You might also like

- The Statement of Financial Position of Ninety LTD For The Last Two Years AreDocument2 pagesThe Statement of Financial Position of Ninety LTD For The Last Two Years Arenjoroge mwangiNo ratings yet

- SFM CA Final Mutual FundDocument7 pagesSFM CA Final Mutual FundShrey KunjNo ratings yet

- Biniyam Yitbarek Article Review On Financial AnalysisDocument6 pagesBiniyam Yitbarek Article Review On Financial AnalysisBiniyam Yitbarek100% (1)

- Chapter 04 Working Capital 1ce Lecture 050930Document71 pagesChapter 04 Working Capital 1ce Lecture 050930rthillai72No ratings yet

- Problems On Cash Management Baumol ModelsDocument1 pageProblems On Cash Management Baumol ModelsDeepak100% (1)

- Banking CompaniesDocument68 pagesBanking CompaniesKiran100% (2)

- Financial Management - PPT - 2011Document134 pagesFinancial Management - PPT - 2011Bhanu Prakash100% (1)

- Approaches in Portfolio ConstructionDocument2 pagesApproaches in Portfolio Constructionnayakrajesh89No ratings yet

- Industry and Life Cycle AnalysisDocument31 pagesIndustry and Life Cycle AnalysisASK ME ANYTHING SMARTPHONENo ratings yet

- Cost of CaptialDocument72 pagesCost of CaptialkhyroonNo ratings yet

- CS Executive MCQ and Risk AnalysisDocument17 pagesCS Executive MCQ and Risk Analysis19101977No ratings yet

- Financial Management 2: UCP-001BDocument3 pagesFinancial Management 2: UCP-001BRobert RamirezNo ratings yet

- Ch-8 Investing Decision Capital BudgetingDocument58 pagesCh-8 Investing Decision Capital BudgetingAbdela AyalewNo ratings yet

- How To Write A Ratio AnalysisDocument2 pagesHow To Write A Ratio AnalysisLe TanNo ratings yet

- FM S5 Capitalstructure TheoriesDocument36 pagesFM S5 Capitalstructure TheoriesSunny RajoraNo ratings yet

- Lecture Notes2231 SCMDocument57 pagesLecture Notes2231 SCMhappynandaNo ratings yet

- Unit 2 Capital Budgeting Decisions: IllustrationsDocument4 pagesUnit 2 Capital Budgeting Decisions: IllustrationsJaya SwethaNo ratings yet

- Bond ValuationDocument38 pagesBond ValuationAbdii DhufeeraNo ratings yet

- M09 Gitman50803X 14 MF C09Document56 pagesM09 Gitman50803X 14 MF C09dhfbbbbbbbbbbbbbbbbbhNo ratings yet

- BCG ApproachDocument2 pagesBCG ApproachAdhityaNo ratings yet

- Fnce 220: Business Finance: Lecture 6: Capital Investment DecisionsDocument39 pagesFnce 220: Business Finance: Lecture 6: Capital Investment DecisionsVincent KamemiaNo ratings yet

- Leverage PPTDocument13 pagesLeverage PPTamdNo ratings yet

- Capital Structure TheoriesDocument47 pagesCapital Structure Theoriesamol_more37No ratings yet

- 5 - Capital Budgeting - Risk & UncertaintyDocument22 pages5 - Capital Budgeting - Risk & UncertaintySymron KheraNo ratings yet

- Tandon Committee Report On Working CapitalDocument4 pagesTandon Committee Report On Working CapitalMohitAhujaNo ratings yet

- Decision Areas in Financial ManagementDocument15 pagesDecision Areas in Financial ManagementSana Moid100% (3)

- Chapter - 05 - Activity - Based - Costing - ABC - .Doc - Filename UTF-8''Chapter 05 Activity Based Costing (ABC)Document8 pagesChapter - 05 - Activity - Based - Costing - ABC - .Doc - Filename UTF-8''Chapter 05 Activity Based Costing (ABC)NasrinTonni AhmedNo ratings yet

- Oaf 624 Course OutlineDocument8 pagesOaf 624 Course OutlinecmgimwaNo ratings yet

- Indian Financial System - An Overview - Mahesh ParikhDocument33 pagesIndian Financial System - An Overview - Mahesh ParikhJe RomeNo ratings yet

