You might also like

- Monte Carlo SimulationDocument22 pagesMonte Carlo SimulationWillinton GutierrezNo ratings yet

- Sensitivity AnalysisDocument33 pagesSensitivity AnalysisMary McfaddenNo ratings yet

- Linear Programming: Sensitivity Analysis and Interpretation of SolutionDocument56 pagesLinear Programming: Sensitivity Analysis and Interpretation of Solutionjony96100% (1)

- Mba Statistics First Long QuizDocument7 pagesMba Statistics First Long QuizEllaine Jane FajardoNo ratings yet

- Time Value of Money ScriptDocument15 pagesTime Value of Money ScriptSudheesh Murali NambiarNo ratings yet

- Regression Models ProjectDocument5 pagesRegression Models ProjectAkshay RaoNo ratings yet

- 01 Probability and Probability DistributionsDocument18 pages01 Probability and Probability DistributionsRama DulceNo ratings yet

- Basic Statistics 6 Sample Vs Population DistributionsDocument26 pagesBasic Statistics 6 Sample Vs Population DistributionsJay Ann DomeNo ratings yet

- Chapter 7 - K-Nearest-Neighbor: Data Mining For Business IntelligenceDocument17 pagesChapter 7 - K-Nearest-Neighbor: Data Mining For Business Intelligencejay100% (1)

- Cost of Capital Excel Temple-Free CH 10Document10 pagesCost of Capital Excel Temple-Free CH 10Mohiuddin AshrafiNo ratings yet

- Chapter 14 - Cluster Analysis: Data Mining For Business IntelligenceDocument31 pagesChapter 14 - Cluster Analysis: Data Mining For Business IntelligencejayNo ratings yet

- Ch08 Linear Programming SolutionsDocument26 pagesCh08 Linear Programming SolutionsVikram SanthanamNo ratings yet

- Statistics 578 Assignment 5 HomeworkDocument13 pagesStatistics 578 Assignment 5 HomeworkMia Dee100% (5)

- Simple Linear RegressionDocument18 pagesSimple Linear RegressionAriel Raye RicaNo ratings yet

- ARIMA ForecastingDocument9 pagesARIMA Forecastingilkom12No ratings yet

- Valuation of Bonds and Shares: Problem 1Document29 pagesValuation of Bonds and Shares: Problem 1Sourav Kumar DasNo ratings yet

- FM Practice Questions KeyDocument7 pagesFM Practice Questions KeykeshavNo ratings yet

- Curve FittingDocument4 pagesCurve FittingIlham Indrapraja IskandarNo ratings yet

- Sensitivity AnalysisDocument7 pagesSensitivity AnalysisChaitanya100% (1)

- Week3 Logistic Regression Post PDFDocument110 pagesWeek3 Logistic Regression Post PDFYecheng Caroline LiuNo ratings yet

- Ch01 Business StatisticsDocument65 pagesCh01 Business StatisticsApu DawNo ratings yet

- Time Series Forecasting Chapter 16Document43 pagesTime Series Forecasting Chapter 16Jeff Ray SanchezNo ratings yet

- HW 1, FIN 604, Sadhana JoshiDocument40 pagesHW 1, FIN 604, Sadhana JoshiSadhana JoshiNo ratings yet

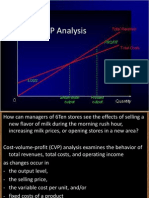

- CVP Analysis Helps Evaluate Effects of ChangesDocument41 pagesCVP Analysis Helps Evaluate Effects of ChangesAbdulyunus Amir100% (1)

- Discounted Cash Flow (DCF) ModellingDocument43 pagesDiscounted Cash Flow (DCF) Modellingjasonccheng25No ratings yet

- Monte Carlo Simulation ExplainedDocument3 pagesMonte Carlo Simulation ExplainedNihar DeyNo ratings yet

- CH 13 SolutionsDocument7 pagesCH 13 SolutionsSyed Mohsin Haider0% (1)

- Analyzing Decisions with Decision Trees and Expected UtilityDocument27 pagesAnalyzing Decisions with Decision Trees and Expected Utilitymanu192No ratings yet

- Anlyse Mine UnstructeredData@SocialMediaDocument80 pagesAnlyse Mine UnstructeredData@SocialMediaVenkata Nelluri Pmp100% (1)

- Semester-I Managerial Economics MBA-DA-103 Credits-5: Learning ObjectiveDocument2 pagesSemester-I Managerial Economics MBA-DA-103 Credits-5: Learning ObjectiveAshish AcharjeeNo ratings yet

- The Internet of Things (Iot)Document25 pagesThe Internet of Things (Iot)Ankit ThakkarNo ratings yet

- Regression AnalysisDocument280 pagesRegression AnalysisA.Benhari100% (1)

