deborah Zemke) Performance Ma (BookFi)Joy BhattacharyaNo ratings yet

- Capital ExpendituresDocument9 pagesCapital Expenditurestaoyuan521No ratings yet

- Cityam 2011-01-10Document32 pagesCityam 2011-01-10City A.M.No ratings yet

- Assessment 3 2024 Financial AssetDocument9 pagesAssessment 3 2024 Financial AssetAlthea mary kate MorenoNo ratings yet

- Quiz in Business Combi, Conso and Corpo LiqDocument11 pagesQuiz in Business Combi, Conso and Corpo LiqExequielCamisaCrusperoNo ratings yet

- Call OptionDocument1 pageCall OptionMustafa BhaiNo ratings yet

- Portfolio & Investment Management: (KUBS)Document57 pagesPortfolio & Investment Management: (KUBS)Jonathan WilderNo ratings yet