You might also like

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Layman's Guide To Pair TradingDocument9 pagesLayman's Guide To Pair TradingaporatNo ratings yet

- BRAC Bank Limited - Cards P@y Flex ProgramDocument3 pagesBRAC Bank Limited - Cards P@y Flex Programaliva78100% (2)

- Heritage Doll CompanyDocument11 pagesHeritage Doll CompanyDeep Dey0% (1)

- Session 2 - Role of A ManagerDocument65 pagesSession 2 - Role of A Managerapi-3832224100% (1)

- Performance AppraisalDocument29 pagesPerformance Appraisalapi-383222486% (7)

- Session 3 - Issues of HRMDocument14 pagesSession 3 - Issues of HRMapi-3832224No ratings yet

- HRM RJC 1Document21 pagesHRM RJC 1api-3832224100% (1)

- Human Resource PlanningDocument25 pagesHuman Resource Planningapi-3832224100% (3)

- Interviews 1Document25 pagesInterviews 1api-3832224No ratings yet

- Motivation and MoraleDocument42 pagesMotivation and Moraleapi-3832224100% (4)

- CommunicationDocument27 pagesCommunicationapi-3832224No ratings yet

- Incentives PrezDocument38 pagesIncentives Prezapi-3832224100% (1)

- NegotiationDocument27 pagesNegotiationapi-3832224No ratings yet

- Barriesr To CommDocument17 pagesBarriesr To Commapi-3832224100% (1)

- EsopsDocument26 pagesEsopsapi-3832224No ratings yet

- Fringe Benefits 10Document28 pagesFringe Benefits 10api-3832224100% (6)

- Chapter 11Document23 pagesChapter 11api-3832224No ratings yet

- The Income Tax ActDocument32 pagesThe Income Tax Actapi-3832224No ratings yet

- Clubbing of IncomeDocument4 pagesClubbing of Incomeapi-3832224100% (1)

- Set OffDocument3 pagesSet Offapi-3832224No ratings yet

- Barriers To Effective Communication PhotosDocument6 pagesBarriers To Effective Communication Photosapi-3832224100% (2)

- Set Off & Carry Forward of Losses: Lecture NotesDocument45 pagesSet Off & Carry Forward of Losses: Lecture Notesapi-3832224100% (1)

- Barriers To CommunicationDocument22 pagesBarriers To Communicationapi-383222480% (5)

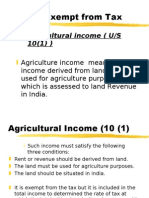

- Income ExemptDocument25 pagesIncome Exemptapi-3832224No ratings yet

- Salaries: Lecture NotesDocument12 pagesSalaries: Lecture Notesapi-3832224100% (1)

- Income ExemptDocument21 pagesIncome Exemptapi-3832224100% (1)

- Taxation 2004 SolvedDocument18 pagesTaxation 2004 Solvedapi-3832224100% (2)

- Minimum Alternate TaxDocument20 pagesMinimum Alternate Taxapi-3832224100% (2)

- Profits and Gains of Business or ProfessionDocument17 pagesProfits and Gains of Business or Professionapi-3832224No ratings yet

- 1st Barcelona Metropolitan Strategic PlanDocument42 pages1st Barcelona Metropolitan Strategic PlanTbilisicds GeorgiaNo ratings yet

- 3 Form BDFSDDocument44 pages3 Form BDFSDMaulik RavalNo ratings yet

- PreviewPDF PDFDocument2 pagesPreviewPDF PDFLing TanNo ratings yet

- قائمة (ب)Document1 pageقائمة (ب)Hossam NasrNo ratings yet

- On Beauty 1 The SalonDocument3 pagesOn Beauty 1 The Salonalessandra LugliNo ratings yet

- 6.1 Government of Pakistan's Treasury Bills: PeriodsDocument13 pages6.1 Government of Pakistan's Treasury Bills: PeriodsKidsNo ratings yet

- CSR Activities of RobiDocument15 pagesCSR Activities of RobiAseki Shakib Khan SimantoNo ratings yet

- Institutional Membership FormDocument2 pagesInstitutional Membership Formdhruvi108No ratings yet

- Spy Gap StudyDocument30 pagesSpy Gap StudyMathias Dharmawirya100% (1)

- 1 - Corporate Social Responsibility Corporate Programme Proposal FormDocument3 pages1 - Corporate Social Responsibility Corporate Programme Proposal FormMohd ShahNo ratings yet

- Extension For Submission: of Time of Written CommentsDocument51 pagesExtension For Submission: of Time of Written CommentsMonali LalNo ratings yet

- 05 Cir V Boac 149 Scra 395Document3 pages05 Cir V Boac 149 Scra 395Angelette BulacanNo ratings yet

- Bankura TP ListDocument16 pagesBankura TP ListDeb D Creative StudioNo ratings yet

- IGNOU Tutor Marked AssignmentDocument5 pagesIGNOU Tutor Marked AssignmentshivalimohanNo ratings yet

- 343-Article Text-1058-1-10-20121119 PDFDocument4 pages343-Article Text-1058-1-10-20121119 PDFSam H BerhanuNo ratings yet

- Esteva Commoning in The New SocietyDocument16 pagesEsteva Commoning in The New SocietyMotin-drNo ratings yet

- Ijcrt1704123 PDFDocument6 pagesIjcrt1704123 PDFshivanand shuklaNo ratings yet

- Historias de Éxito FH Bolivia LivDocument14 pagesHistorias de Éxito FH Bolivia LivMarcelo Alvarez AscarrunzNo ratings yet

- Dornbusch 6e Chapter12Document19 pagesDornbusch 6e Chapter12kushalNo ratings yet

- Electronic Challan .1.9Document27 pagesElectronic Challan .1.9Soumya BisoiNo ratings yet

- Bhavnath TempleDocument7 pagesBhavnath TempleManpreet Singh'100% (1)

- First Draft of The 2012 City of Brantford Budget DocumentsDocument1,181 pagesFirst Draft of The 2012 City of Brantford Budget DocumentsHugo Rodrigues100% (1)

- RP 1Document42 pagesRP 1Pahe LambNo ratings yet

- Seven FridayDocument15 pagesSeven FridayRoshan Acharya0% (1)

- 35X70 One City-ModelDocument1 page35X70 One City-ModelRD DaskaNo ratings yet

- Ongoing Renewable Projects GeorgiaDocument4 pagesOngoing Renewable Projects GeorgiamokarcanNo ratings yet

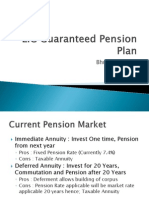

- LIC Guaranteed HNI Pension PlanDocument9 pagesLIC Guaranteed HNI Pension PlanBhushan ShethNo ratings yet