- Finance Formulas Break-Even Analysis NPV IRRDocument1 pageFinance Formulas Break-Even Analysis NPV IRRAbiMatarloNo ratings yet

- Curves Coefficients Cutoffs@measurments Sensitivity SpecificityDocument66 pagesCurves Coefficients Cutoffs@measurments Sensitivity SpecificityVenkata Nelluri PmpNo ratings yet

- Chap4 Exercise On Sensitivity Analysis SolutionDocument2 pagesChap4 Exercise On Sensitivity Analysis SolutionIves LeeNo ratings yet

- Group Work Case 10 Berkshire InstrumentsDocument3 pagesGroup Work Case 10 Berkshire InstrumentsPatrick Alsim100% (4)

- Predict used Toyota Corolla prices from specsDocument5 pagesPredict used Toyota Corolla prices from specspavan adapalaNo ratings yet

- CH 5Document3 pagesCH 5AnonymousNo ratings yet

- Case Study 4Document10 pagesCase Study 4fayre86No ratings yet

- Linear Programming Problem (LPP)Document65 pagesLinear Programming Problem (LPP)Mahesh Rangaswamy100% (1)

- AnalyticsDocument50 pagesAnalyticsIkshit Bhushan0% (1)

- Regression Analysis Explained in 40 CharactersDocument21 pagesRegression Analysis Explained in 40 CharactersjjjjkjhkhjkhjkjkNo ratings yet

- Ch11Integer Goal ProgrammingDocument54 pagesCh11Integer Goal ProgrammingAngelina WattssNo ratings yet

- Regression Analysis: Brand Association and ReplicaDocument5 pagesRegression Analysis: Brand Association and ReplicaAnonymous K9PRixtrOONo ratings yet

- EXERCISE - Calculating The Internal Rate of ReturnDocument5 pagesEXERCISE - Calculating The Internal Rate of ReturnNipun BajajNo ratings yet

- Computer AssignmentDocument6 pagesComputer AssignmentSudheender Srinivasan0% (1)

- CE 366 Exam 3 Review - SDocument7 pagesCE 366 Exam 3 Review - SShaunak TripathiNo ratings yet

- Business StatisticsDocument123 pagesBusiness StatisticsCarla Tate100% (2)

- R06 The Time Value of Money Q BankDocument19 pagesR06 The Time Value of Money Q BankTeddy JainNo ratings yet

- Evans - Analytics2e - PPT - SC BDocument39 pagesEvans - Analytics2e - PPT - SC Bsener.asliNo ratings yet

- Sensitivity Analysis: Linear ProgrammingDocument45 pagesSensitivity Analysis: Linear ProgrammingHoa NguyenNo ratings yet

- DualityDocument26 pagesDualityNavneet RaiNo ratings yet

- Linear Programming Sensitivity AnalysisDocument35 pagesLinear Programming Sensitivity AnalysisALLISON GRUBBSNo ratings yet

- Linear Programming Sensitivity Analysis: © 2007 Pearson EducationDocument37 pagesLinear Programming Sensitivity Analysis: © 2007 Pearson Educationhussain.aabid309No ratings yet

- 4 Sensitivity AnalysisDocument35 pages4 Sensitivity AnalysisVidhi MaheshwariNo ratings yet

- SA Optimal SensitivityDocument21 pagesSA Optimal SensitivitySahil ChaudharyNo ratings yet

- NOTES 6 - Sensitivity Analysis3Document36 pagesNOTES 6 - Sensitivity Analysis3Danny MwaleNo ratings yet

- Optimal Operating Level: Economies of Scale Diseconomies of ScaleDocument24 pagesOptimal Operating Level: Economies of Scale Diseconomies of ScaleAbhay Srivastava100% (1)

- Computer Solution and Sensitivity Analysis of Linear Programming ProblemsDocument38 pagesComputer Solution and Sensitivity Analysis of Linear Programming ProblemsBob RobNo ratings yet

- Design Review PP (12-1)Document38 pagesDesign Review PP (12-1)Janaka DonNo ratings yet

- Bain What It Takes To Win in Customer ExperienceDocument12 pagesBain What It Takes To Win in Customer ExperienceJishnu Chakraborty100% (2)

- Big Data StartupsDocument10 pagesBig Data StartupsJishnu ChakrabortyNo ratings yet

- TM Website AnalysisDocument16 pagesTM Website AnalysisJishnu ChakrabortyNo ratings yet

- MoreDocument1 pageMoreJishnu ChakrabortyNo ratings yet

- Photography Composition RulesDocument42 pagesPhotography Composition RulesJishnu ChakrabortyNo ratings yet

- Higher Algebra - Hall & KnightDocument593 pagesHigher Algebra - Hall & KnightRam Gollamudi100% (2)

- Constrained Flow Shop Scheduling With N-Jobs, Machines, Processing Time Associated With Probability Involving TransportationDocument13 pagesConstrained Flow Shop Scheduling With N-Jobs, Machines, Processing Time Associated With Probability Involving TransportationiisteNo ratings yet