- Ratio Analysis Assignment 2020Document1 pageRatio Analysis Assignment 2020Nguyễn Thu TrangNo ratings yet

- 14 - Dividend Policy SumsDocument17 pages14 - Dividend Policy SumsRISHA SHETTYNo ratings yet

- Chapter 3 Valuation and Cost of CapitalDocument92 pagesChapter 3 Valuation and Cost of Capitalyemisrach fikiruNo ratings yet

- SAPM Portfolio EvaluationDocument6 pagesSAPM Portfolio EvaluationsarahrahulNo ratings yet

- The Cost of CapitalDocument18 pagesThe Cost of CapitalzewdieNo ratings yet

- SHRMDocument10 pagesSHRMArya Akbani100% (1)

- Financial Management Assignment - Sem IIDocument11 pagesFinancial Management Assignment - Sem IIAkhilesh67% (3)

- Problems Sub-IfDocument11 pagesProblems Sub-IfChintakunta PreethiNo ratings yet

- MBA QuestionsDocument15 pagesMBA QuestionsKhanal NilambarNo ratings yet

- Gitman Chapter 15 Working CapitalDocument67 pagesGitman Chapter 15 Working CapitalArif SharifNo ratings yet

- Unit 2 Capital StructureDocument27 pagesUnit 2 Capital StructureNeha RastogiNo ratings yet

- 35 Financial Management FM 71 Imp Questions With Solution For CA Ipcc MsDocument90 pages35 Financial Management FM 71 Imp Questions With Solution For CA Ipcc Msmysorevishnu75% (8)

- Corporate Finance Ppt. SlideDocument24 pagesCorporate Finance Ppt. SlideMd. Jahangir Alam100% (1)

- L&T Financial Services Case StudyDocument12 pagesL&T Financial Services Case StudyKaushlendraKumarNo ratings yet

- CH 12. Risk Evaluation in Capital BudgetingDocument29 pagesCH 12. Risk Evaluation in Capital BudgetingN-aineel DesaiNo ratings yet

- Working Capital MGTDocument14 pagesWorking Capital MGTrupaliNo ratings yet

- IBA Suggested Solution First MidTerm Taxation 12072016Document9 pagesIBA Suggested Solution First MidTerm Taxation 12072016Syed Azfar HassanNo ratings yet

- 5.calculation of EPSDocument6 pages5.calculation of EPSVinitgaNo ratings yet

- Cost of CapitalDocument34 pagesCost of CapitalShubham SinghNo ratings yet

- PPTDocument27 pagesPPTafeeraNo ratings yet

- Investment ManagementDocument38 pagesInvestment ManagementPranjit BhuyanNo ratings yet

- The Impact of Government Policy and Regulation On BankingDocument15 pagesThe Impact of Government Policy and Regulation On BankingAmna Nasser100% (1)

- Topic 1 The Investment EnvironmentDocument19 pagesTopic 1 The Investment EnvironmentDavid Adeabah Osafo100% (1)

- Balance of Payments: International FinanceDocument42 pagesBalance of Payments: International FinanceSoniya Rht0% (1)

- Lecture 7 Adjusted Present ValueDocument19 pagesLecture 7 Adjusted Present ValuePraneet Singavarapu100% (1)

- Hire PurchaseDocument49 pagesHire PurchasePriya SinghNo ratings yet

- Corporate Financial Analysis with Microsoft ExcelFrom EverandCorporate Financial Analysis with Microsoft ExcelRating: 5 out of 5 stars5/5 (1)

- Value Chain Management Capability A Complete Guide - 2020 EditionFrom EverandValue Chain Management Capability A Complete Guide - 2020 EditionNo ratings yet

- Fair Value C NsultingDocument67 pagesFair Value C NsultingGiri SukumarNo ratings yet

- Providing Service Quality Through Internal MarketingDocument31 pagesProviding Service Quality Through Internal MarketingAamit KumarNo ratings yet

- Rural BankingDocument25 pagesRural BankingAamit KumarNo ratings yet

- BajajDocument13 pagesBajajAamit KumarNo ratings yet

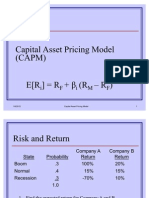

- Capital Asset Pricing ModelDocument25 pagesCapital Asset Pricing ModelAamit KumarNo ratings yet