- Higher Algebra - Hall & KnightDocument593 pagesHigher Algebra - Hall & KnightRam Gollamudi100% (2)

- Steam TurbineDocument102 pagesSteam Turbinerashm006ranjan67% (3)

- Asme Sec Ix 2019 381Document1 pageAsme Sec Ix 2019 381Balkishan DyavanapellyNo ratings yet

- Plastic Ban LetterDocument5 pagesPlastic Ban LetterrkarlinNo ratings yet

- Lab 7 Fluid SaturationDocument6 pagesLab 7 Fluid SaturationRichard OwusuNo ratings yet

- Cp12 Pps 3274c Me Ds 001 Data Sheet Hvac Sunyaragi Rev.0Document1 pageCp12 Pps 3274c Me Ds 001 Data Sheet Hvac Sunyaragi Rev.0Triana Rosma Fikriyati DinaNo ratings yet

- En 13364 - 2001Document2 pagesEn 13364 - 2001Letícia Valdo0% (1)

- Gas Dynamics MCQsDocument6 pagesGas Dynamics MCQsprawinlNo ratings yet

- Demonstration of Wireless Gas Sensor Using Reduced Graphene Oxide Loaded Patch AntennaDocument3 pagesDemonstration of Wireless Gas Sensor Using Reduced Graphene Oxide Loaded Patch AntennaJeff SalesNo ratings yet

- Lab Manual 15B17CI574 Artificial Intelligence Lab PDFDocument45 pagesLab Manual 15B17CI574 Artificial Intelligence Lab PDFAviral TanwarNo ratings yet

- Individualized Education Plan Annex 6Document5 pagesIndividualized Education Plan Annex 6Fritzie Ann BinegaNo ratings yet

- Early 2011 Macbook Pro SpecsDocument4 pagesEarly 2011 Macbook Pro SpecsMatthew Timothy PuaNo ratings yet

- Building Resilient Teams Workbook FINALDocument16 pagesBuilding Resilient Teams Workbook FINALКремена П.No ratings yet

- BSBWHS308Document40 pagesBSBWHS308Pragati AryalNo ratings yet

- CII4Q3 - Computer Vision-EAR - Week-11-Intro To Deep Learning v1.0Document50 pagesCII4Q3 - Computer Vision-EAR - Week-11-Intro To Deep Learning v1.0Zee IngameNo ratings yet

- 2 Oieyqhwgfdewio 9 D 328 eDocument1 page2 Oieyqhwgfdewio 9 D 328 euihgfhjjhghNo ratings yet

- Abis For GSM TelecommunicationsDocument2 pagesAbis For GSM TelecommunicationsUmar Abbas BabarNo ratings yet

- Introduction: Nature and Background of the StudyDocument24 pagesIntroduction: Nature and Background of the StudyJm BalessNo ratings yet

- Chap # 14 (Electromagnetic Induction)Document6 pagesChap # 14 (Electromagnetic Induction)Tariq MahmoodNo ratings yet

- Acopl Todos - MétricoDocument53 pagesAcopl Todos - MétricoDaniela E. Wagner100% (1)

- Xylux Lr3: High Output Emergency LED Luminaire Suitable For 10.8 Lux ApplicationsDocument4 pagesXylux Lr3: High Output Emergency LED Luminaire Suitable For 10.8 Lux ApplicationsAtiqNo ratings yet

- Fujifilm Ga645 FullDocument31 pagesFujifilm Ga645 FullWork In ArtNo ratings yet

- Outline Medical TerminologyDocument3 pagesOutline Medical TerminologypearlparfaitNo ratings yet

- Mechanical Intro 17.0 WS06.2 JointsDocument15 pagesMechanical Intro 17.0 WS06.2 JointsInventor SolidworksNo ratings yet

- Transition Novels: Conrad, Lawrence and ModernismDocument6 pagesTransition Novels: Conrad, Lawrence and ModernismAndrea GiubellinoNo ratings yet

- A320 71-80v2500jarb1 PDFDocument415 pagesA320 71-80v2500jarb1 PDFHoang L A TuanNo ratings yet

- Redevelopment ThesisDocument5 pagesRedevelopment Thesisjessicaandersonseattle100% (2)

- MentahanDocument2 pagesMentahanNoviyanti 008No ratings yet

- Analysis of Entropy Generation Inside Concentric Cylindrical Annuli With Relative RotatioDocument9 pagesAnalysis of Entropy Generation Inside Concentric Cylindrical Annuli With Relative RotatioSafaa Hameed Al NaseryNo ratings yet

- The Rose Review 2009Document217 pagesThe Rose Review 2009Matt Grant100% (3)

- Physics of FluidsDocument41 pagesPhysics of FluidsSherwin PNo ratings yet