- AttitudeDocument5 pagesAttitudeAamit KumarNo ratings yet

- PM2 - The Marketing ProcessDocument41 pagesPM2 - The Marketing ProcessRHam VariasNo ratings yet

- Mock D QDocument15 pagesMock D QZeeshan Shaikh100% (1)

- Acquarius Case AnalysisDocument6 pagesAcquarius Case AnalysisEarl MarquezNo ratings yet

- IM Test-BankDocument20 pagesIM Test-BankHoàng TrâmNo ratings yet

- Varun ProjectDocument14 pagesVarun ProjectRaj KumarNo ratings yet

- SAP TablesDocument26 pagesSAP TablesjackNo ratings yet

- BUS 2201 Discussion Forum Unit 2Document1 pageBUS 2201 Discussion Forum Unit 2Cherry HtunNo ratings yet

- Case Study Ameritrade: Cost of CapitalDocument14 pagesCase Study Ameritrade: Cost of Capitalsnigdha_saniNo ratings yet

- Functions of Financial ManagementDocument15 pagesFunctions of Financial ManagementCarla B. JimenezNo ratings yet

- Marketing Planning StrategyDocument199 pagesMarketing Planning StrategyNaturell India RitebiteNo ratings yet

- Managerial Economics Assignment Question Spring 21Document1 pageManagerial Economics Assignment Question Spring 21farhan Momen100% (2)

- ATM For Advertising and PromotionDocument1 pageATM For Advertising and PromotionwritershoodNo ratings yet

- Redeveloped Division Initiated Self-Learning Module: Department of Education - Division of PalawanDocument20 pagesRedeveloped Division Initiated Self-Learning Module: Department of Education - Division of PalawanRajer AlsadNo ratings yet

- Product EndorsementDocument16 pagesProduct Endorsementrud_jaypee_rathoreNo ratings yet

- Miles CPA RoadmapDocument72 pagesMiles CPA RoadmapRoshan SNo ratings yet

- Basel Disclouser Chaitra2070Document2 pagesBasel Disclouser Chaitra2070Krishna Bahadur ThapaNo ratings yet

- Benefits of Supply ChainDocument4 pagesBenefits of Supply ChainOkorie SundayNo ratings yet

- Strategic and Marketing PlanningDocument13 pagesStrategic and Marketing PlanningCarmilleah Freyjah100% (1)

- Akash Kumar Singh : ProfileDocument1 pageAkash Kumar Singh : ProfileZamirtalent TrNo ratings yet

- AFAR Problem MCQDocument45 pagesAFAR Problem MCQGJames ApostolNo ratings yet

- Education Allendale School Marketing PlanDocument29 pagesEducation Allendale School Marketing PlansethasarakmonyNo ratings yet

- The Study of Cash Flow Statement of Axis Bank For Period 2017-21Document11 pagesThe Study of Cash Flow Statement of Axis Bank For Period 2017-21Dnyandeep ManwarNo ratings yet

- Bank of Rajasthan MergerDocument75 pagesBank of Rajasthan MergerArunKumar100% (1)

- Oracle Inventory and Costing Cloud EbookDocument11 pagesOracle Inventory and Costing Cloud Ebooksingh_indrajeetkumarNo ratings yet

- Chapter 2, Lesson 3demand ForecastingDocument15 pagesChapter 2, Lesson 3demand Forecastingfelize padllaNo ratings yet

- Nature of Corporate PersonalityDocument18 pagesNature of Corporate Personalitypokandi.fbNo ratings yet

- Lecture 2 - Regulatory FrameworkDocument29 pagesLecture 2 - Regulatory FrameworkFarwa AroojNo ratings yet

- Cancellation of 4ward ContractDocument8 pagesCancellation of 4ward ContractManu K AnujanNo ratings yet

- Aptitude QuestionsDocument4 pagesAptitude QuestionsRavindra BabuNo ratings yet

- Strategy - Multiple Choice QuestionsDocument7 pagesStrategy - Multiple Choice QuestionsWolf's RainNo ratings yet